Shares of SoFi Technologies (SOFI) have lost significant value, falling more than 49% from their 52-week high of $32.73. Concerns about valuation, macroeconomic uncertainty, and a shifting revenue mix have weighed on investor sentiment.

However, with SOFI stock now trading well below its peak, is this the best time to accumulate SoFi shares?

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Into SOFI Stock’s Decline

SoFi delivered strong quarterly numbers for Q1 2026 as it added more members, drove product adoption among existing customers, and saw loan originations accelerate. These factors helped drive stronger top-line growth, highlighting the continued demand for SoFi’s financial products and services.

However, the company’s revenue mix raised concerns. A key concern emerged from the company’s higher reliance on its lending business. While lending can generate meaningful revenue growth, it is capital-intensive and exposes the company to credit risks. This shift contrasts with SoFi’s long-term strategy of expanding higher-margin, capital-light revenue streams such as its technology platform and financial services segments.

Notably, SoFi’s technology platform business experienced a revenue decline following the loss of a major client. While this was anticipated, as management had earlier communicated the exit of a large customer, it raised questions about the company’s efforts to diversify its business away from lending.

For instance, SoFi’s combined revenue from the financial services and technology platform segments totaled $503.6 million in the first quarter, representing a 24% year-over-year (YoY) increase and accounting for just under half of total revenue. While that growth remains healthy, it marks a significant slowdown from the fourth quarter of 2025, when those same businesses generated $579 million in revenue, grew 61% YoY, and contributed 57% of total company revenue.

www.barchart.com

www.barchart.com SoFi’s Growth Prospects Remain Solid

While the recent slowdown in SoFi's capital-light business has raised concerns, the company's broader growth trajectory remains solid. Its operating metrics remain solid, supported by strong member growth, increasing product adoption, and diversified revenue streams.

SoFi's customer acquisition engine remains solid. During the first quarter, SoFi added a record number of new members, while product adoption reached new highs. Management expects this momentum to continue, projecting member growth of at least 30% YoY in 2026. Importantly, many of SoFi's newer products are adopted by its existing member base, creating significant cross-selling opportunities and lowering customer acquisition costs.

While SoFi’s lending business continues to perform well, its focus on diversifying revenue streams augurs well for growth. For instance, SoFi’s Financial Services segment remains a major growth driver. First-quarter revenue rose 41% YoY to $429 million, driven by a 55% jump in noninterest income to $201 million.

Several businesses within the segment delivered particularly strong results. Interchange revenue climbed 54% YoY, supported by higher annualized spending across SoFi Money and credit card products. Brokerage fee revenue more than doubled from the prior year, highlighting growing engagement across the company's investment platform.

The biggest growth engine is SoFi's Loan Platform Business (LPB), which generates fee income without retaining credit risk. Capital markets activity remained robust during the quarter, with SoFi selling or transferring $3.8 billion of personal and home loans through the platform. The company also secured $3.6 billion of new commitments from three additional partners, expanding future growth opportunities.

One of SoFi's competitive advantages is its ability to allocate loan originations between its balance sheet and LPB channels. While balance sheet lending generates higher lifetime revenue, its LPB transactions provide capital-light fee income. This flexibility allows management to optimize profitability.

While SoFi’s capital-light business is expected to sustain solid growth, the company’s deposit base continues to strengthen. Total deposits increased by $2.7 billion during the quarter to reach $40.2 billion. Growing deposits provide a lower-cost source of funding, improve net interest margins, and support long-term earnings growth.

The Bottom Line

SOFI stock's recent selloff has been driven by investor concerns over its lending exposure and slower growth in one of its capital-light businesses. However, SoFi continues to add members at an impressive pace, deepen customer engagement through higher product adoption, and generate strong momentum in its financial services business led by solid growth in its LPB.

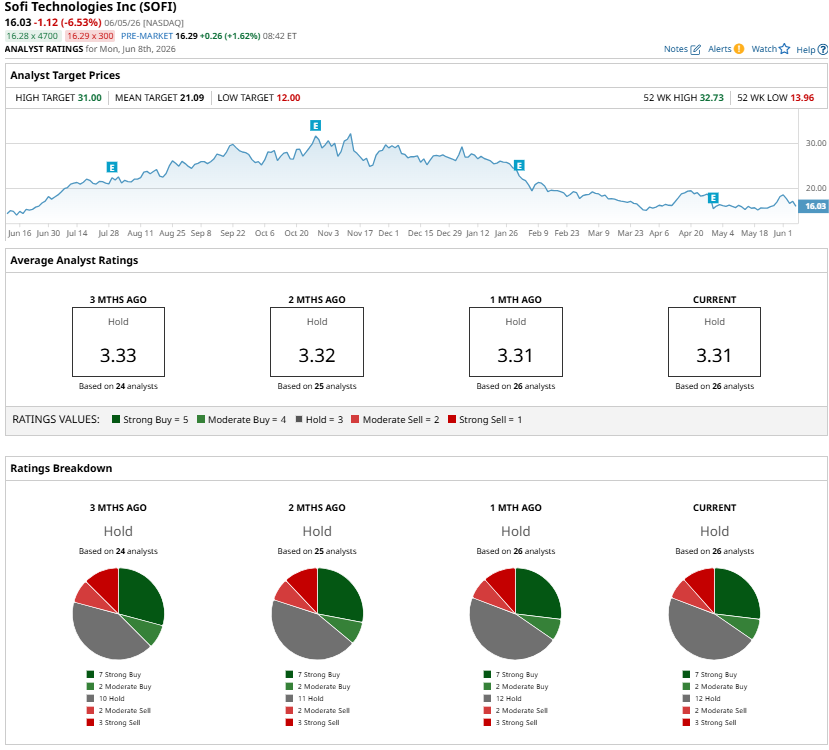

Wall Street analysts currently maintain a "Hold" consensus rating on SOFI stock. However, after a sharp 49% pullback from its highs, SOFI is an attractive long-term investment with significant runway ahead.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

As Bitcoin Prices Plunge, Wall Street Is Losing Faith in Coinbase Stock Down 49%, SoFi Stock Is an Attractive Buy Here for Long-Term Investors Broadcom Stock Dropped on Guidance Concerns, Yet Analysts Still See Significant Upside Ahead Investors Buying Unusually Heavy Volume of Strategy, Inc. Call Options - Bullish on Bitcoin