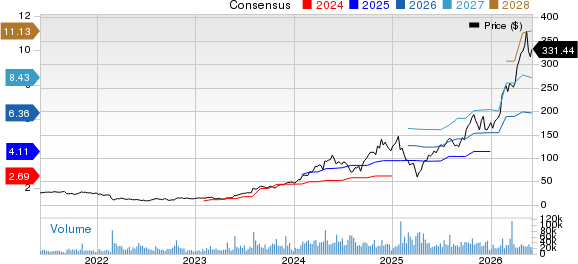

Vertiv VRT shares have rallied 195% in the past year compared with the broader Zacks Computer & Technology sector’s rise of 55.9%. The Zacks Computers - IT Services industry decreased 22.6% over the same period.

Vertiv’s shares have also outperformed its peers, which include Super Micro Computer SMCI and Amphenol APH. Both Super Micro Computer and Amphenol are expanding their capabilities in the AI and data center infrastructure markets. Shares of Super Micro Computer and Amphenol have rallied 7.1% and 60.7%, respectively, in the year.

The outperformance of VRT stock can be attributed to its rich partner base and extensive product portfolio spanning thermal systems, liquid cooling, UPS, switchgear, busbars and modular solutions. Vertiv remains leveraged to rising data center power and thermal needs as AI deployments drive higher infrastructure density and faster build cycles.

VRT Stock's Performance

Image Source: Zacks Investment Research

Vertiv Gains From AI Demand and Strategic Acquisitions

Vertiv’s expanding portfolio and acquisitions are contributing to margin stability and growth. In the first quarter of 2026, Vertiv reported 30% year-over-year revenue growth, with organic sales up 23%. Adjusted operating margins expanded 430 basis points, and adjusted free cash flow more than doubled compared to the prior year.

Acquisitions have played an important role in further expanding Vertiv’s footprint. Acquisitions such as PurgeRite (fluid management and liquid cooling) and BMarko Structures (modular infrastructure) expanded Vertiv's technology portfolio and service capabilities, positioning the company better to serve the evolving needs of data center customers. In the first quarter of 2026, acquisitions contributed 4% to revenues.

The company’s ability to deliver integrated, prefabricated solutions like OneCore and SmartRun is particularly valued as customers seek faster deployment and greater efficiency.

Building on this momentum, the company recently introduced the first converged physical infrastructure digital twin for NVIDIA NVDA Omniverse DSX. This solution integrates VRT’s SmartRun platform into NVIDIA’s AI factory design environment.

The company allows data center operators to model, simulate, and validate power, cooling, and infrastructure systems as a single digital replica before deploying them. The digital twin reduces design changes, lowers integration risks, improves collaboration among teams and speeds up AI factory deployment by shifting from traditional document-based planning to a model-based approach. This launch is the first step in Vertiv’s larger plan to create scalable, simulation-ready infrastructure for next-generation AI factories.

VRT Benefits From Expanding NVIDIA Partnership

Vertiv’s partnership with NVIDIA has been a key catalyst. In March 2026, Vertiv announced its partnership with NVIDIA to improve the combined physical infrastructure for AI factories. This will be done through DSX SimReady digital power and cooling assets, standardized 12.5MW modular building blocks, Vertiv OneCore and system-level designs that integrate power, cooling and controls.

The goal is to reduce deployment complexity, speed up readiness, improve scalability and enable digitally validated, high-performance AI infrastructure from the grid to the chip level.

VRT Initiates Positive 2Q26 Guidance

Vertiv is benefiting from its strong portfolio and rich partner base, which will continue to benefit the company’s top-line growth.

For the second quarter of 2026, revenues are expected to be between $3.25 billion and $3.45 billion. Organic net sales are expected to increase in the 20% to 24% range. The Zacks Consensus Estimate for Vertiv’s second-quarter 2026 revenues is pegged at $3.37 billion, suggesting growth of 27.69% year over year.

VRT expects second-quarter 2026 non-GAAP earnings per share between $1.37 and $1.43 per share. The Zacks Consensus Estimate for second-quarter 2026 earnings is currently pegged at $1.42 per share, which has declined by a penny over the past 30 days. The figure indicates a year-over-year increase of 49.47%.

Vertiv Holdings Co. Price and Consensus

Vertiv Holdings Co. price-consensus-chart | Vertiv Holdings Co. Quote

Vertiv Stock Is Trading at a Premium

Vertiv is currently overvalued, as suggested by a Value Score of D.

In terms of the trailing 12-month Price/Book, Vertiv is currently trading at 29.99X compared with the broader Computer and Technology sector’s 10.63X.

VRT's Valuation

Image Source: Zacks Investment Research

Conclusion

Vertiv is benefiting from its strong portfolio and rich partner base, which are driving order growth. These factors justify the company’s premium valuation.

Vertiv stock currently carries a Zacks Rank #2 (Buy) and has a Growth Score of A, a favorable combination that offers a strong investment opportunity, per the Zacks Proprietary methodology. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amphenol Corporation (APH): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Super Micro Computer, Inc. (SMCI): Free Stock Analysis Report

Vertiv Holdings Co. (VRT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).