Equinix (EQIX) is not just renting space anymore. It is becoming a key stop on the AI supply chain. That matters. Big tech does not want random data centers. It wants secure, connected, high-performance sites that can handle huge AI workloads.

That is where Equinix keeps winning. Its ties with Nvidia and Cisco only sharpen that story. The company recently said it is partnering with Nvidia (NVDA) and Cisco (CSCO) to help deploy secure AI factories across its global network of data centers.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Despite this boost, the real question remains. The stock has already had a big run, so the real question is not whether the AI story is real. The question is whether investors are paying too much for it now.

The Stock Has Already Done a Lot of Heavy Lifting

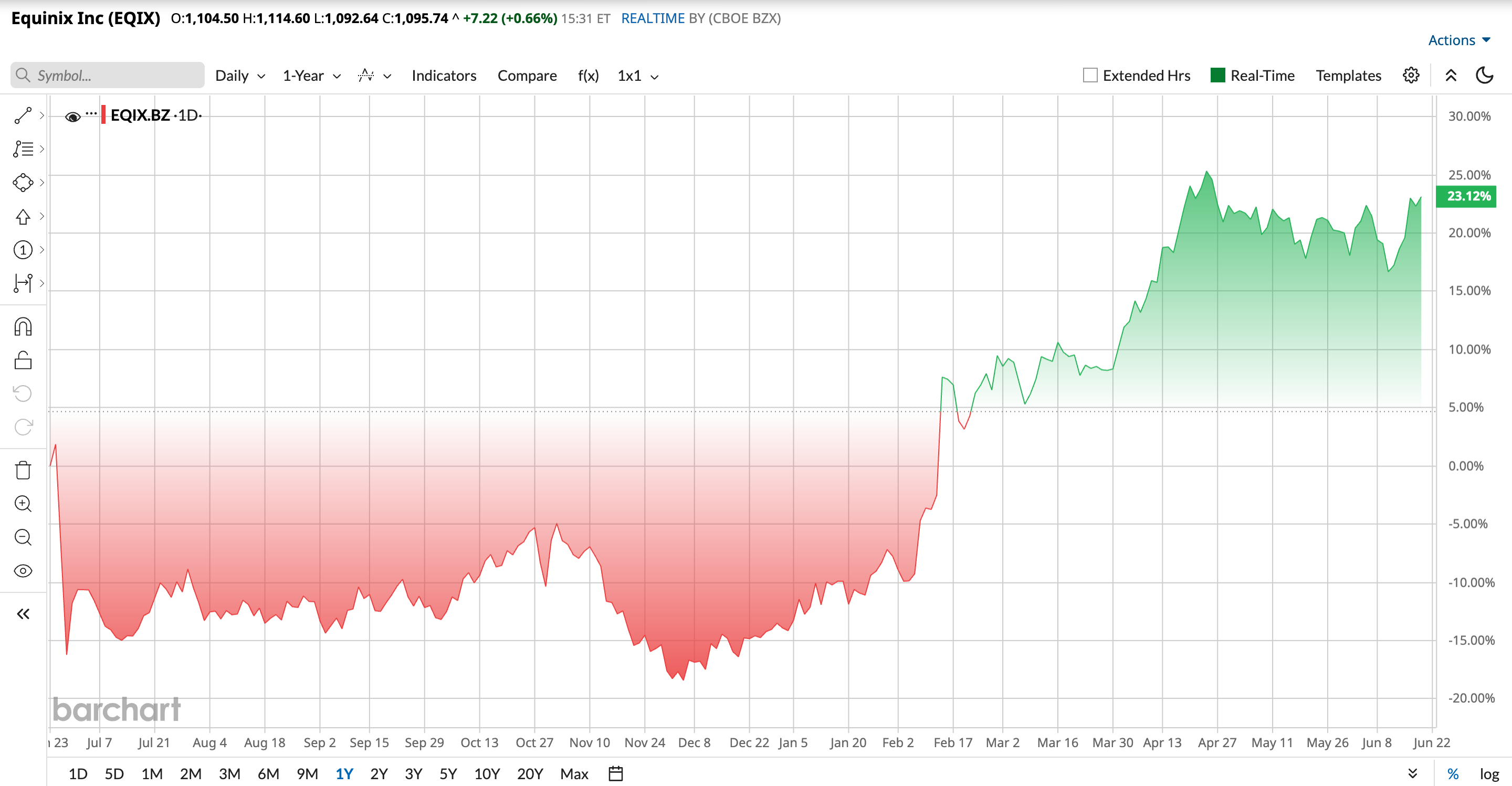

EQIX has been strong over the past year. The stock climbed from the low $700s in mid 2025 to about $1,089 in June 2026, a gain of roughly 43.2% year-to-date (YTD). Investors have chased anything tied to AI infrastructure. The big catalyst has been the idea that Equinix is not just benefiting from AI demand, but it is helping shape where that demand lives.

This is where investors need to be careful. Equinix looks expensive on traditional metrics. Its price-to-earnings ratio is 71.54 times, while the broader REIT sector is much lower, closer to 30.45 times. Its EV to EBITDA multiple is 30.21 times, which is also rich versus most peers in the sector at 16.96 times.

That premium can make sense for a company with durable growth and a strong AI position. But it also means the market is already paying up for a lot of good news. This is not a bargain stock. It is a quality stock priced like one.

www.barchart.com

www.barchart.com Nvidia and Cisco Add Credibility to the AI Story

The latest headline is important because it shows Equinix is getting pulled deeper into the AI buildout. Its expanded work with Nvidia, and Cisco is aimed at secure AI factories across its data center footprint. That means Equinix wants to be the place where enterprise AI gets deployed, tested, and scaled.

Investors liked that. The stock popped on the announcement. That reaction makes sense because deals like this validate Equinix’s role in AI infrastructure. They also strengthen its pitch to large customers who want trusted partners, not just raw capacity. The impact is bigger than a one-day move. Rather, it gives Equinix more credibility in front of customers, and more optionality for future service revenue.

Q1 Showed the Core Business Is Still Moving

Equinix’s latest quarter was strong. For the first quarter of 2026, revenue came in at $2.444 billion, up 10% year-over-year (YOY) on an as-reported basis. Also, the company continues to lean on a mix of recurring services across its global footprint, with growth coming from the Americas, EMEA, and Asia Pacific regions. That is the kind of broad-based demand investors want to see.

Net income was $415 million, up 21% from a year ago. Adjusted EPS came in at $4.20, up 20%. Free cash flow was negative in the quarter because Equinix is still spending heavily on expansion, and cash, cash equivalents, and restricted cash ended the period at about $1.4 billion.

CEO Adaire Fox-Martin said the results reflected continued strength across the business and highlighted customer demand for AI, cloud, and networking solutions. That is the right message for this stock.

The company also raised guidance. For the full year 2026, revenue is now expected to land between $10.144 billion and $10.244 billion. Analysts are looking for about $10.3 billion to $10.4 billion in revenue for the year, with earnings estimates still pointing higher as capacity and demand keep improving.

Wall Street Still Likes the Stock

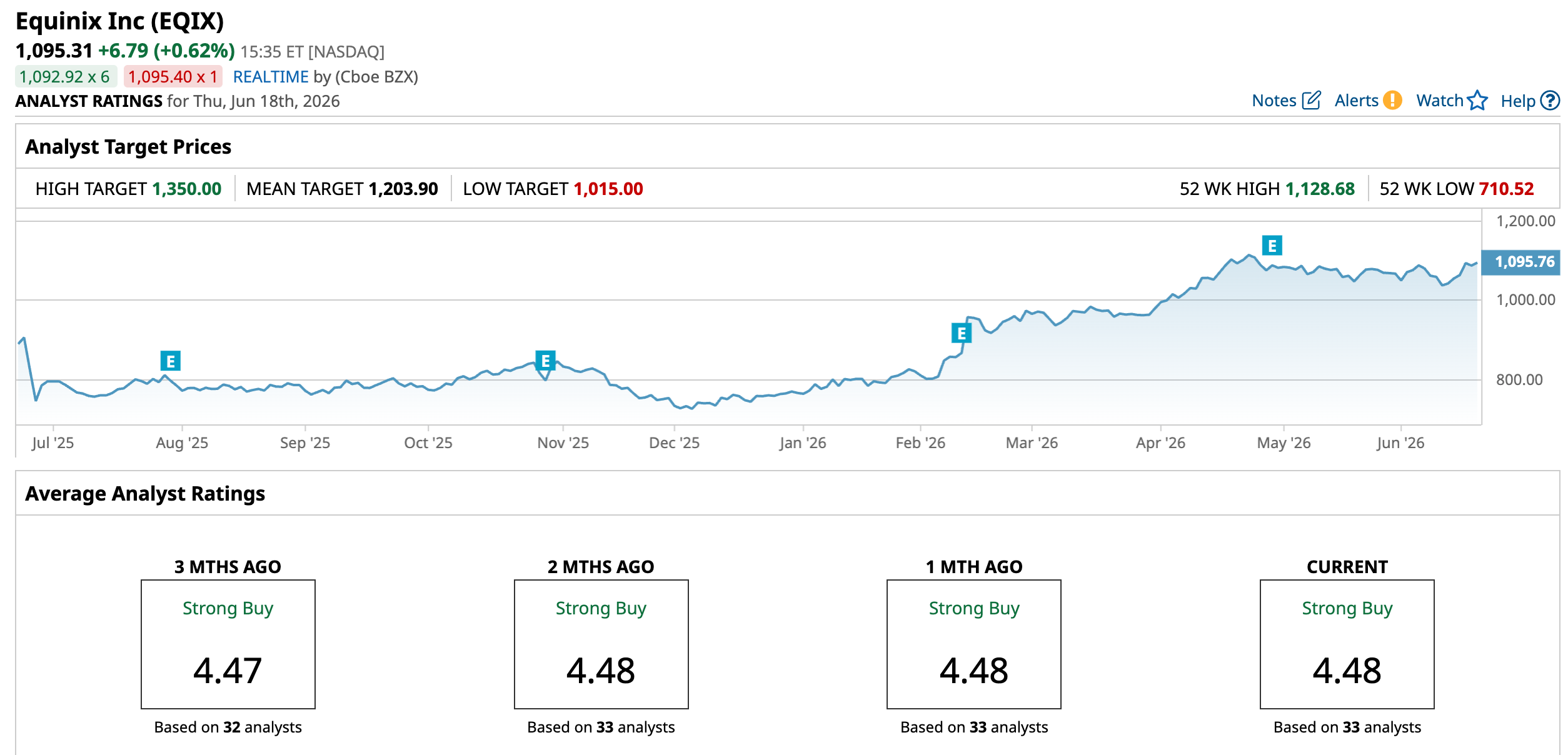

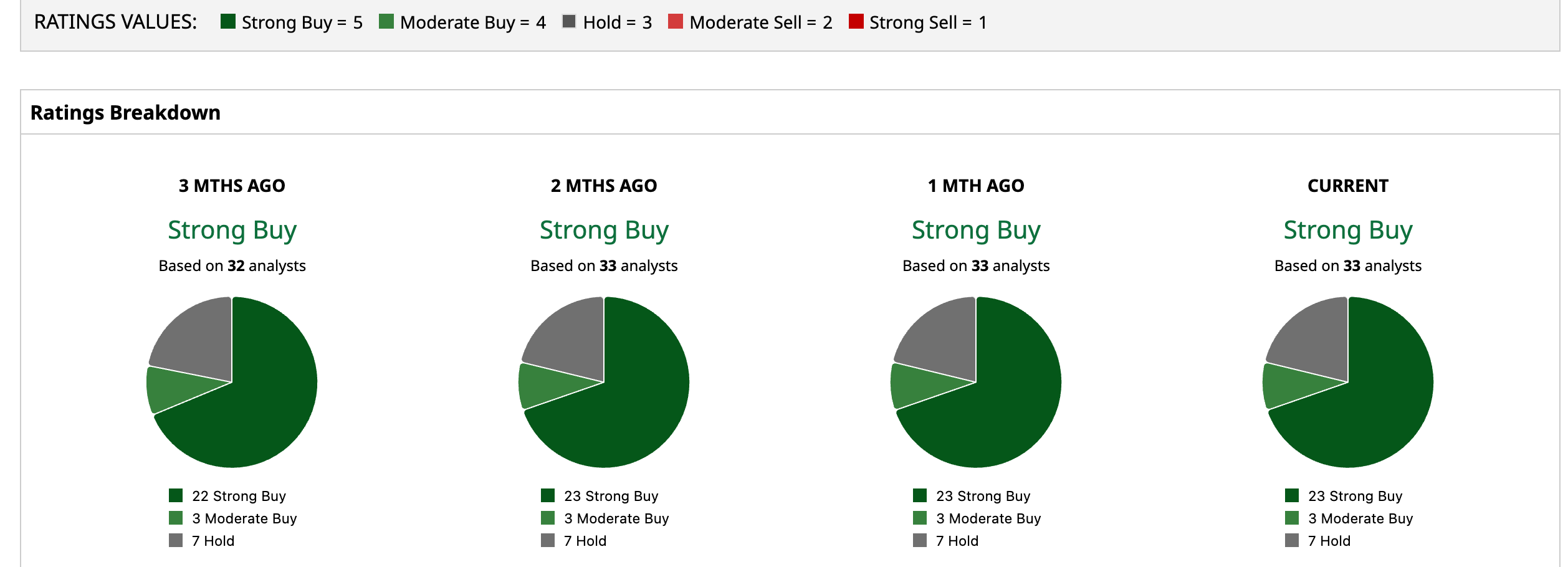

Analysts still lean positive. Morgan Stanley raised its price target to $1,075 and kept an “Overweight” rating, pointing to stronger recurring revenue and better guidance. Goldman Sachs has a “Buy” rating and sees long-term AFFO growth supported by data center demand. Guggenheim kept its “Buy” rating and $1,235 target.

The average analyst target is $1,203.90, which points to 9.8% upside. The consensus rating is still firmly bullish at “Strong Buy” levels.

Equinix has the AI story, the execution, and the analyst support. But after a big run, investors may want to buy it with patience, not chase it with both feet.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

The Quiet Revolution at the Fed: The U.S. Banking Sector Received a Catalyst More Potent than Rate Cuts Carnival Stock Pops on Mediterranean Expansion Plans Trump Just Sent Intel Stock Soaring. Here's Why.