For a few years now, artificial intelligence (AI) has been the market’s undisputed growth engine, powering massive gains for tech giants and fueling relentless investor optimism. However, a growing number of strategists are beginning to question whether the AI boom can maintain its current pace, with rising AI token costs emerging as a potential headwind for the sector. Among the skeptics is Wells Fargo (WFC) Chief Equity Strategist Ohsung Kwon, who recently warned that the market’s AI-fueled surge may be entering a more challenging phase.

“The sugar high rally is likely over,” Kwon said, describing the recent market pullback as a reminder that “nothing goes up every day, forever.” While he stressed that the current tech selloff was initially driven more by market positioning than weakening fundamentals, he pointed to what he sees as the most immediate risk to AI stocks is the end of “token-maxxing.” The concern centers on rising AI token costs as AI labs scale back subsidies that had previously helped keep usage expenses in check.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

As those costs climb, companies ranging from Walmart (WMT) to Uber (UBER) have begun signaling that their AI budgets could be consumed much faster than expected. According to Kwon, any slowdown in AI spending could have significant implications for the broader investment theme that has fueled many of the market’s biggest winners. The challenge arrives at a particularly difficult moment for hyperscalers.

Companies such as Microsoft Corporation (MSFT), Meta Platforms (META), Alphabet (GOOG) (GOOGL), and Amazon (AMZN) are already ramping up capital expenditures amid supply-chain constraints and mounting cost inflation. As infrastructure spending climbs, these companies may be forced to pass higher costs on to customers just as businesses grow increasingly sensitive to AI-related expenses.

Reflecting those concerns, Wells Fargo has moved from a bullish stance in April to a “firmly neutral” outlook this month, with Kwon saying the firm is “unenthused about this market.” So, with concerns about rising costs, slowing demand growth, and mounting spending commitments beginning to surface, here’s a closer look at two hyperscalers that could be particularly vulnerable if the AI trade starts to lose momentum.

Stock #1: Microsoft Corporation

Founded in 1975 by Bill Gates and Paul Allen, Microsoft has evolved from a small software startup into one of the most influential technology companies on the planet. Headquartered in Redmond, Washington, the tech giant has shaped the modern digital era through iconic products such as Windows, Office, Teams, and Xbox, platforms that have become deeply embedded in the way people work, communicate, and entertain themselves.

Over the decades, Microsoft expanded well beyond its software roots, making a bold push into cloud computing with Azure, which has become a cornerstone of digital transformation for businesses worldwide. Today, the company is doubling down on artificial intelligence, weaving AI-powered capabilities throughout its ecosystem in an effort to boost productivity, streamline workflows, and redefine the ways users interact with technology.

Yet despite Microsoft's dominant position and relentless innovation across both cloud and AI, investors have become increasingly cautious. Shares have faced mounting pressure over the past year as the company commits tens of billions of dollars toward expanding its AI infrastructure, raising concerns about the near-term payoff from those massive capital expenditures. The recent broader tech selloff has only added to the stock's struggles, weighing further on investor sentiment.

While Microsoft remains one of the world's most valuable companies, boasting a market capitalization of roughly $2.95 trillion, its stock performance has failed to keep pace with the broader market. Shares have fallen 17.9% over the past year, sharply trailing the 21.27% gain delivered by the broader S&P 500 Index ($SPX). The weakness has persisted in 2026, with MSFT down another 19.8% year-to-date (YTD), compared to the broader market's 6.7% advance.

www.barchart.com

www.barchart.com Microsoft’s fiscal third-quarter 2026 earnings report, released on April 29, showcased a company firing on all cylinders operationally, even as Wall Street focused on a growing concern. The tech giant delivered revenue of $82.9 billion, up an impressive 18% year-over-year (YOY) and comfortably ahead of analysts’ expectations of $81.4 billion. Leading the charge was Azure and other cloud services, which posted remarkable growth of 40% YOY, or 39% in constant currency, underscoring the continued strength of enterprise demand for Microsoft's cloud and AI offerings.

Growth was broad-based across the business. The Intelligent Cloud segment, home to Azure, server products, GitHub, and Nuance cloud services, generated $34.68 billion in revenue, marking a 30% increase from the prior year. Meanwhile, the Productivity and Business Processes division, which includes Office, LinkedIn, and Dynamics, delivered $35.01 billion in revenue, up 17% YOY. On the bottom line, Microsoft's earnings power remained equally impressive, with adjusted EPS climbing 21% annually to $4.27, easily surpassing Wall Street's consensus estimate of $4.07.

However, the headline-grabbing aspect of the quarter wasn't Microsoft's strong financial performance, it was the enormous price tag attached to its AI ambitions. The company spent a staggering $31.9 billion on capital expenditures during the quarter alone, a level of spending that continued to weigh on free cash flow. More notably, management stunned investors by forecasting roughly $190 billion in CapEx for calendar year 2026, while guiding fourth-quarter spending to exceed an eye-popping $40 billion in a single quarter.

That massive investment plan overshadowed an otherwise stellar report and sparked concerns about how long Microsoft can sustain such aggressive spending before seeing stronger returns. Investors responded cautiously, sending the stock down roughly 4% following the earnings release despite the company's clear top- and bottom-line beat. Still, management highlighted that its AI business surpassed a $37 billion annual revenue run rate during the quarter, soaring 123% YOY. Microsoft also continued rewarding shareholders, returning $10.2 billion through dividends and share repurchases during the third quarter of fiscal 2026.

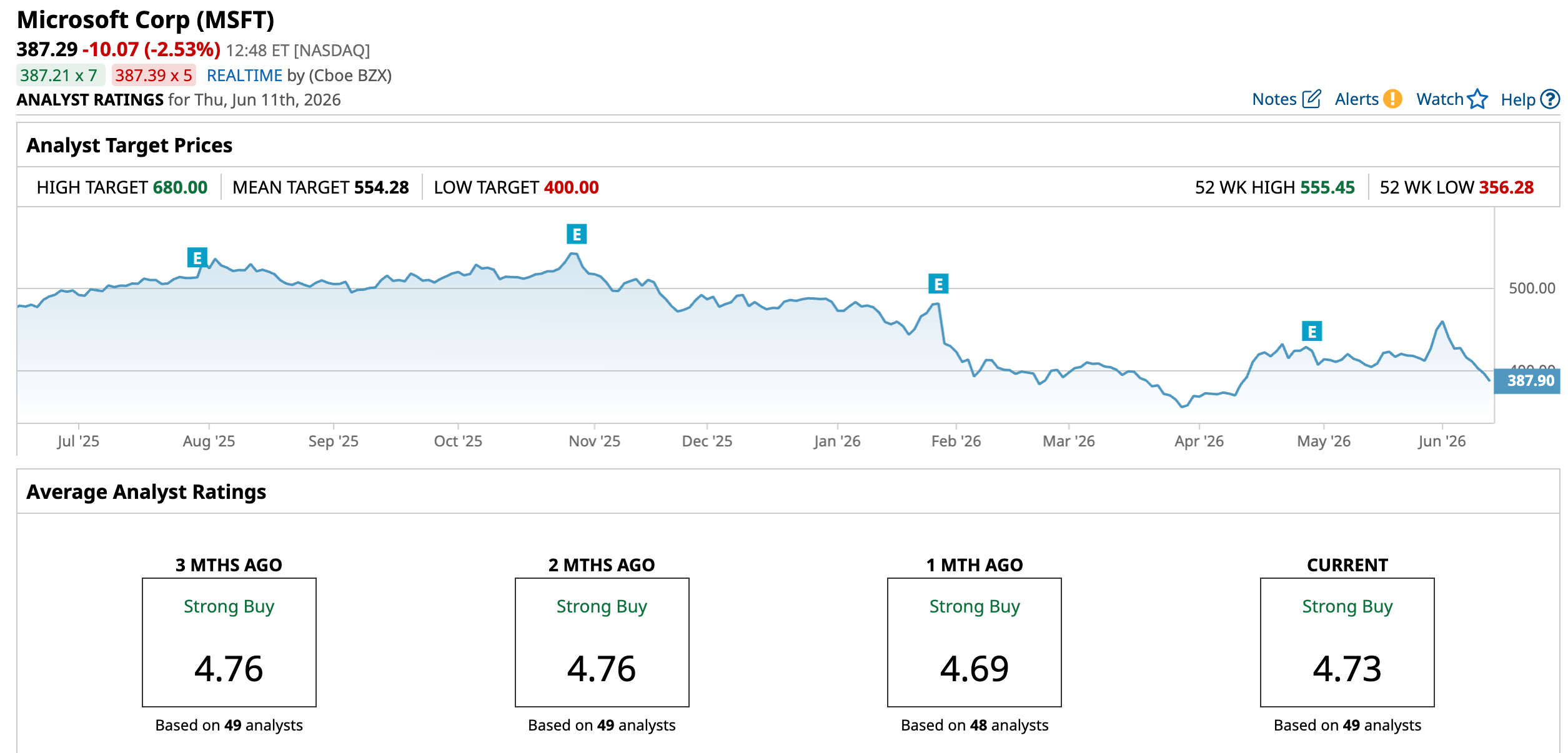

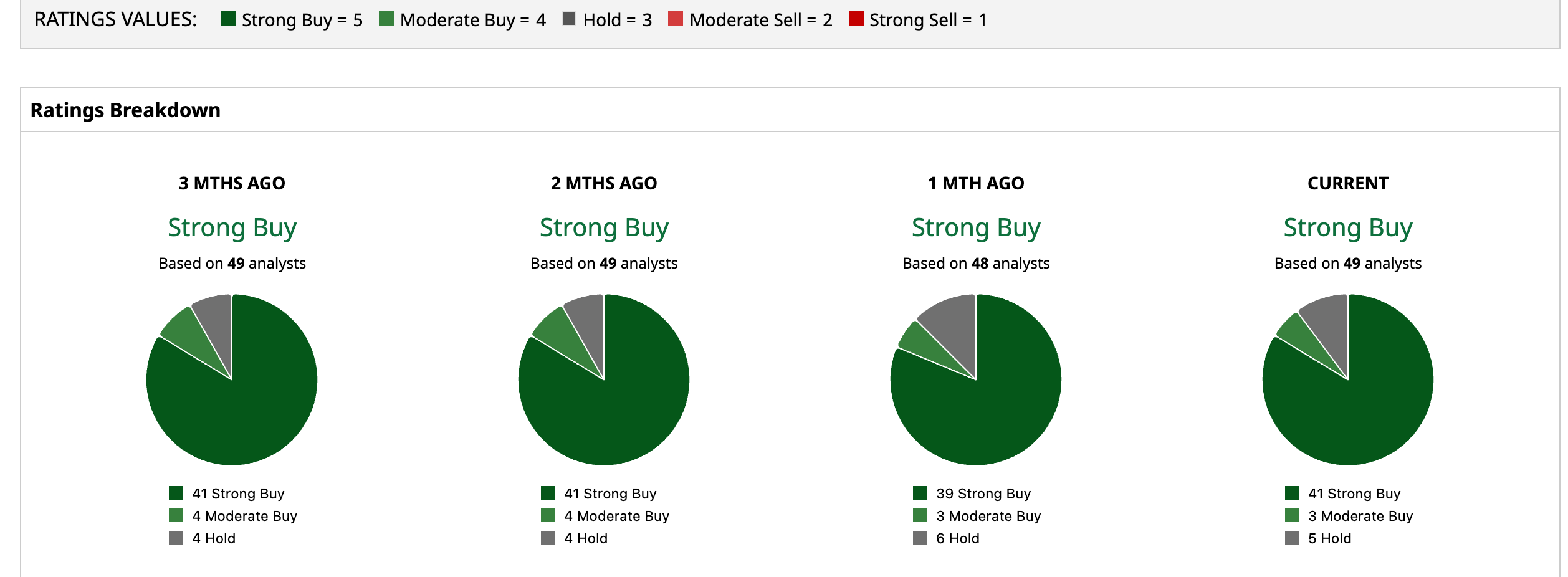

Despite Microsoft's recent struggles on Wall Street, analysts remain overwhelmingly optimistic about the tech giant's long-term prospects. The stock currently carries a consensus “Strong Buy” rating, reflecting continued confidence in its leadership across cloud computing and AI. Among the 49 analysts covering the stock, 41 rate it a “Strong Buy,” three recommend “Moderate Buy,” and only five remain on the sidelines with a “Hold” rating.

The average analyst price target of $554.28 implies potential upside of 43.12% from current levels, while the Street-high target of $680 points to a potential gain of as much as 75.6%, highlighting analysts' confidence that Microsoft's AI and cloud investments could eventually translate into significant shareholder returns.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Stock #2: Meta Platforms

What started as a college social networking website called Facebook has grown into one of the world's most powerful technology companies. Founded in 2004 by Mark Zuckerberg and headquartered in Menlo Park, California, Meta Platforms has fundamentally reshaped the way billions of people connect, communicate, share content, and engage with the digital world through platforms such as Facebook, Instagram, WhatsApp, and Messenger.

Over the years, Meta has evolved far beyond its social media roots, pouring billions of dollars into technologies it believes will define the next era of computing. From virtual and augmented reality initiatives housed within its Reality Labs division to sophisticated AI systems that power content recommendations, advertising, and user engagement, the company has consistently positioned itself at the forefront of innovation.

Today, Meta sits at the crossroads of social media, digital advertising, artificial intelligence, and immersive technologies, making it one of the most closely watched players in the tech sector. However, despite its aggressive push into AI and its dominant position across multiple digital markets, investors have become increasingly cautious.

While advertising remains Meta's core profit engine, the company's massive investments in AI infrastructure and future technologies have raised questions about spending levels and long-term returns. Currently valued at approximately $1.44 trillion, Meta, much like Microsoft, has struggled to keep pace with the broader market. Shares have fallen 18.94% over the past year and are down another 14.76% so far in 2026, highlighting growing investor concerns even as the company continues to invest heavily in its next chapter of growth.

www.barchart.com

www.barchart.com Meta’s fiscal first-quarter 2026 earnings report, released on April 29, delivered exactly what investors have come to expect from the social media giant. Explosive growth, massive profits, and an even bigger commitment to artificial intelligence. The company crushed Wall Street’s expectations on both revenue and earnings, with sales surging 33% YOY to $56.31 billion from $42.3 billion a year earlier. That marked Meta’s fastest quarterly revenue growth since 2021 and comfortably topped analysts’ estimates of $55.49 billion.

The impressive performance highlights how CEO Mark Zuckerberg’s AI investments are already strengthening the company’s advertising machine, even before generating meaningful standalone AI revenue. The growth story extended well beyond the top line. Family Daily Active People (DAP) reached 3.56 billion on average during March 2026, up 4% from a year ago. Meanwhile, ad impressions delivered across Meta’s Family of Apps jumped 19% YOY, underscoring the growing effectiveness of the company’s AI-powered recommendation and advertising systems.

Profitability was even more impressive. Earnings per share soared 62% from the prior year to $10.44, while adjusted EPS of $7.31 easily surpassed Wall Street’s consensus forecast of $6.71. Yet despite the blockbuster quarter, investors found a reason to worry. Rather than celebrating Meta’s accelerating growth, the market focused on the enormous costs associated with the company’s AI ambitions. Shares slid 8.55% on April 30 as investors digested another sharp increase in spending plans.

Capital expenditures, including principal payments on finance leases, totaled a staggering $19.84 billion during the quarter, reflecting Meta’s aggressive buildout of AI infrastructure and data center capacity. The company also returned $1.35 billion to shareholders through dividends and dividend-equivalent payments while maintaining a fortress-like balance sheet with $81.18 billion in cash, cash equivalents, and marketable securities as of March 31, 2026.

However, the biggest concern was management’s updated outlook. Meta reaffirmed its full-year 2026 expense guidance of $162 billion to $169 billion but raised its capital expenditure forecast to between $125 billion and $145 billion, up from its previous range of $115 billion to $135 billion. Management cited higher component costs and additional data center investments needed to support future AI capacity as the primary drivers of the increase.

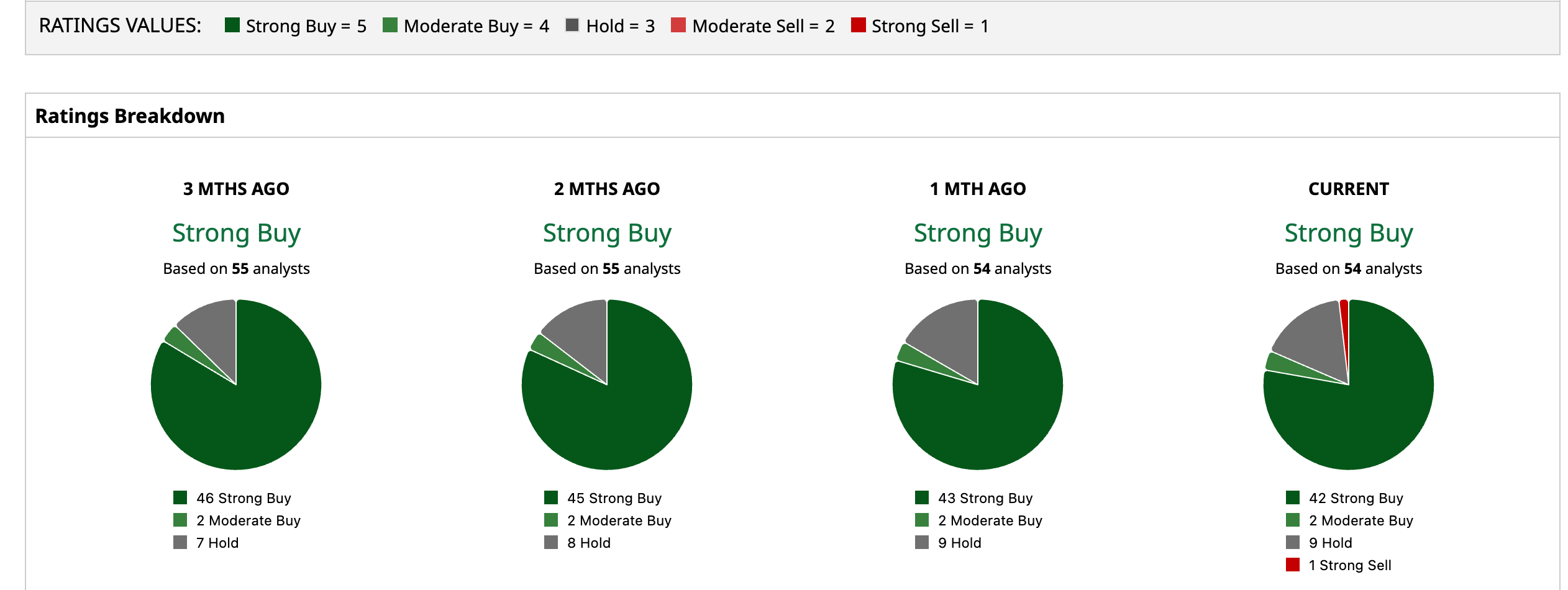

Even with Meta's recent struggles on the stock chart, Wall Street's conviction in the social media and AI giant remains remarkably strong. The stock currently carries a consensus “Strong Buy” rating. Among the 54 analysts covering the stock, 42 recommend “Strong Buy,” two rate it a “Moderate Buy,” nine maintain a “Hold,” and only one analyst has issued a “Strong Sell” rating.

That overwhelming optimism is reflected in analysts' price targets. The average target of $826.78 implies potential upside of 47.6% from current levels, while the Street-high target of $1,015 suggests Meta could surge as much as 81.2%, highlighting Wall Street's belief that the recent weakness may be temporary rather than a sign of deteriorating fundamentals.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Wells Fargo Is Warning That Surging AI Token Costs Is a Death Knell for Hyperscaler Stocks Like Meta and Microsoft Home Depot or Lowe’s: 1 Has Raised Its Dividend for 50+ Years. The Other Pays More Now Iran Ceasefire and a $1,250 Price Target: How to Play Micron Stock Here CubeSmart Stock Is Primed for a Breakout – and It Pays You to Wait with a 5.1% Dividend Yield