Macy’s, Inc. (M) used its first quarter of fiscal 2026 call to make a broader point than an earnings beat. Management said the company’s Bold New Chapter strategy is gaining traction across banners, with stronger execution, healthier category breadth and a more responsive customer.

That message mattered because the quarter also gave Macy’s room to raise full-year guidance while keeping a cautious tone on tariffs, fuel costs and the macro backdrop.

Macy’s Raises Outlook After Broad-Based Beat

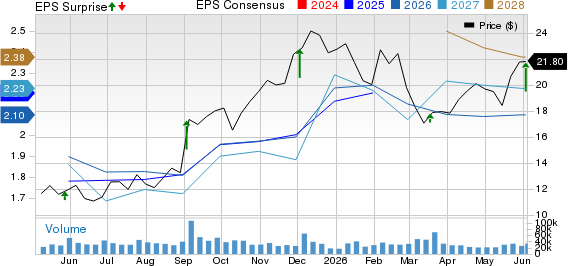

M reported adjusted earnings per share of $0.13, ahead of the Zacks Consensus Estimate of $0.02 and delivering a 678.44% surprise. Revenues of $4.68 billion also topped the Zacks Consensus Estimate of $4.62 billion by 1.28%.

Macy's, Inc. Price, Consensus and EPS Surprise

Macy's, Inc. price-consensus-eps-surprise-chart | Macy's, Inc. Quote

Chief executive officer and chairman Tony Spring said the company posted its best comparable sales performance in four years, with all nameplates and channels positive. He framed that as evidence that Macy’s merchandising, service and marketing changes are starting to resonate more consistently.

Management also raised full-year guidance. Macy’s now expects fiscal 2026 net sales of $21.5 billion to $21.75 billion, comparable sales growth of 0.5% to 1.2% and adjusted EPS of $2.00 to $2.20.

Macy’s Reimagine Stores Keep Leading the Chain

Spring pointed to Macy’s nameplate as a central proof point for the strategy, with comparable sales up 1.6% and Reimagine 200 locations up 2.4%. He said those stores have now delivered positive comparable sales in eight of the last nine quarters.

The CEO described Reimagine less as a single initiative than as a store-level operating model. He said the gains are coming from sharper assortments, stronger storytelling, added staffing, better fitting-room and beauty service, and more local decision-making.

That local element came up again in the Q&A. Responding to Telsey Advisory Group, Spring said local leaders now have more freedom to deploy resources by floor and area, which he tied to better execution across regions and cohorts.

Macy’s Sees Luxury and Beauty Outperform

The strongest growth again came from Macy’s higher-end banners. Bloomingdale’s comparable sales rose 10.2%, while Bluemercury comps increased 6.4%.

Spring said Bloomingdale’s is benefiting from premium contemporary and luxury positioning, new brands, personalized service and traffic-driving events. He also said the banner is gaining from closer collaboration with Macy’s without losing brand distinction.

Beauty remained another bright spot. Management said Bluemercury’s quarter was driven by makeup, dermatological skin care and fragrances, while Spring added in the Q&A that all three banners are leaning into service-led beauty experiences to make stores more relevant.

Macy’s Balances Growth Spending and Cost Pressure

Chief operating officer and chief financial officer Thomas Edwards said gross margin was 38.9% of net sales, down 30 basis points from last year. Excluding tariffs, he said gross margin would have been flat.

Edwards argued that expense control was a bigger positive. SG&A was flat as a percent of revenues despite continued investment in Reimagine, Bloomingdale’s and digital initiatives, helping adjusted EBITDA come in above guidance at 5.9% of total revenues.

The company’s outlook still reflects outside cost pressure. Edwards said full-year guidance assumes tariff rates lower than previously expected but also elevated fuel and transportation costs, with the two factors netting to a neutral effect for the year.

Macy’s Q&A Centers on Traffic, AUR and Margins

Several analysts pressed on the durability of the sales momentum. In response to questions from Jefferies and Goldman Sachs, management said second-quarter trends had remained encouraging and the first quarter was notably consistent month to month.

Spring said traffic improved sequentially, while average unit retail and basket size stayed supportive. He told analysts that Macy’s is carrying a better mix of premium fabrication, stronger brands and less clearance merchandise, which is helping pricing without relying on heavier promotions.

Evercore ISI and UBS focused on the link between higher AUR and margins. Edwards said first-quarter gross margin performance was in line with internal expectations and maintained that the company still sees room for margin build through the rest of the year as inventory and assortment tools improve.

Macy’s Uses AI and Events to Deepen Engagement

Macy’s also used the call to highlight customer-facing and operational initiatives beyond the quarter. Spring said Ask Macy’s, the new AI-powered shopping assistant, is producing higher conversion among users in its early stages.

Edwards added that the company now has 35 AI pilots and tests underway, spanning customer service, associate productivity and supply-chain use cases. He said the goal is to support the broader strategy rather than pursue technology for its own sake.

Management also emphasized event-driven customer engagement. Spring tied upcoming fireworks, parade, MLB and World Cup activations to Macy’s effort to create reasons to visit stores and digital channels beyond basic need-based purchases.

Macy’s Ends the Call With Measured Confidence

The tone exiting the call was constructive but disciplined. Spring repeatedly said the company feels good about the factors it can control, while keeping room for guidance for geopolitical and macro uncertainty.

Edwards reinforced that posture by pairing the stronger sales outlook with a prudent stance on tariffs, fuel and competitive conditions. The overall message was that Macy’s sees clearer internal momentum, but is not ready to declare the external environment easy.

Macy’s Rank and Style Signals

M carries a Zacks Rank #4 (Sell), along with a Value Score of A, Growth Score of B, Momentum Score of A and VGM Score of A. Those Style Scores point to favorable characteristics across value, growth and momentum factors, with the VGM Score indicating strong combined appeal.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Still, Zacks materials make clear that the Rank takes priority over the Style Scores. A Zacks Rank #4 signals weaker earnings estimate revision trends, even when other style measures look attractive. That rank can change after a fresh earnings report as analyst estimates are updated.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Macy's, Inc. (M): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).