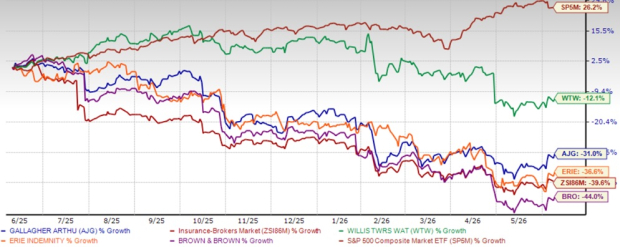

Shares of Arthur J. Gallagher & Co. AJG have lost 31% in the past year compared with the industry’s decline of 39.6%.

AJG shares have faced pressure as investors reacted to moderating organic growth and softer insurance pricing trends, which have reduced expectations for commission growth. Consequently, investors have reassessed the company's premium valuation. However, continued acquisition activity, growth in the Risk Management segment and a strong capital position should support long-term growth prospects.

Shares of other insurers like Erie Indemnity Company ERIE, Willis Towers Watson Public Limited Company WTW and Brown & Brown, Inc. BRO have lost 36.6%, 12.1% and 44%, respectively, in the said time frame.

1-Year Price Performance: AJG, ERIE, WTW, BRO, Industry & S&P 500

Image Source: Zacks Investment Research

AJG’s Growth Projection Encourages

The Zacks Consensus Estimate for Arthur J. Gallagher’s 2026 EPS indicates a year-over-year increase of 24.1%. The consensus estimate for revenues is pegged at $16.78 billion, implying a year-over-year improvement of 21.7%.

The consensus estimate for 2027 EPS and revenues indicates an increase of 11.3% and 9.3%, respectively, from the 2026 estimates.

Earnings of AJG grew 18.1% in the last five years, better than the industry average of 13.9%. The long-term earnings growth is expected to be 14.9%.

Optimistic Analyst Sentiment on AJG

Three analysts have raised estimates for 2026 and 2027 over the past 30 days, against no downward movement. Thus, the Zacks Consensus Estimate for 2026 and 2027 has moved 0.7% and 0.9% north, respectively, during this time.

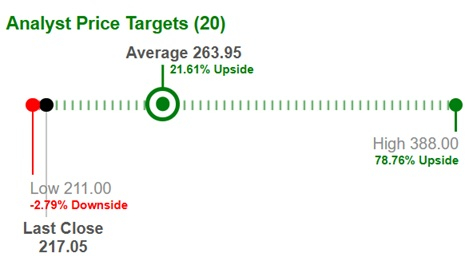

Target Price Reflects Potential Upside

Based on short-term price targets offered by 20 analysts, the Zacks average price target is $267.05 per share. The average indicates a potential 21.6% upside from the last closing price.

Image Source: Zacks Investment Research

Factors Impacting AJG

Arthur J. Gallagher is growing through mergers and acquisitions. Revenue growth rates generally ranged from 5% to 15% for acquisitions completed in 2026. In the first quarter of 2026, AJG completed eight acquisitions with estimated annualized revenues of about $49 million. Looking at the pipeline, AJG has around 40 term sheets signed or being prepared, representing about $400 million of annualized revenues.

AJG's growth is supported by continued performance in its Brokerage and Risk Management segments, which continue to drive organic revenue. The Risk Management business benefits from solid client retention, increased customer activity and higher claim volumes. Additionally, improving renewal premiums across major geographies, healthy new business production and expanding data and analytics capabilities position the company for continued growth. While AJG expects approximately 6% organic growth in 2026, driven by a strong sales pipeline and momentum across reinsurance, retail, bond and specialty insurance operations, organic growth has moderated from the double-digit levels achieved in prior periods.

AJG’s revenues are geographically diversified with strong domestic and international operations. International operations contribute about one-third of revenues. Given the number and size of its non-U.S. acquisitions, AJG expects international contributions to its total revenues to trend upward. Moreover, loss of clients or weakening of macro conditions in any particular country would not have any severe impact on the top line.

A robust capital position over the years reflects its financial flexibility. Banking on its capital position, AJG distributes wealth to shareholders through dividend hikes and share repurchases. In the first quarter of 2026, the dividend was raised by 7.6%, reflecting a three-year CAGR (2020-2025) of 7.6%. AJG’s current cash position, potential borrowing capacity and strong expected free cash flow position it well for its pipeline of M&A opportunities. Over the next two years, AJG expects to have $10 billion to fund M&A, before utilizing any stock.

Risks to Watch

Arthur J. Gallagher has been experiencing an increase in expenses due to higher compensation, depreciation, amortization and operating expenses which have been eroding margins.

Valuation of Arthur J. Gallagher remains stretched at the current level. Its forward price-to-earnings multiple of 15.58X is higher than the industry average of 14.43X.

Arthur J. Gallagher’s return on equity of 12.8% is lower than the industry average of 18.8%. This shows the company’s inefficiency in managing shareholders’ funds.

Conclusion

AJG continues to benefit from solid retention, improving renewal premiums, and inorganic growth. The Risk Management and Brokerage segments should continue to support its operations. A robust capital position over the years reflects its financial flexibility. Its impressive dividend history, optimistic analyst sentiment, and solid growth projections are other positives.

However, given the escalating expenses, moderate organic growth and unfavorable return on capital, it is better to stay cautious about this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Arthur J. Gallagher & Co. (AJG): Free Stock Analysis Report

Brown & Brown, Inc. (BRO): Free Stock Analysis Report

Erie Indemnity Company (ERIE): Free Stock Analysis Report

Willis Towers Watson Public Limited Company (WTW): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).