Intel Corporation (INTC) has certainly staged one of the market’s most dramatic turnarounds over the past year, transforming itself into a stock that many investors are finding hard to overlook. The chip giant has doubled down on innovation, accelerated its push to become a leading foundry player, and expanded its presence in the red-hot artificial intelligence (AI) market. Aggressive cost-cutting efforts, sweeping restructuring initiatives, new leadership, the continued buildout of Intel Foundry Services (IFS), and a string of high-profile partnerships have all helped reshape the company’s outlook.

Confidence in the turnaround received another major boost when the U.S. federal government acquired nearly a 10% stake in Intel last year, highlighting the company’s strategic importance and reinforcing faith in its long-term growth ambitions. The result has been nothing short of extraordinary, with Intel’s shares delivering triple-digit gains over the past year. However, even as the turnaround story gathers momentum, recent insider selling has caught investors’ attention.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Naga Chandrasekaran, Intel’s Executive Vice President, Chief Technology and Operations Officer, and General Manager of the Intel Foundry organization, recently sold 21,024 shares, reducing his direct ownership stake by roughly 9.27%. The transaction, valued at approximately $2.49 million, was executed at $118.28 per share and leaves him with 205,852 shares. While insider selling is not uncommon and can occur for a variety of personal financial reasons, the transaction is still likely to raise questions among investors about whether there is more to the story.

So, should shareholders view it as routine portfolio management, or be concerned instead?

About Intel Stock

For decades, Intel Corporation stood as one of the defining forces in the global semiconductor industry. Founded in 1968 and headquartered in Santa Clara, the company built its reputation by designing and manufacturing the processors that power millions of personal computers and data centers around the world. Today, however, Intel is far more than a PC chipmaker.

Its operations span multiple high-growth markets, including client computing, data center and AI processors, networking and edge computing, and IFS, its rapidly expanding contract semiconductor manufacturing business. As AI and advanced computing reshape the technology landscape, Intel is pursuing an ambitious transformation, aiming to establish itself as both a leading chip designer and a world-class semiconductor manufacturer.

But the company’s current momentum is a sharp contrast to where it stood just a few years ago. While fabless rivals such as Nvidia (NVDA) and Advanced Micro Devices (AMD) surged ahead during the AI boom, Intel struggled to keep pace, steadily losing market share and falling behind in one of the industry’s most important growth opportunities. The former semiconductor powerhouse found itself battling slowing growth, shrinking margins, declining earnings, and waning investor confidence.

Conditions became so challenging that Intel slashed its dividend in 2023 before suspending it altogether in 2024. Its stock continued to slide, billions of dollars in market value disappeared, and many investors concluded that the company had missed the biggest technological shift of the decade. But the story looks dramatically different in 2026.

Fueled by renewed investor confidence, growing strategic support, advances in AI-focused technologies, and progress in next-generation semiconductor manufacturing, Intel has rapidly transformed from one of the market’s biggest laggards into one of its most closely watched turnaround plays. With a market capitalization of approximately $542.40 billion, Intel Corporation has rewarded shareholders with returns that few stocks can match.

Over the past year, the chipmaker has surged an eye-popping 383%, leaving the broader S&P 500 Index ($SPX) and its 21.37% gain far behind. The rally has shown little sign of slowing in 2026, with Intel shares climbing another 189.16% year-to-date (YTD), compared to the market’s more modest 7.06% advance. Perhaps most remarkable of all, the stock has skyrocketed roughly 464% from its 52-week low of $18.97 reached last August, highlighting the scale of Intel’s transformation from one of the market’s biggest disappointments into one of its most remarkable comeback stories.

www.barchart.com

www.barchart.com Intel’s Q1 Earnings Snapshot

Intel’s improving financial performance is giving investors more reasons to believe that the company’s turnaround is real. On April 23, the chip giant delivered a surprisingly strong fiscal 2026 first-quarter earnings report, beating Wall Street’s expectations on nearly every major metric and triggering a massive 23.6% surge in the stock the following trading day. Revenue, gross margin, and earnings per share all came in above the high end of management’s guidance, marking Intel’s sixth straight quarter of outperforming its own forecasts.

The company reported non-GAAP revenue of $13.58 billion, up 7% year-over-year (YOY) and comfortably ahead of analysts’ consensus estimate of $12.39 billion. However, the biggest surprise came from the bottom line. Intel posted non-GAAP earnings of $0.29 per share, blowing past expectations of just $0.01 per share. The impressive earnings beat was fueled largely by aggressive cost-cutting initiatives and a more favorable mix of higher-margin products.

Nonetheless, Intel’s recovery remains a work in progress. On a GAAP basis, the company still reported a net loss of $3.7 billion, primarily due to one-time charges related to goodwill impairment and ongoing restructuring efforts. Even so, several key business segments showed encouraging signs of momentum.

One standout was Intel’s data center division, where the company is beginning to gain traction in AI-related workloads as demand for powerful CPUs continues to rise. Revenue in the segment jumped 22% YOY to $5.1 billion. Meanwhile, the Client Computing Group (CCG), home to Intel’s PC processor business, generated $7.7 billion in revenue, representing a modest 1% increase from the prior year. Intel’s ambitious foundry business also delivered encouraging results.

Revenue at Intel Foundry climbed 16% to $5.4 billion, reflecting growing interest in the company’s semiconductor manufacturing capabilities. While the segment remained unprofitable, its operating loss narrowed to $2.4 billion, improving by $72 million sequentially as stronger yields across Intel 4, Intel 3, and Intel 18A helped support gross margins. Those gains were partially offset by higher operating expenses as Intel deliberately increased investments in Intel 14A, aiming to support technology evaluations from both internal teams and prospective external customers.

Looking ahead, management struck an optimistic tone. Intel forecast second-quarter revenue between $13.8 billion and $14.8 billion, comfortably ahead of prior Wall Street expectations. The company also expects a non-GAAP gross margin of approximately 39%, as it continues balancing the significant costs of expanding its manufacturing footprint with the profitable ramp-up of its next generation of AI and consumer-focused chips.

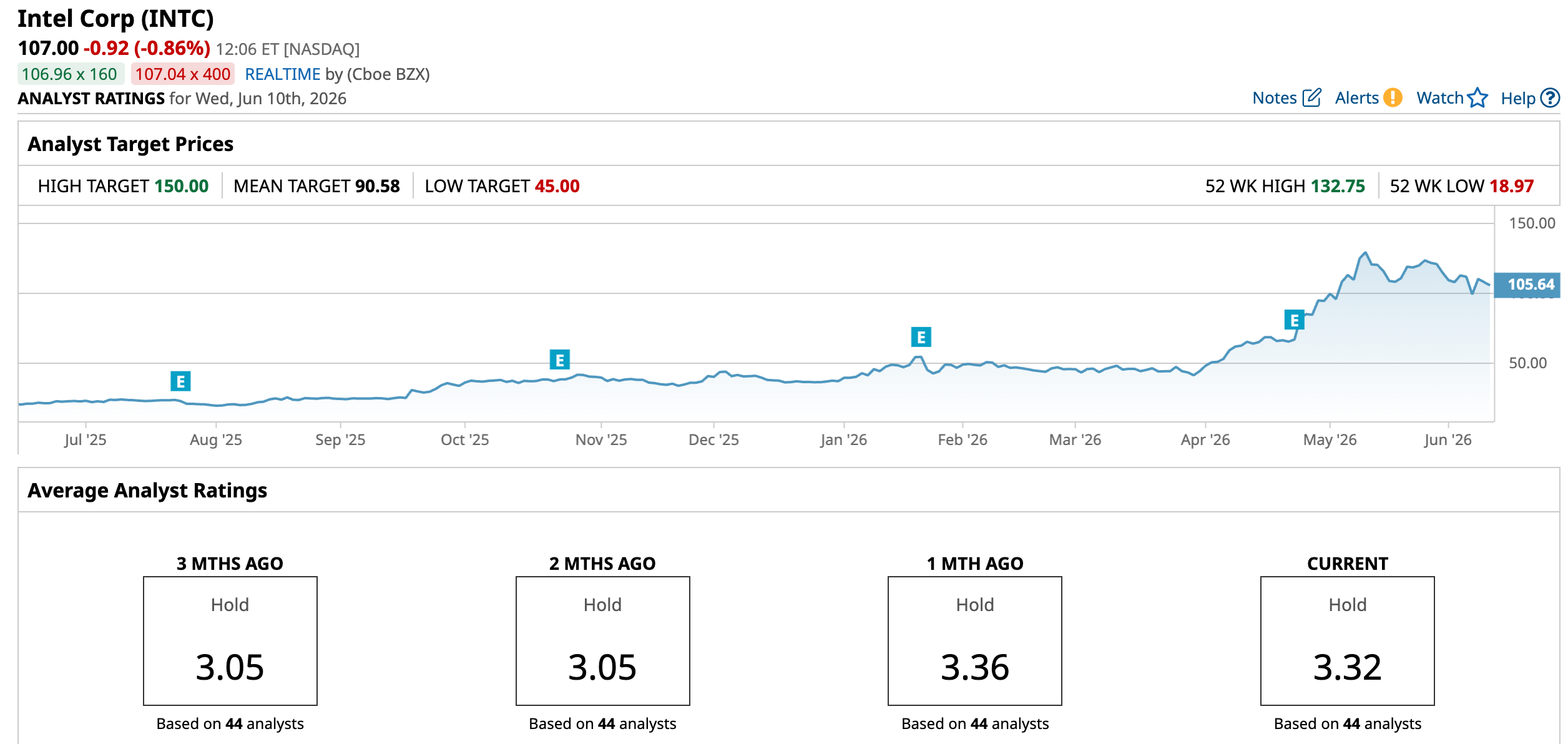

How Are Analysts Viewing Intel Stock?

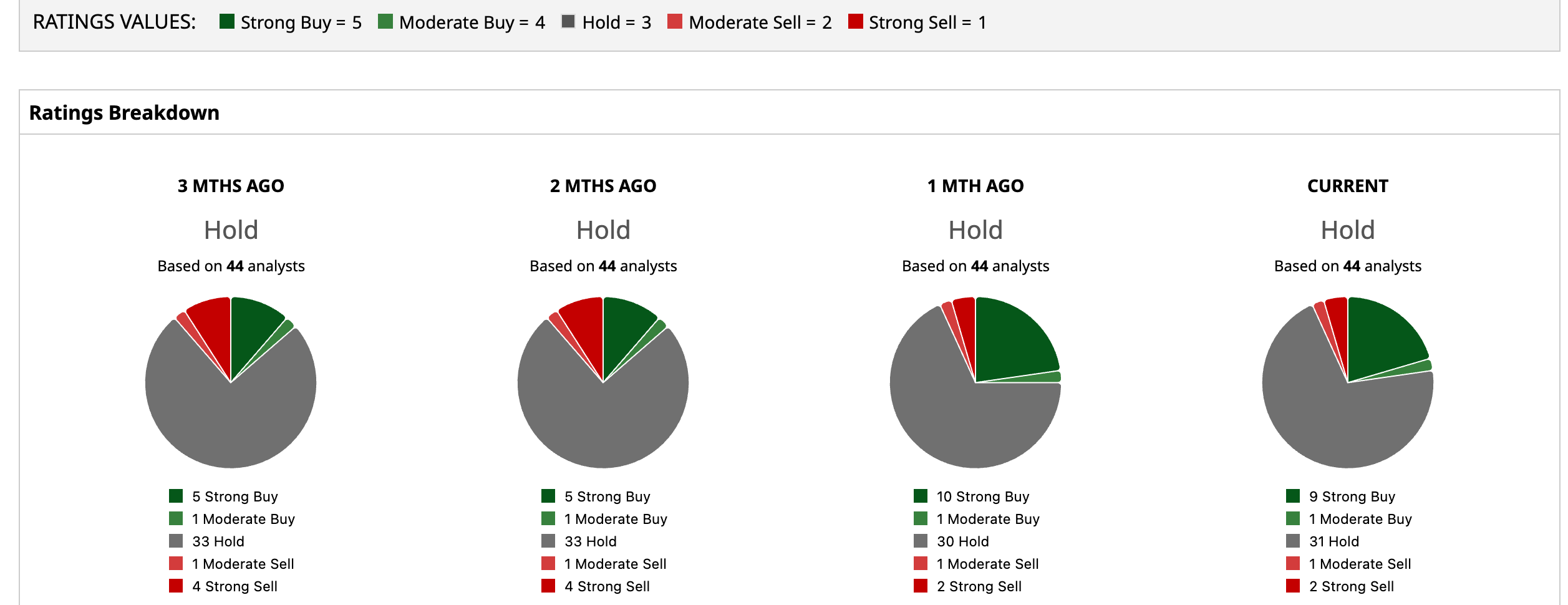

Despite Intel’s remarkable comeback, Wall Street remains surprisingly cautious. The stock currently carries a consensus “Hold” rating, suggesting that many analysts are still waiting for more proof that the turnaround can be sustained. Among the 44 analysts covering the stock, nine rate it a “Strong Buy,” one recommends “Moderate Buy,” 31 remain on the sidelines with “Hold” ratings, while one analyst rates it “Moderate Sell,” and two recommend “Strong Sell.”

Notably, the stock has already surged past the average analyst price target of $90.58, yet the most bullish target on Wall Street stands at $150, implying there could still be as much as 40.2% upside ahead if Intel’s turnaround story continues to gain momentum.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

The $500 Million Reason Redwire Stock Is Down Today 1 Intel Insider Just Sold Nearly 10% of His INTC Stock Super Micro Stock Drops on Dilution Fears, But a $39 Billion AI Order Could Spark a Turnaround. DraftKings Stock Soars as Predictions Volume Explodes. DKNG’s Next Growth Engine Might Just Be Getting Started.