Marsh & McLennan Companies, Inc. MRSH is well positioned for growth, driven by product innovation, expansion into emerging markets and strategic acquisitions.

Marsh — with a market capitalization of $79.9 billion — is a global professional services firm focused on risk, reinsurance, people-related consulting and management consulting services. In the year-to-date period, the stock has fallen 10.9% compared with the industry’s 16.6% decline.

Courtesy of solid prospects, MRSH currently carries a Zacks Rank #3 (Hold).

Where Do Estimates for MRSH Stand?

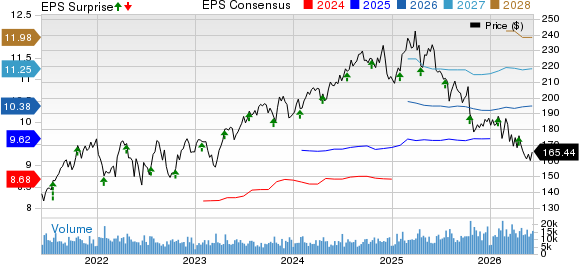

The Zacks Consensus Estimate for Marsh’s 2026 earnings is pegged at $10.38 per share, indicating a 6.5% year-over-year rise, which has been revised upward over the past 30 days. Furthermore, the consensus mark for revenues is pegged at $28.3 billion for 2026, implying a 4.9% year-over-year gain. It beat earnings estimates in each of the past four quarters, with an average surprise of 3.9%.

Marsh Price, Consensus and EPS Surprise

Marsh price-consensus-eps-surprise-chart | Marsh Quote

MRSH’s Growth Drivers

Marsh continues to benefit from strong demand across its Risk & Insurance Services, and Consulting businesses despite softer insurance pricing and lower fiduciary interest income. In the first quarter of 2026, its total revenues rose 7.6% year over year, supported by solid new business generation, improving momentum at Marsh Risk, continued expansion in Mercer’s health and wealth segments, and healthy demand for management consulting services.

AI remains a key pillar of Marsh’s strategy. The company is expanding AI-powered products and analytics tools to enhance client insights, improve service delivery and create new revenue opportunities. Alongside this, the Thrive program is driving operational improvements through automation, process simplification and technology modernization, with savings being reinvested in talent, innovation and growth-focused initiatives.

Marsh continues to use acquisitions as a complement to organic growth, focusing on opportunities that expand capabilities and strengthen its market position. The company maintains an active M&A pipeline and recently announced an agreement to acquire AltamarCAM to increase and expand its capabilities in the private markets platform. Alongside larger strategic opportunities, Marsh remains focused on its disciplined “string of pearls” approach, pursuing targeted acquisitions that enhance capabilities, deepen client relationships and broaden its service offerings. In June 2026, it completed the acquisition of TriBridge Partners, expanding its presence in the DC-Baltimore market.

MRSH remains committed to enhancing shareholder value through dividends and share buybacks. Its current dividend yield is 2.2%, higher than the industry average of 1.8%. In the first quarter of 2026, the company rewarded its shareholders with share buybacks worth $750 million.

Risk Factors

However, there are some factors that investors should keep a careful eye on.

Marsh is facing rising costs due to higher wages, talent retention efforts and acquisition-related expenses, with total expenses increasing 15.6% year over year in the first quarter of 2026. These pressures could limit margin expansion and weigh on earnings growth.

The company also carried a significant debt burden of $18.9 billion at the end of March 2026, compared with cash and cash equivalents of $1.6 billion. Its total debt-to-capital of 56.1% is higher than the industry average of 49.9%.

The company’s valuation remains stretched at the current level. Marsh currently has a forward 12-month P/E of 15.38X, higher than the industry’s average of 13.46X.

Better-Ranked Players

Some better-ranked stocks in the business services space are Sezzle Inc. SEZL, Dave Inc. DAVE and Green Dot Corporation GDOT, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Sezzle’s current-year earnings is pinned at $5.09 per share and has witnessed one upward revision in the past 30 days against no movement in the opposite direction. Sezzle beat earnings estimates in each of the trailing four quarters, with the average surprise being 17.4%. The consensus estimate for current-year revenues is pegged at $592.6 million, implying 31.6% year-over-year growth.

The Zacks Consensus Estimate for Dave’s current-year earnings is pinned at $16.17 per share and has witnessed two upward revisions in the past 30 days against no movement in the opposite direction. Dave beat earnings estimates in each of the trailing four quarters, with the average surprise being 45.8%. The consensus estimate for current-year revenues is pegged at $713.7 million, implying 28.8% year-over-year growth.

The Zacks Consensus Estimate for Green Dot’s current-year earnings is pinned at $1.68 per share and has witnessed one upward revision in the past 30 days against no movement in the opposite direction. Green Dot beat earnings estimates in three of the trailing four quarters. The consensus estimate for current-year revenues is pegged at $2.2 billion, implying 8.3% year-over-year growth.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dave Inc. (DAVE): Free Stock Analysis Report

Green Dot Corporation (GDOT): Free Stock Analysis Report

Sezzle Inc. (SEZL): Free Stock Analysis Report

Marsh (MRSH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).