The meteoric rise of Micron Technology (MU) to a market capitalization of more than $1 trillion has been a spectacle to watch, with the artificial intelligence (AI)-fueled rally backed by robust growth and clear demand visibility. For the second quarter of fiscal 2026, Micron reported 196% year-over-year (YOY) revenue growth to $23.86 billion. For the same period, operating income and cash flow from operations were $16.46 billion and $11.9 billion, respectively. These headline numbers put Micron's growth trajectory and cash flow potential in the spotlight.

For Q3, Micron also guided for revenue of $33.5 billion, plus or minus $750 million. Management believes that gross margin expansion will sustain as well. Considering the trend, annualized operating cash flow in excess of $50 billion is in the cards. Therefore, as markets close in on Q3 earnings on June 24, there are reasons for investors to remain optimistic. Key factors to watch include any potential revision to fiscal 2026 guidance and the company’s assessment of the demand-supply scenario for the next 12 to 24 months.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For investors, it would make sense to remain on the sidelines before considering any fresh exposure to MU stock. However, any potential near-term correction would present a good buying opportunity in an industry with multi-year tailwinds.

About Micron Stock

Founded in 1978 and headquartered in Boise, Idaho, Micron is a developer, manufacturer, and seller of memory and storage products. The company’s global product portfolio includes DRAM, NAND, NOR, solid-state devices, graphics and high bandwidth memory (HBM), and managed NAND and multi-chip packages.

Micron’s innovation provides an edge in an intensely competitive market with the company having a large portfolio of active patents both in the U.S. and abroad. For fiscal 2025, Micron reported revenue of $37.38 billion. The company’s four business segments include cloud memory, data center, mobile and client, and automotive and embedded.

Micron is positioned to benefit from the AI revolution through its memory and storage solutions. To put things in perspective, Micron expects the DRAM and NAND demand-supply scenario to remain tight through 2026. Even beyond 2026, the demand-supply mismatch will likely translate into healthy growth and robust margins.

Amid structural industry tailwinds and robust growth, MU stock has skyrocketed 293% in the last six months.

www.barchart.com

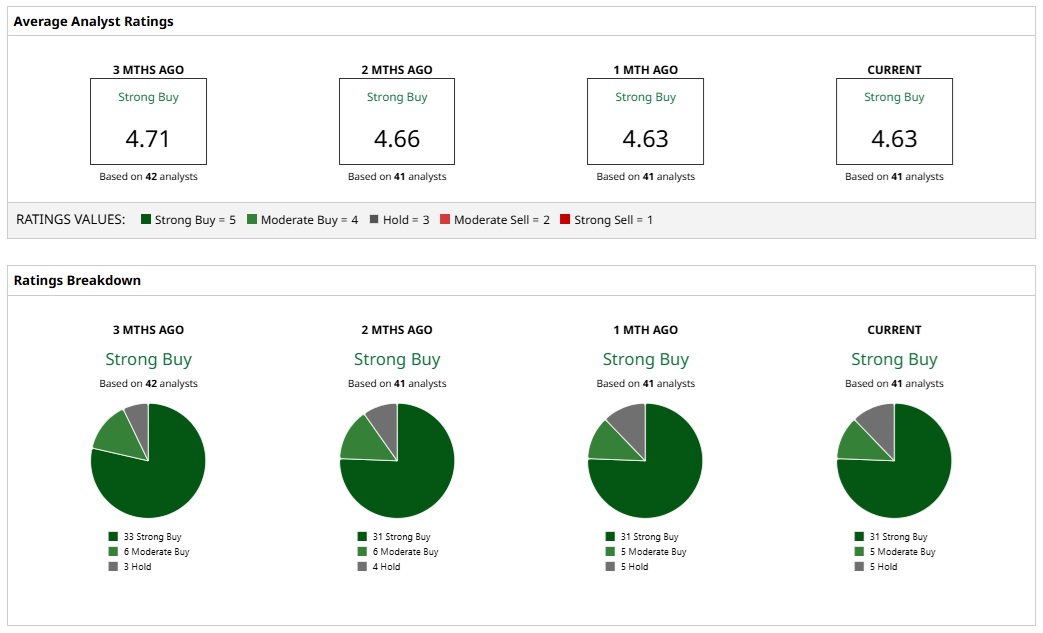

www.barchart.com What Do Analysts Say About MU Stock?

Based on 41 analysts with coverage, MU stock has a consensus “Strong Buy” rating. While 31 analysts have a “Strong Buy” rating for MU stock, five analysts have a “Moderate Buy" rating and five have a “Hold” rating.

The mean price target of $755.63 represents potential downside of roughly 19% from current levels. However, the most bullish price target of $1,750 suggests that MU stock could climb as much as 89% from here.

www.barchart.com

www.barchart.com Is Micron Stock Overvalued?

Micron recently surpassed the $1 trillion valuation mark and the stock has gone ballistic this year with returns of 777% in the last 52 weeks. Some correction after a massive rally seems likely, but MU stock is not in a phase of euphoria.

To put things into perspective, MU trades at a forward price-to-earnings (P/E) ratio of 18.4 times. Further, according to analyst estimates, earnings growth is expected to be strong for fiscal 2026 and fiscal 2027 at 665% and 74%, respectively. With both industry tailwinds and Micron’s capex to meet impending demand, growth will likely sustain.

Recently, Susquehanna increased its price target for Micron stock to $1,750. The key factor behind the price hike was continued strength in memory and storage. Raymond James also recently increased its price target for MU stock to $1,100 with an “Outperform” rating. Analysts noted that the industry has “never seen a similar demand environment."

Overall, Micron is well positioned for sustained growth and cash flow upside. With Q3 results due later this month, another strong quarter with optimistic guidance should be on the horizon.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dear Micron Stock Fans, Mark Your Calendars for June 24 TTM Technologies Stock Is Up 450% in a Year and Could Still Run Higher Intel Just Landed a Major Foxconn AI Win. INTC Stock Needs Proof, Not Hope, to Climb Further. CELH Stock Alert: What to Know as Celsius Faces Child Safety Investigation