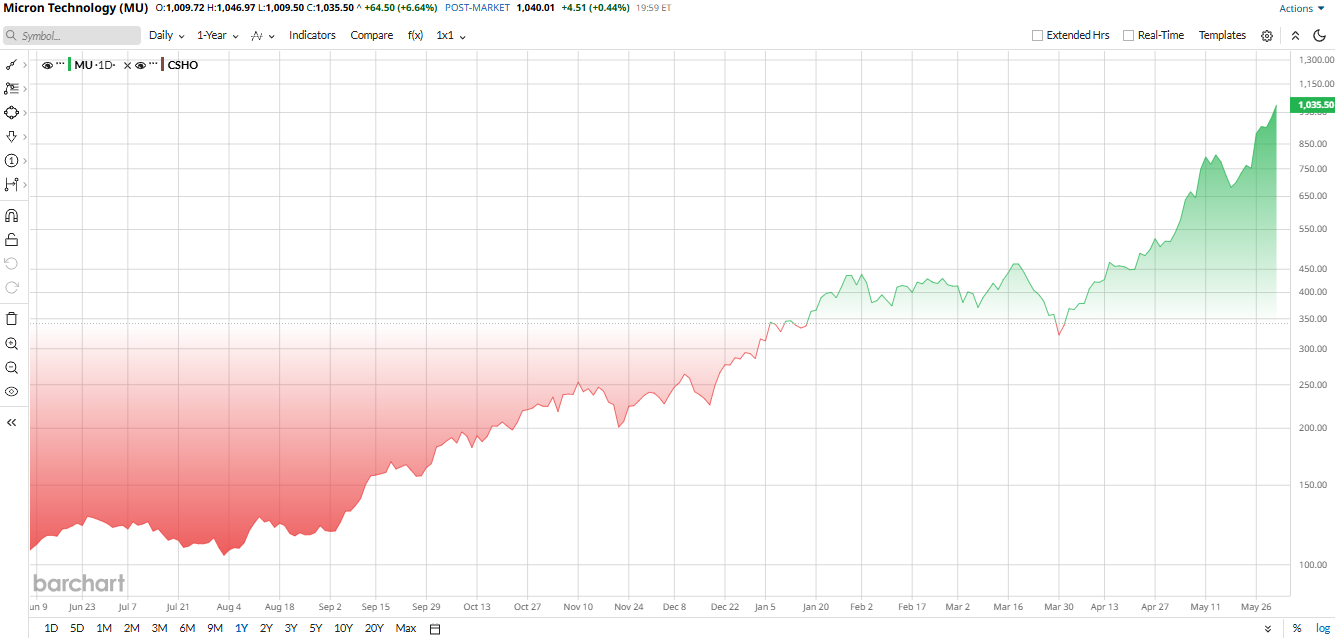

Memory chip stocks have been on fire this year, with Micron (MU) leading the charge. Advanced AI servers have sent demand soaring, making chips that were once deemed “boring” the hottest part of tech. MU stock has climbed almost 750% over the past 52 weeks as investors bet on an extended memory supercycle. Raymond James recently added to the momentum by lifting its price target to $1,100 from $530 and reiterating an “Outperform” rating ahead of the June 24 earnings report. In response, the stock rose more than 6% and moved above the $1,000 mark, although shares now trade closer to the $900 level.

Raymond James' bullish call rests on more than a fast-moving share price. Micron said in March that second-quarter revenue nearly tripled from a year earlier and it expects another record-setting quarter, with management pointing to strong AI data-center demand, tight industry supply, and improving visibility from customers.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For investors looking for a way to play the AI memory boom, Micron is now one of the market’s most closely watched names.

Why Micron Keeps Winning

Micron has been grabbing headlines beyond the numbers. Just weeks ago, the company celebrated production of 1-alpha (1α) DRAM — the most advanced memory ever made in the United States — at its plant in Manassas, Virginia. This DRAM boosts domestic chip supply for industries like auto, defense, and AI, and underscores Micron’s multibillion U.S. investment plan. Earlier in 2026, Micron was also added to the S&P 100 Index ($OEX). Inclusion in this blue-chip index brings new buyers from index funds and boosts MU stock’s visibility. These developments, plus dozens of contract wins to supply high-bandwidth memory chips for top AI companies, reinforce Micron’s central role in the AI boom.

Technically, Micron has been in a powerful uptrend. The stock sits well above its 50-day and 200-day moving averages, signaling a breakout. Over the past 12 months, MU has seen huge returns fueled by record sales and profits. A year ago, shares traded below $300; the stock is now near $900 and climbing.

Market-wide, Micron has handily beaten the S&P 500 ($SPX) and semiconductor peers in 2026. Sector-wise, Micron still trades at rich levels, with a price-to-book (P/B) ratio of 16.8 times, significantly higher than the sector median. However, its forward price-to-earnings (P/E) ratio of 18.4 times is lower than the sector median, indicating some attractive pricing aspects.

www.barchart.com

www.barchart.com The Raymond James Upgrade Stirs the Bull Case

The Raymond James note on June 1 helped fuel the latest rally. It came after Micron’s blowout Q2 results and as excitement builds for fiscal Q3.

In the note, analysts led by Melissa Fairbanks cited Micron’s massive momentum and raised their target to $1,100. MU stock immediately jumped more than 6% on the news, hitting fresh highs by day’s end.

Raymond James isn’t alone, however, as recent weeks have seen several firms lift their targets. For example, HSBC and Melius both recently moved their targets up to $1,100 as well, while Citi boosted its target to $840. In short, Wall Street’s mood has flipped bullish.

Micron Delivered a Beat-and-Raise Quarter

Micron's Q2 was a blockbuster. Revenue hit $23.86 billion, nearly triple the year-ago level. The spike was broad-based; DRAM sales alone were about $18.8 billion while NAND flash revenue came to $5 billion, reflecting ferocious demand from cloud and AI data centers.

Net income exploded, too. Micron reported $13.79 billion in profit, or $12.20 per share on an adjusted basis, up from just $1.58 billion a year earlier, or $1.56 per share on an adjusted basis. Free cash flow was enormous at about $6.9 billion. Micron ended the period with roughly $16.7 billion in cash and equivalents on the balance sheet. In short, the quarter shattered records across the board.

CEO Sanjay Mehrotra summed it up plainly in the report: “Micron set new records across revenue, gross margin, EPS, and free cash flow in fiscal Q2.” Mehrotra added that a “strong demand environment, tight industry supply, and […] strong execution” drove the results. With AI taking off, the CEO noted that memory has become a “strategic asset” for customers. Accordingly, Micron’s board voted to raise the dividend by 30% in Q2 as a sign of confidence.

Looking ahead, Micron offered bullish guidance. For Q3, the company foresees about $33.5 billion in revenue with roughly 81% gross margins. That level of sales would mark another massive year-over-year (YOY) jump. The company also guided for adjusted EPS of around $18.90. Management expects “significant records again in fiscal Q3,” implying the recent rally isn’t a one-off.

Wall Street is even more optimistic. Analysts now expect fiscal 2026 earnings of $58.79 per share, up 665% YOY, as well as earnings of $102.26 per share for fiscal 2027. Expectations are sky-high after the blowout quarter in March.

What Do Analysts Say About MU Stock?

The chatter among analysts is overwhelmingly positive. UBS raised its target to $1,625 from $535 in late May, arguing that new long-term memory supply deals will keep prices high and profits stable. UBS even noted there’s “no reason” Micron shouldn’t trade like a high-flying chipmaker such as Nvidia (NVDA), given AI demand. Morgan Stanley is also bullish on MU stock, keeping an “Overweight” rating with a $1,050 price target.

On the other hand, Goldman Sachs remains cautious. The firm is effectively a lone outlier on MU stock with a price target closer to $400 per share, warning that memory remains cyclical.

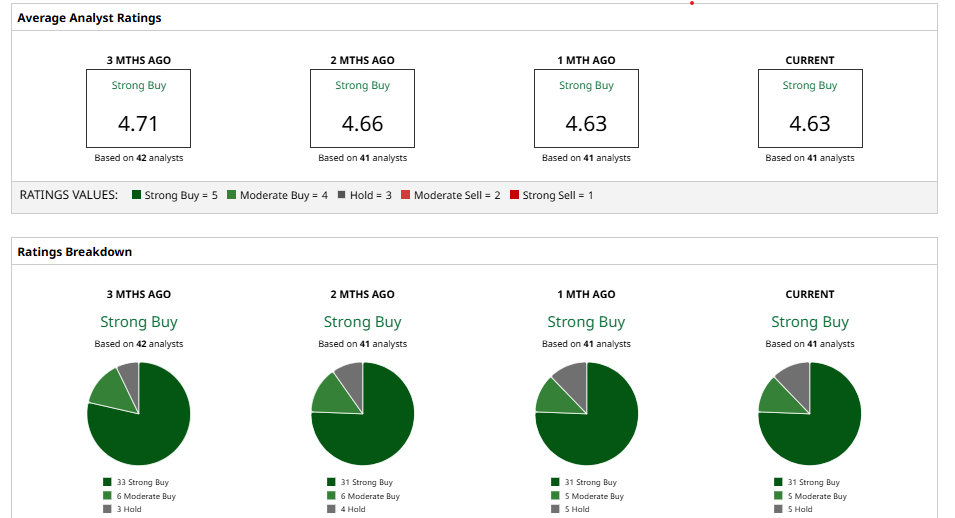

Overall, most Wall Street analysts see more upside ahead, praising Micron’s execution and pointing to multi-year AI chip contracts. MU stock has a consensus “Strong Buy" rating based on 41 analysts with coverage. The average target of $755.63 has already been surpassed, pointing to potential downside from current levels. However, the Street-high target of $1,750 implies roughly 100% potential upside from here.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Nvidia Acquires Kumo AI for $400 Million. What That Means for NVDA Stock. Why 1 Veteran Analyst Doubled Her Micron Stock Price Target for 2026 Why Cathie Wood and Berkshire Hathaway Both Love Google Stock Here UnitedHealth Stock Jumps on Upgrade From Bank of America. UNH Is No Longer Just an Insurance Company.