Sandisk (SNDK) has become one of the market’s loudest momentum names in 2026. The stock has gone from niche memory play to one of the hottest charts on Wall Street. That alone makes it interesting. But what really stands out is that the move is not just about hype. It is tied to strong demand for NAND flash, tight supply, and a business that is suddenly very relevant in the AI buildout.

That is why traders are watching this name so closely. The monthly RSI has shot to an extreme level near 99.14, which normally would scream overbought. Yet the chart keeps refusing to roll over. As Barchart market strategist John Rowland said in the recent video, “Sandisk is not going down. If anything, the trend is continuing, the momentum is moving there is no obstacle in the way of momentum.” That sums up the setup pretty well.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

A Pure Play on Flash Memory

Since separating from Western Digital (WDC), Sandisk has become a cleaner way to play the memory cycle. That can be a blessing when demand is strong. It can also be brutal when pricing turns.

Right now, the cycle is working in Sandisk’s favor. AI infrastructure is consuming more storage. Data centers need more flash. Supply is still tight. And that combination has given Sandisk a very powerful tailwind.

Read more from Barchart:

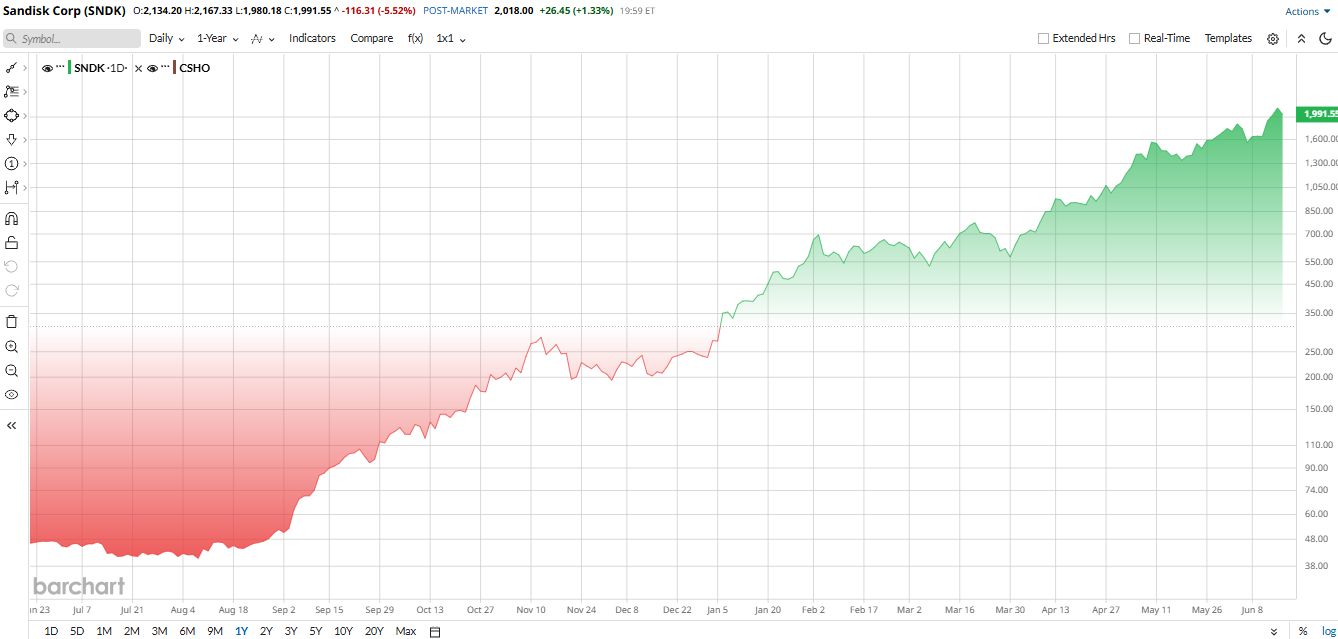

AI is “one of the largest industries ever” ...and it’s already disrupting this $1T market. The next AI wave won’t look like chatbots. It will look like this.The stock has already had a huge run in 2026. It has climbed roughly 725.2% year-to-date (YTD) and 847% over the past six months. It is also trading well above its 50-day moving average, around 1,832, and its 200-day moving average, around 1,608. That tells you the trend is still firmly intact.

Technically, the chart looks almost too strong. But that is also what makes it dangerous to fight. Momentum stocks often look expensive right before they look even more expensive. Rowland’s point matters here. When he said there is “no obstacle standing in the way of momentum,” he was really pointing to the lack of overhead resistance. In simple terms, sellers have not shown up in a meaningful way yet.

www.barchart.com

www.barchart.com Not Cheap, But Not Crazy Either

On valuation, Sandisk is no bargain basement stock anymore. It trades at 30.43 times earnings. That is not cheap. But for a company growing this quickly in a hot memory cycle, it isn't outrageous either. Bank of America (BAC) argued the multiple still looks attractive given Sandisk’s market share gains and the long-term upside from industry consolidation.

The other factor to watch is cash generation. This is not just a story about price action. Sandisk produced about $980 million of free cash flow in its latest quarter. That is real support under the story. When a stock runs this hard, cash flow matters because it helps separate a real business from a pure trading frenzy.

The Latest Quarter Backed Up the Rally

SanDisk’s latest quarter gave bulls plenty to cheer about. The company reported fiscal third-quarter 2026 revenue of $5.95 billion, up 97% sequentially and 251% from a year earlier, as demand stayed strong across the business.

Net income came in at $3.62 billion, while diluted earnings per share landed at $23.03 on a GAAP basis, which also topped the estimate.

The strength was broad-based, not just one hot corner of the business. Data Center revenue reached $1.467 billion, Edge revenue totaled $3.663 billion, and Consumer revenue added another $820 million.

Looking ahead, SanDisk guided for fourth-quarter revenue of $7.75 billion to $8.25 billion and EPS of $30.00 to $33.00, which suggests management still sees plenty of momentum ahead.

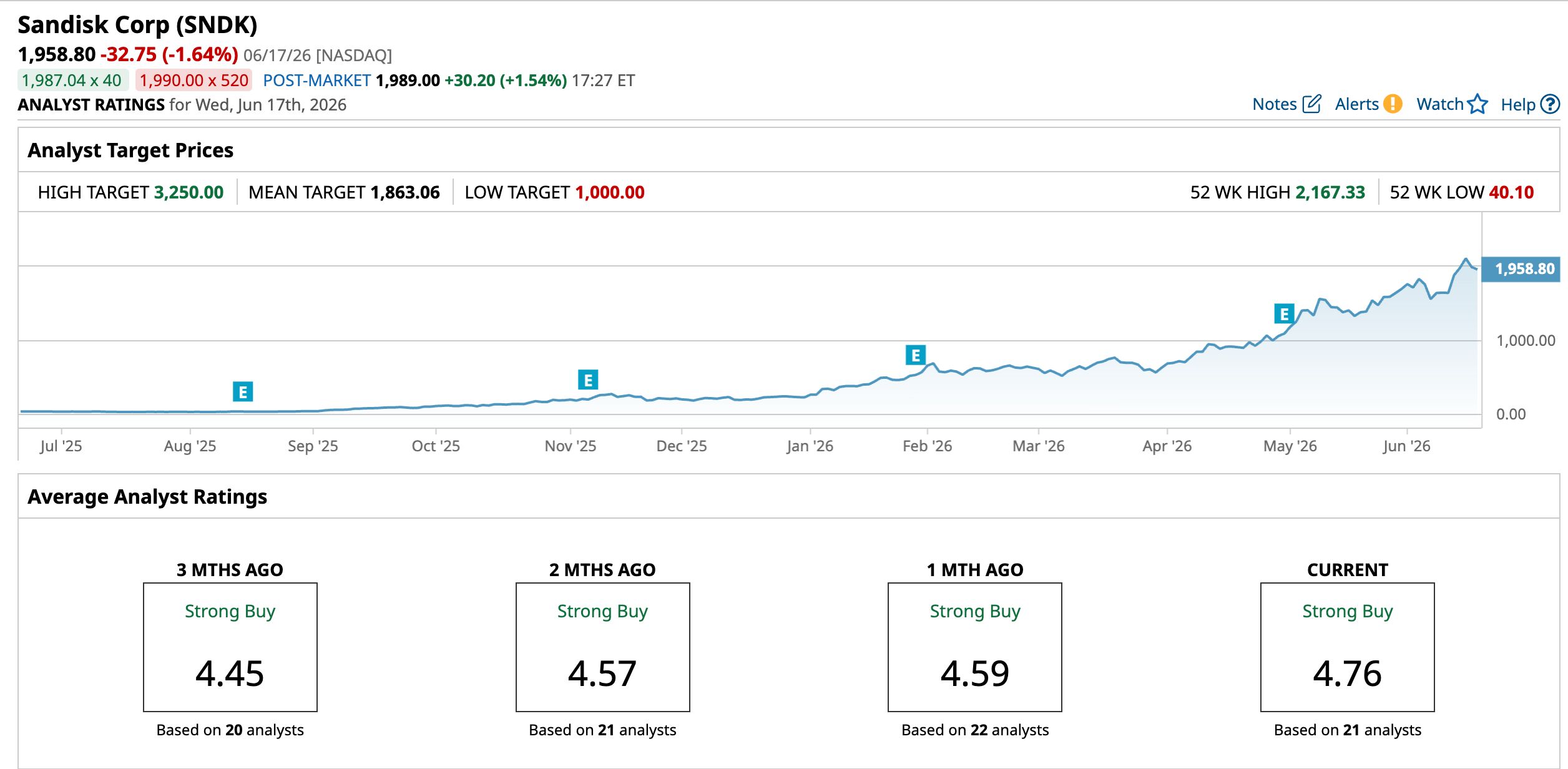

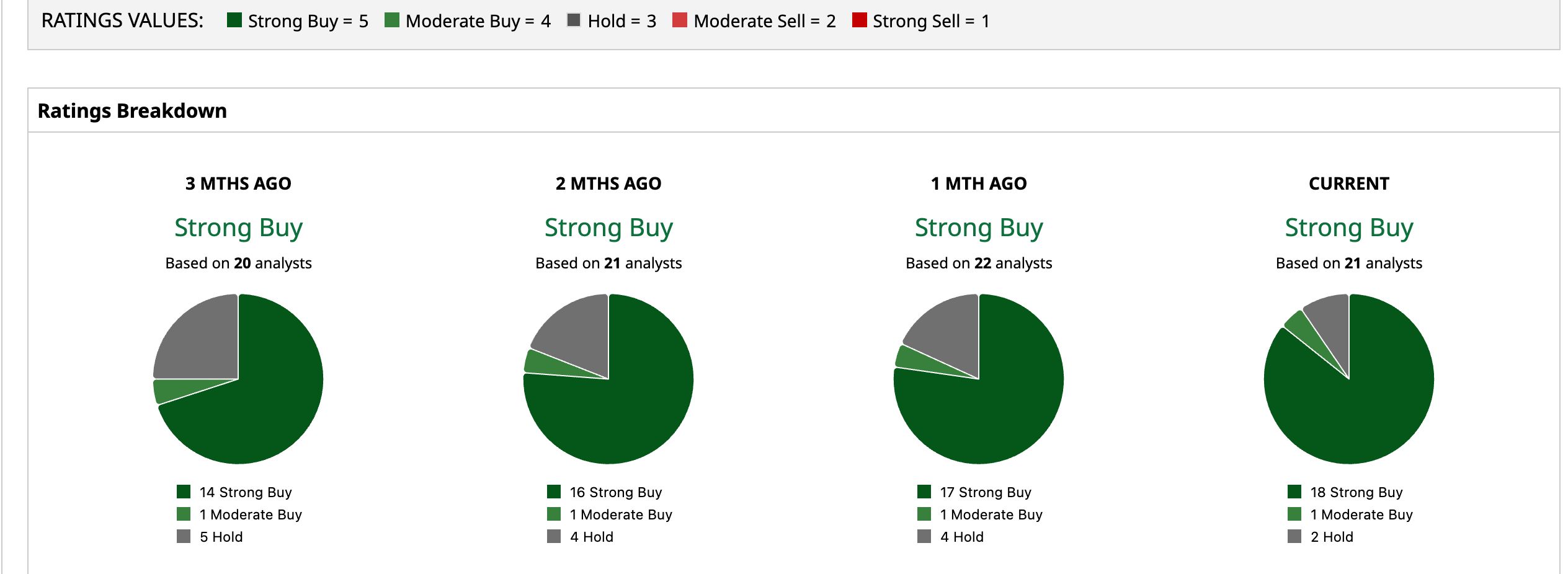

What Analysts Think of SNDK Stock

Wall Street is still bullish. Bank of America raised its price target and kept a “Buy” rating. Goldman Sachs lifted its target to $700. RBC moved its target to $650. Morgan Stanley raised its target to $690 and kept an “Overweight” rating. The common theme is simple. Analysts see a tight NAND market, strong pricing, and better earnings power ahead.

Barchart’s consensus view is "Strong Buy, and the 12-month average target is $1,863.06, with some downside, yet the street's highest target of $3,250 gives hope of the stock climbing another 65.9% from here.

For now, the chart says yes. The fundamentals say yes. The valuation says maybe. That is exactly what makes Sandisk such an interesting stock right now.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

From ‘Hold’ to ‘Buy’: Here Is Why Truist Just Changed Its Mind on DDOG Stock Dear Investors: Don’t Act Your Age, Act Your Risk Tolerance Rivian Is Cutting Staff Again. What That Means for RIVN Stock. SanDisk Stock Looks Wildly Overbought, But SNDK’s Chart and Fundamentals Say It Can Keep Climbing