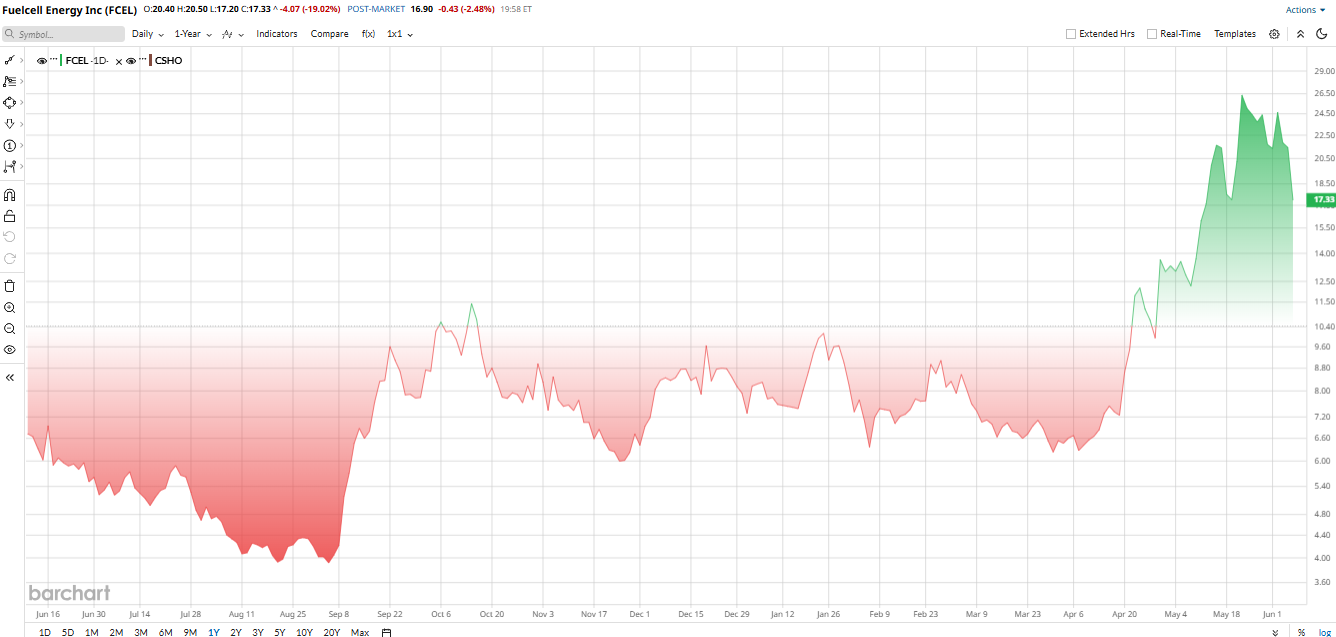

FuelCell Energy (FCEL) shares fell by double digits on Monday after the company reported fiscal second-quarter results that missed analyst estimates. It reported wider-than-expected losses and also a decline in revenue. This came despite a 267% sequential increase in its pipeline of potential AI data center projects.

FuelCell Energy has promoted its fuel-cell systems as a way to provide on-site power for AI data centers facing grid capacity constraints. However, investors focused on weaker-than-expected revenue and earnings, raising fresh concerns about execution and cash usage.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

The market reaction suggested that strong growth in the company’s project pipeline was not enough to offset near-term financial challenges.

FuelCell’s AI-Fueled Rally Faces a Valuation Test

The market has not been shy about FuelCell. Despite the 21% loss over the past week, the stock has more than doubled in 2026 from the $8.19 level seen at the end of January, powered by the AI data center theme and a wave of momentum buying across fuel-cell stocks. The move has also been fed by FuelCell’s expanding pipeline, which the company says is now heavily tied to data center demand.

Valuation is where the optimism starts to meet gravity. Barchart shows FuelCell with a market cap of $821 million, annual sales of $158 million, a price-to-sales ratio of 3, and a price-to-book ratio of 1.2. Those are not bargain numbers for a company that is still losing money, especially one with a 60-month beta of 2.42. The clean-energy rally has made the stock look more credible on the chart, but on the balance sheet, it still looks like a speculative growth trade rather than a classic value name.

www.barchart.com

www.barchart.com The Real Story Was Pipeline Growth

FuelCell Energy’s fiscal second-quarter results were a reminder that this remains one of the market’s most speculative AI-infrastructure plays. The company reported revenue of $35.6 million, down 5% year-over-year (YoY), as growth in some areas was offset by project timing and a challenging operating environment.

The bottom line was mixed. Net loss improved to $1.45 per share from a loss of $1.79 per share a year ago, marking the third consecutive quarter of narrowing losses. However, results still fell short of Wall Street expectations.

“Our pipeline is increasingly tied to AI and data-center opportunities,” CEO Jason Few said, emphasizing that more than 80% of the company’s project pipeline is now linked to those markets. That comment helps explain why investors looked past the earnings miss. The real story was FuelCell’s sales pipeline, which surged 267% sequentially to 4 gigawatts.

FuelCell also unveiled plans to expand its Torrington manufacturing facility to support up to 500 megawatts of annual production capacity, signaling confidence in future demand.

The company did not provide formal next-quarter or full-year revenue and earnings guidance. Analysts currently expect fiscal 2026 revenue of roughly $158 million and continued losses as FuelCell invests in growth. For now, the market appears willing to focus on pipeline growth and AI-related demand rather than near-term profitability.

What Fuelcell Is Doing Beyond the Headline

The company is not sitting still. In March, FuelCell announced it would expand its Utility Power Block output from approximately 100 MW to 350 MW and said its business-development pipeline had increased by 275% since February 2025, with most of the growth in customers from the data center space.

Additionally, it has announced a partnership with Sustainable Development Capital to investigate up to 450 MW of Fuel Cell power to serve the data center and other mission-critical loads. FuelCell is attempting a transition, and it certainly couldn't hurt to have a new board member on the board who understands how to run things in the days of artificial intelligence, such as John Livingston, a cybersecurity and McKinsey veteran.

Wall Street Still Wants Proof

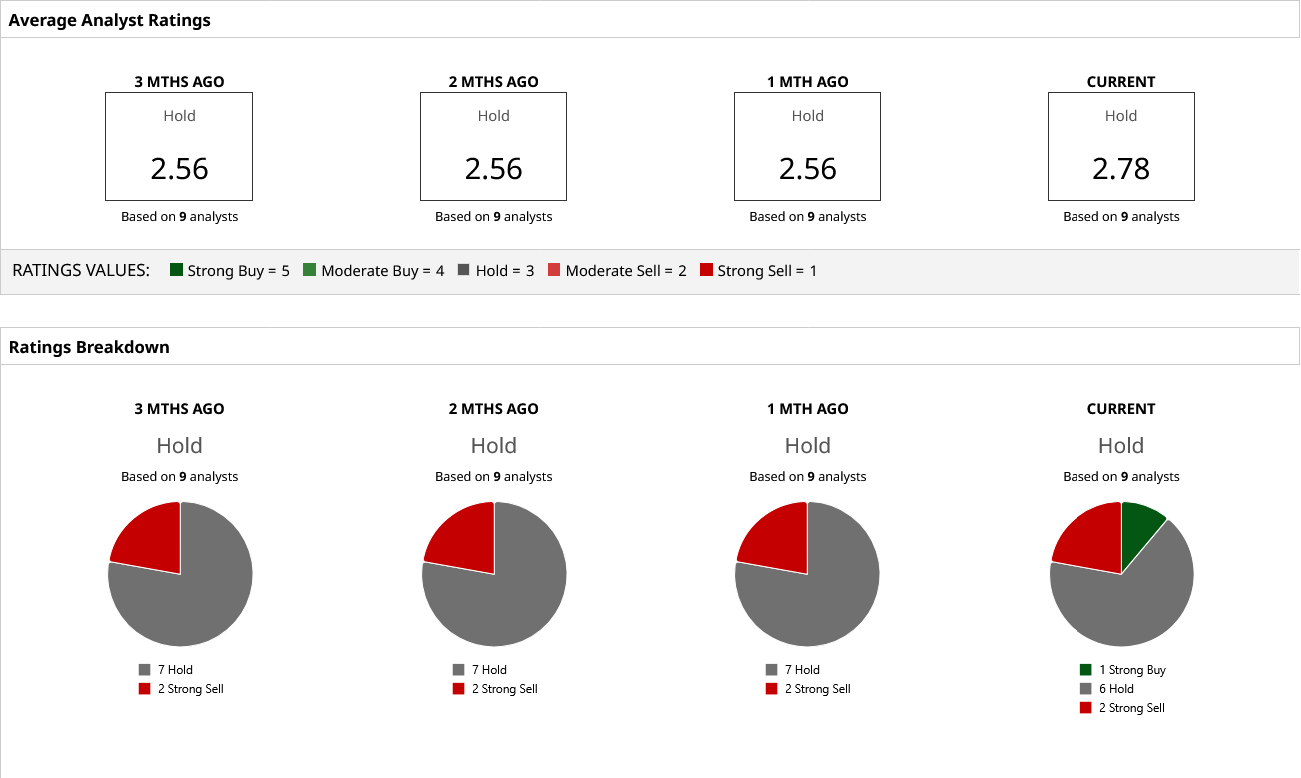

Wall Street is still leaning cautiously. Barchart shows FCEL stock with a consensus “Hold” rating based on nine analysts and an average target of $13.24. That target implies roughly 22% downside from the current price.

Separately, Wells Fargo recently cut its target to $6 from $7, and TD Cowen kept a “Hold” while lifting its target to $9 from $7. The one standout optimist was Canaccord, which upgraded FCEL to $30 from $12. Canaccord analyst George Gianarikas noted that despite uncertainty about the timing of an upcoming “transformative data center deal,” they are certain one is “within reach.”

However, for now, analysts like Jefferies, Goldman, Morgan Stanley, etc., have mostly steered clear or are neutral.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

FuelCell Stock Sink After Q2 Earnings Miss. Why 267% Pipeline Growth Wasn’t Enought. Jensen Huang Says AI Is ‘Insanely Profitable.’ That Means It’s Not Too Late to Hop on the Nvidia Bandwagon. Blue Owl Capital President Logan Nicholson Just Bought 3,000 Shares of OBDC Stock Amid Private Credit Scandal Nvidia Chose This AI Cloud Stock Over Everyone Else. Here’s Why.