Last month, Palantir Technologies (PLTR) posted Q1 numbers that made Wall Street sit up and take notice.

The artificial intelligence and data platform company reported 85% year-over-year (YoY) revenue growth in the first quarter of 2026, its best growth rate since going public.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Its U.S. business surpassed 100% YoY growth for the first time, climbing 104%.

These stellar numbers have prompted several Wall Street analysts to raise their PLTR stock price targets.

www.barchart.com

www.barchart.com Palantir's AI Platform Is Setting It Apart From the Competition

Palantir’s Artificial Intelligence Platform, known as AIP, is designed to help large organizations, from defense agencies to Fortune 500 companies, deploy AI in the real world.

At the center of AIP sits something called the Ontology. Think of it as an operating system for a company's data. It connects departments, maps how workflows depend on one another, and ensures AI agents act only on verified information.

As Chief Technology Officer Shyam Sankar put it on the company's Q1 earnings call, AIP is "the no slop zone," meaning AI actions are "governed, attributed and auditable."

The results back this up.

GE Aerospace (GE) saw a 26% increase in engine production after deploying AIP. Defense giant ShipOS cut the manufacturing bill-of-materials approval time from 200 hours to 15 seconds. And the U.S. Department of Agriculture awarded Palantir a contract worth up to $300 million to support American farmers and agricultural supply chains.New partnerships are expanding quickly, too. According to separate company statements, Palantir recently formed a first-class integration with Alphabet's (GOOG) (GOOGL) Google Cloud, connecting its Foundry and AIP directly with BigQuery and Gemini.

Law firm Kirkland and Ellis is building a private equity fundraising platform on AIP.

And McCarthy Building Companies signed a multiyear deal to create what it calls an "AI operations suite" for its construction teams.

What Wolfe Research Said About PLTR Stock

Wolfe Research recently resumed coverage of Palantir with a “Peer Perform” rating. Analyst Alex Zukin praised AIP as the strongest product-market fit in enterprise software today.

He highlighted the Ontology's ability to connect the dots across complex business workflows. The analyst also pointed to metrics such as 150% net revenue retention, 85% revenue growth, and a 97% expansion in remaining deal value, all achieved with just around 1,000 customers and 4,000 employees.

Zukin projects revenue growing at a compound annual rate of roughly 39% through 2029 in his base case, rising to 55% in an upside scenario, against a total addressable market he estimates at $385 billion.

He stopped short of a bullish rating, noting that the tech stock currently trades at about 30x 2027 revenues and 65x earnings, roughly double that of peers. That, he said, makes it a tough entry point as the company heads into larger and more complex renewal cycles.

But Wolfe left the door open, writing that strong growth could make the stock an entry point "too good to ignore," according to Investing.com.

Forward estimates shared on TIKR.com reflect similar optimism.

Analysts expect Palantir's revenue to reach $7.72 billion in 2026 and grow to $38.28 billion by 2030. Normalized earnings per share are projected to climb from $1.47 in 2026 to $8.56 by 2030. Free cash flow margins are expected to hold above 54% through the end of the decade.The Valuation Question Investors Cannot Ignore

Palantir's business is performing at a level few software companies ever reach. Free cash flow in Q1 rose to $925 million, larger than the company's entire quarterly revenue just a year earlier.

Chief Executive Officer Alex Karp said it plainly on the earnings call: "Our free cash flow this quarter is larger than our revenue a year ago in the same quarter. Think about that."

The company's Rule of 40 score, a metric that combines revenue growth and profit margin, soared to 145% in Q1. The industry benchmark for strong performance is typically 40%, and Palantir is nearly four times that.

But premium businesses carry premium valuations. And at current levels, Palantir leaves very little room for error.

Notably, if PLTR stock is priced at 50x forward earnings, it could more than triple within the next four years.

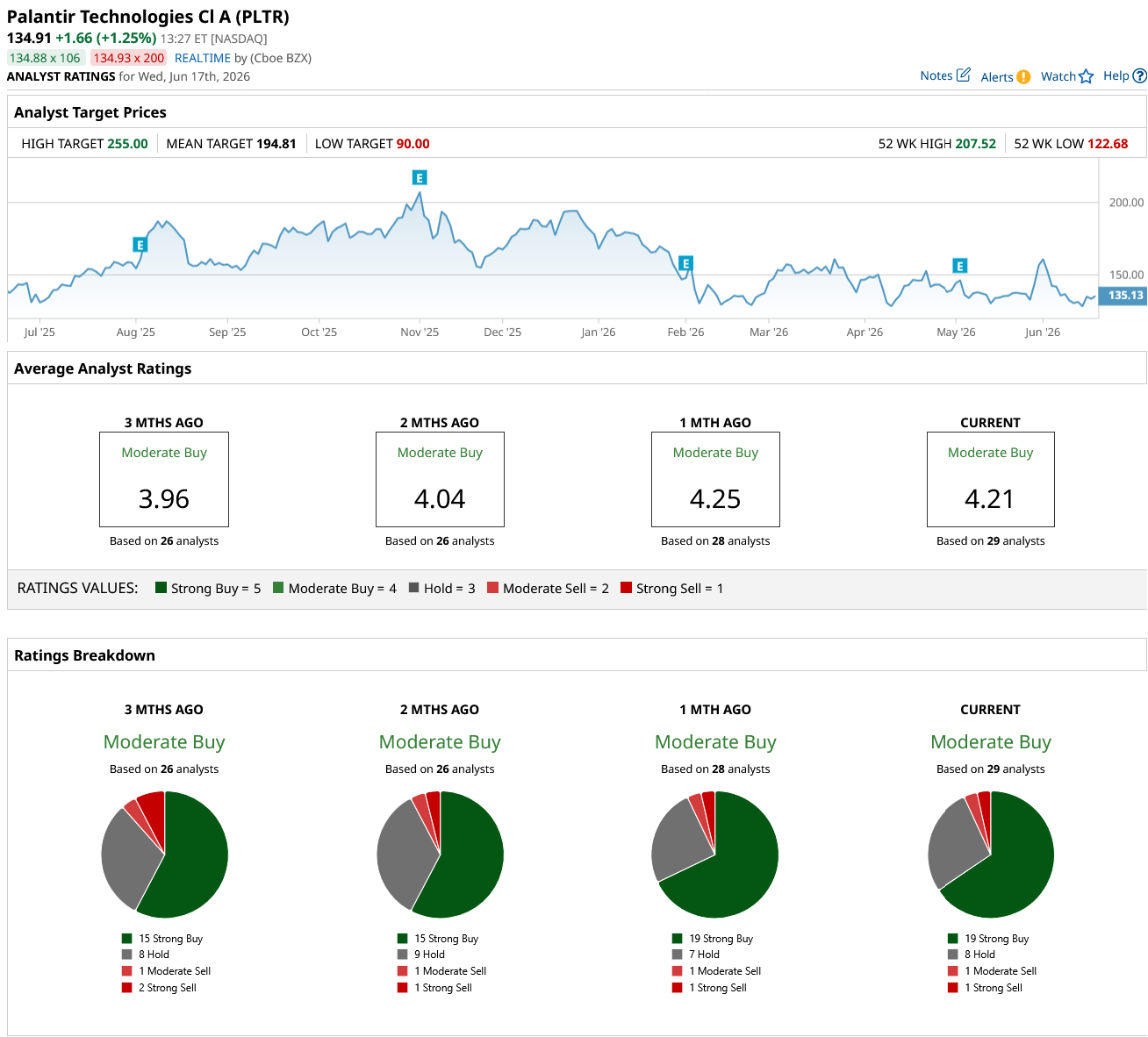

Out of the 29 analysts covering PLTR, 19 recommend “Strong Buy,” eight recommend “Hold,” one recommends “Moderate Sell,” and one recommends “Strong Sell.” The average PLTR stock price target is $194.81, that's about 44% above the current price of $135.

For investors watching from the sidelines, the math is not simple. The business case is compelling, and the valuation demands patience, conviction, or both.

What is clear is that Palantir has moved well beyond being a niche government contractor. It is becoming foundational infrastructure for how enterprises and governments run AI. Whether that justifies today's price is the question every investor will have to answer for themselves.

www.barchart.com

www.barchart.com On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Google Wants to Release 32 Million Mosquitoes in Florida and California in a Bizarre, Futuristic Battle of the Bugs Dear CoreWeave Stock Fans, Mark Your Calendars for June 22 Why This Analyst Says Palantir Stock Is ‘Too Big to Ignore’ Core Scientific Shows Huge, Unusual Put Option Activity - Is CORZ Undervalued?