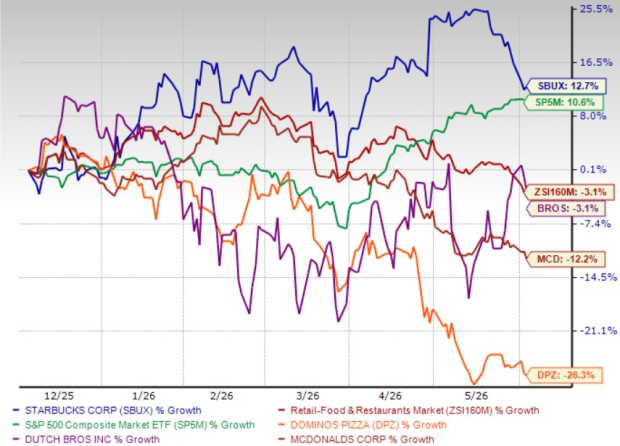

Starbucks Corporation SBUX stock has come under pressure lately, declining 8.6% over the past month compared with the industry's 5.1% drop. In contrast, the S&P 500 has advanced 3.9% during the same period, reflecting investors' concerns about near-term demand trends and the pace of the company's turnaround efforts.

However, the recent weakness does not tell the full story. Over the past six months, Starbucks’ shares have gained 12.7%, against the industry’s decline of 3.1%. The stock's longer-term resilience highlights investor confidence in the company's strategic initiatives, including efforts to enhance customer experience, improve operational efficiency and reignite traffic growth.

With the shares now trading below recent highs, investors may be wondering whether the pullback presents an attractive buying opportunity. While macroeconomic uncertainty and consumer spending pressures remain headwinds, Starbucks' strong brand equity, expanding digital ecosystem and ongoing turnaround strategy could position it for improved long-term performance.

In the past six months, Starbucks has also outperformed other industry players, such as McDonald's Corporation MCD and Dutch Bros Inc. BROS.

Price Performance

Image Source: Zacks Investment Research

Can Starbucks' Turnaround Initiatives Drive the Stock Higher?

Starbucks may be nearing a turning point after several quarters of operational challenges and slowing traffic trends. The company's second-quarter fiscal 2026 results showed meaningful progress, with revenues, earnings and comparable-store sales all returning to growth. More importantly, management highlighted several initiatives that could support sustainable growth and help the stock regain momentum.

One of the biggest positives is the improvement in customer traffic. Starbucks reported its strongest U.S. transaction growth in about three years, with gains across all dayparts and customer income groups. The recovery suggests that efforts to improve the in-store experience are resonating with consumers. Morning traffic has nearly returned to levels seen several years ago, while delivery continues to add incremental sales and expand customer reach.

A major contributor to this progress is the company's Green Apron Service initiative. Starbucks has invested heavily in staffing, training, scheduling and operational execution to deliver faster and more consistent service. Management noted that customer experience scores continue to improve and service times remain on target despite rising transaction volumes. As these initiatives are rolled out across more stores, Starbucks should be able to drive higher customer satisfaction and repeat visits.

Product innovation is providing another source of growth. New beverages, including premium Matcha drinks, energy refreshers and seasonal offerings, are generating strong customer interest. Starbucks' refresher platform has become a significant business and management believes that further product extensions and customization options can expand demand, particularly during the afternoon. Continued innovation should help the company remain relevant in an increasingly competitive beverage market.

The Starbucks Rewards ecosystem is also emerging as a key competitive advantage. Active membership reached a record high during the quarter, while the redesigned rewards structure is encouraging greater engagement and visit frequency. Unlike many restaurant chains that rely heavily on discounts, Starbucks is using personalization and loyalty benefits to deepen customer relationships and strengthen spending patterns.

Beyond sales growth, Starbucks has a clear path to improving profitability. Management remains committed to a multiyear $2 billion cost-savings plan while expecting pressure from coffee costs and tariffs to ease in the second half of fiscal 2026. At the same time, organizational streamlining and productivity improvements should help expand margins as revenue growth accelerates.

International markets also offer meaningful upside. All of Starbucks' top international markets posted positive comparable sales growth during the quarter, while China delivered transaction growth for the fourth consecutive quarter. The company's new partnership structure in China is expected to support expansion while improving long-term returns.

With traffic improving, customer loyalty strengthening, innovation gaining traction and margins poised to recover, Starbucks appears better positioned than it has been in years. If management continues to execute its turnaround strategy successfully, these factors could help drive earnings growth and put the stock back on a sustained upward path.

SBUX’s Estimate Revision Trend

The Zacks Consensus Estimate for SBUX's fiscal 2026 and 2027 EPS moved up in the past 60 days, indicating positive sentiment among analysts for its earnings.

Image Source: Zacks Investment Research

Taking a Look at Starbucks’ Valuation

SBUX stock is trading below the industry. With a forward 12-month price/sales ratio of 2.76X, below its industry average. Meanwhile, other industry players like McDonald's, Dutch Bros and Domino's are trading at 6.67X, 4.35X and 1.93X, respectively.

P/S (F12M)

Image Source: Zacks Investment Research

Wrapping Up

Starbucks appears to offer an attractive opportunity for long-term investors despite its recent share-price weakness. The company is showing clear signs that its turnaround strategy is gaining traction, with improving customer traffic, stronger engagement through the rewards program, successful menu innovation and meaningful enhancements to the in-store experience.

Management's focus on operational efficiency, service quality and cost discipline is beginning to translate into better financial performance, while international markets, particularly China, provide an additional avenue for growth. Coupled with a globally recognized brand, a loyal customer base and a valuation that remains reasonable relative to many restaurant peers, Starbucks seems well-positioned to benefit as its turnaround progresses. For investors willing to look beyond near-term market concerns, the recent pullback could represent an appealing entry point into a company with improving fundamentals and multiple drivers of sustainable growth.

Starbucks currently has a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Starbucks Corporation (SBUX): Free Stock Analysis Report

McDonald's Corporation (MCD): Free Stock Analysis Report

Dutch Bros Inc. (BROS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).