Dell Technologies (DELL) is sitting pretty as the artificial intelligence (AI) race keeps pushing demand into overdrive. The Goldman Sachs Group (GS) now sees the AI server market reaching a staggering $1.24 trillion by 2030, a sharp jump from its earlier $961 billion forecast.

The firm lifted its AI server unit volume outlook by 3% and boosted average selling price (ASP) expectations by 15%, signaling that demand for AI infrastructure still has plenty of runway ahead.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Goldman Sachs also sweetened its outlook for traditional servers. The firm increased its forecasts for 2026 through 2030 by roughly 31% on average and now expects that market to hit $164 billion by 2030 instead of the previously projected $105 billion. A 19% rise in expected unit shipments paired with a 10% increase in ASP helped fuel that brighter outlook.

Dell has wasted no time cashing in on those industry tailwinds. During Q1 FY2027, traditional server revenue shot up 92% year-over-year (YOY), unit shipments climbed 24%, and ASP advanced 49%.

Neocloud revenue more than doubled with a 102% YOY increase. Unit shipments rose 34%. Average selling prices jumped 50%. Enterprise revenue followed the same script and surged 91% YOY. Unit shipments increased 29%, while average selling prices climbed 48%.

The company generated approximately $8.5 billion in traditional server hardware revenue during the quarter. Enterprise customers contributed 54% of that figure. Neocloud customers accounted for another 40%. Dell strengthened its grip on the market as traditional server market share climbed to 30% from 20% a year earlier.

However, the crown jewel came from AI servers. Revenue skyrocketed by $14.3 billion YOY, translating into a remarkable 757% growth rate. Unit shipments surged 300%. ASP climbed 81%. AI server market share vaulted to 17% from only 5%, giving Dell a much larger slice of one of technology’s fastest-growing pies.

About Dell Stock

Headquartered in Round Rock, Texas, Dell Technologies is a global technology company that develops and sells computers, servers, data storage systems, networking products, software, and information technology (IT) services.

Carrying a market cap of $252.8 billion, the company helps businesses modernize technology infrastructure, manage data, strengthen digital operations, support AI workloads, and access financing, subscription, leasing, and technology consumption solutions.

The stock has delivered significant performance momentum, increasing approximately 248.8% over the past 52 weeks and advancing 214.2% year-to-date (YTD). The shorter-term trajectory reflects continued acceleration, with gains of 163.9% over the past three months and 63.6% over the past month.

www.barchart.com

www.barchart.com On the valuation front, DELL stock is currently trading at 21.01 times forward adjusted earnings and 1.49 times sales. The numbers sit below the broader industry average but still run above the company’s five-year historical multiples.

Additionally, Dell returns capital to shareholders with an annual dividend of $2.52 per share, which translates into a yield of 0.68%. The company paid its most recent quarterly dividend of $0.63 per share on May 1 to shareholders of record as of April 21.

Dell Surpasses Q1 Earnings

Dell’s Q1 FY2027 results arrived on May 28 with all the subtlety of a fireworks finale. The stock gained 3.8% on the day of the announcement and then sprinted another 32.76% higher in the following trading session.

Revenue surged 87.5% YOY to $43.8 billion, comfortably topping analyst expectations of $36.1 billion. Adjusted EPS climbed 213.5% to $4.86 from the prior year period and raced past Wall Street’s estimate of $2.96.

The Client Solutions Group, which includes desktop personal computers, laptops, monitors, and related equipment sold to consumers and businesses, generated $14.6 billion in revenue. The figure represented growth of 16.8% from the previous year.

However, the Infrastructure Solutions Group stole the show. Revenue from Dell’s data center-focused operations surged 181.2% to $29 billion. AI-optimized server sales exploded, up 757.2% to $16.1 billion, providing the horsepower behind the division’s standout performance.

That strength flowed straight to the bottom line. Adjusted operating income jumped 154.2% YOY to $4.2 billion while adjusted net income surged 193.7% to $3.2 billion. Moreover, adjusted free cash flow advanced 41.8% and reached $3.2 billion.

Looking ahead, management expects Q2 FY2027 revenue to land between $44 billion and $45 billion. The midpoint of $44.5 billion implies YOY growth of 49%. Management expects adjusted diluted EPS of $4.80 at the midpoint, representing growth of 107%.

Also, the company raised its full-year FY2027 outlook. Revenue now stands projected between $165 billion and $169 billion. The midpoint of $167 billion points to growth of 47% from the previous year. Full-year non-GAAP diluted EPS is expected to reach $17.90 at the midpoint, reflecting 74% growth.

Analysts currently forecast Q2 FY2027 EPS of $4.57, representing YOY growth of 117.6%. Full-year FY2027 bottom line is expected to rise 90.3% from the prior year to $17.60 while FY2028 projections call for another 20.17% increase to $21.15.

What Do Analysts Expect for Dell Stock?

JPMorgan analyst Samik Chatterjee has lifted DELL’s price target to $500 from $280 and maintained an “Overweight” rating after the latest earnings report. The move capped a rapid progression.

Chatterjee had already increased the target to $280 from $205 on May 15 after memory cost pressures eased. The latest earnings report convinced him to push the target all the way to $500.

Goldman Sachs joined the chorus and raised its price target to $500 from $230 while reiterating a “Buy” rating. The firm cited growing confidence in Dell’s scale, business mix, and long-term growth opportunities tied to rising demand for agentic AI solutions.

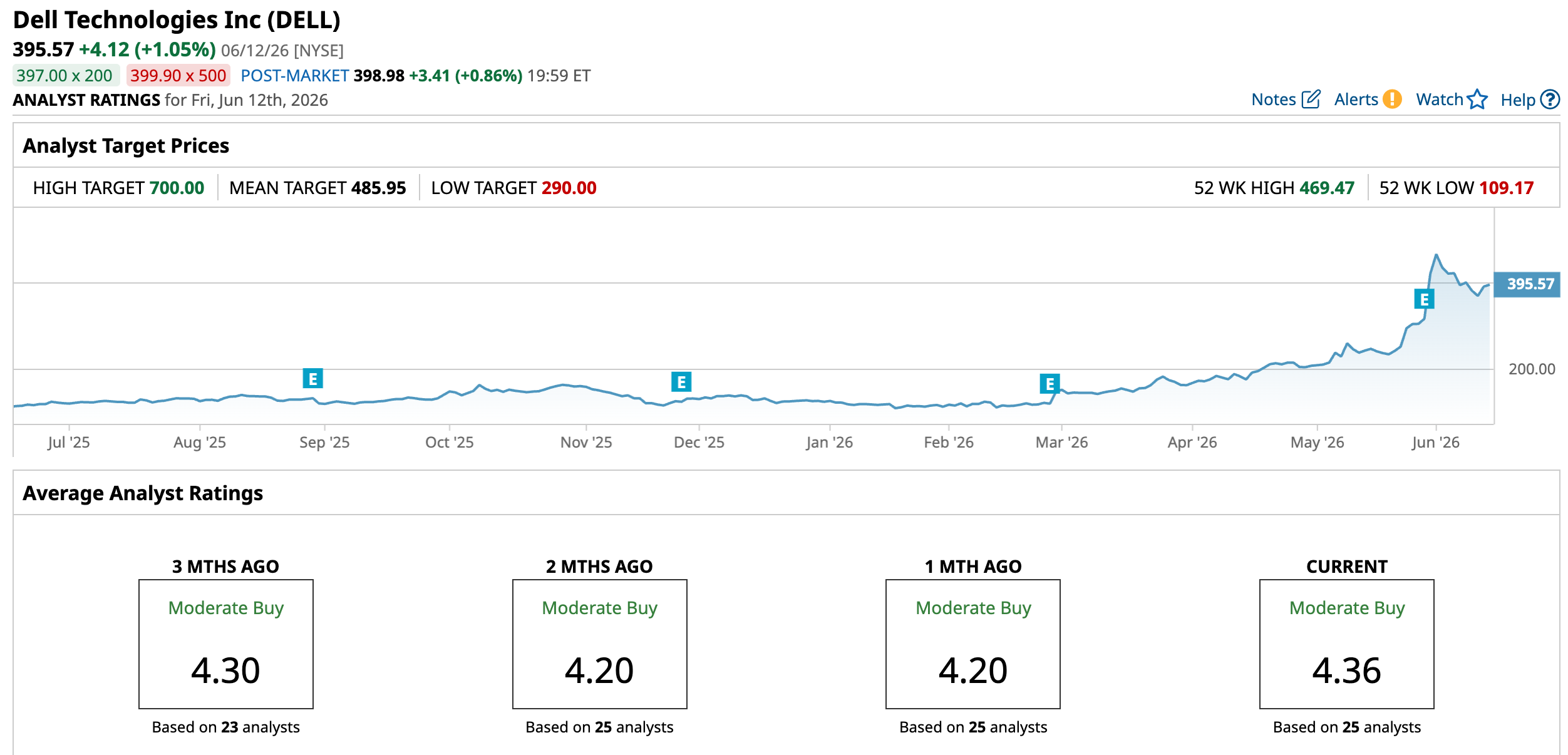

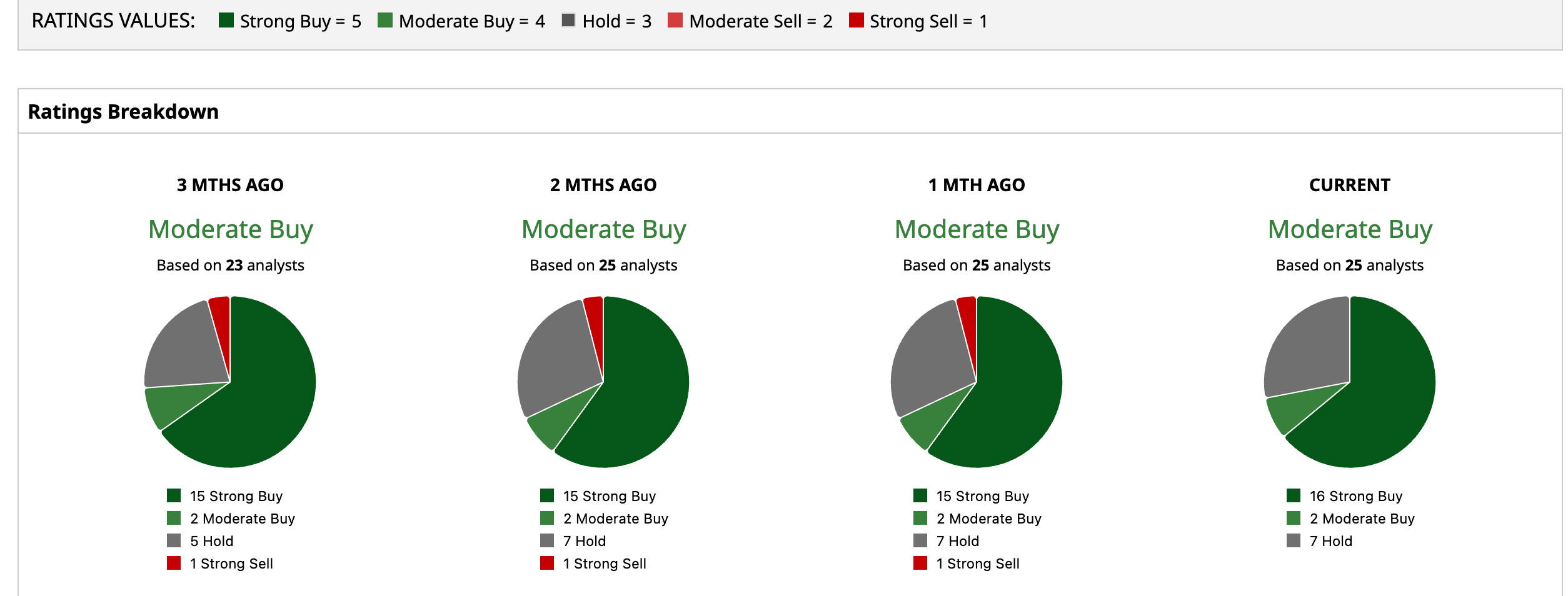

Wall Street currently assigns Dell an overall “Moderate Buy” rating. Among 25 analysts covering the stock, 16 recommend “Strong Buy,” two recommend “Moderate Buy,” while seven suggest “Hold.”

To that end, the stock’s average price target of $485.95 represents potential upside of 22.85%. Meanwhile, the Street-High target of $700 suggests a gain of 76.96% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A Major Short Squeeze Could Be Brewing in Cracker Barrel Stock Ignore the Financial Influencers Pushing a ‘Trifecta’ ETF Strategy. Manage Risk and Volatility with 1 of These Savvy Funds Instead. A $1.24 Trillion Reason to Buy Dell Stock Now Micron Stock is Now Close to Fair Value, But Shorting 2-Week Puts Yield 7.0%