In business, growth is exciting, but lasting success often comes from making tough decisions behind the scenes. Companies frequently restructure operations, trim costs, and streamline teams to improve efficiency and move closer to profitability. While such moves can be painful in the short and long term, they are often viewed as necessary steps toward building a stronger and more sustainable business.

That brings us to Rivian Automotive (RIVN). The electric vehicle maker has once again turned to workforce reductions, laying off hundreds of employees – less than 2% of its staff – as it works to scale its business profitably. The timing is especially noteworthy. The cuts came just days after Rivian began delivering its highly anticipated R2 SUV, a vehicle many see as the company’s best chance to reach the mass market and finally generate consistent profits.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

With Rivian still searching for its first profitable quarter, investors are closely watching whether these cost-cutting measures, combined with the launch of the promising R2, can help steer the company toward a stronger financial future. RIVN stock is already down 15.7% in 2026, making the success of this cost-cutting push and the R2 rollout critical to determining where the shares go next.

About Rivian Stock

Founded in 2009 and headquartered in Irvine, California, Rivian Automotive is an EV maker focused on building a new generation of sustainable transportation. With a market capitalization of $19.768 billion, the company designs and manufactures electric trucks, SUVs, and commercial delivery vans in the U.S.

Rivian combines advanced vehicle engineering with in-house software, electrical architecture, artificial intelligence, and autonomous driving technologies to create a fully integrated EV ecosystem. Serving both consumer and commercial customers, Rivian aims to accelerate the transition to clean transportation while delivering vehicles built for adventure, utility, and everyday use.

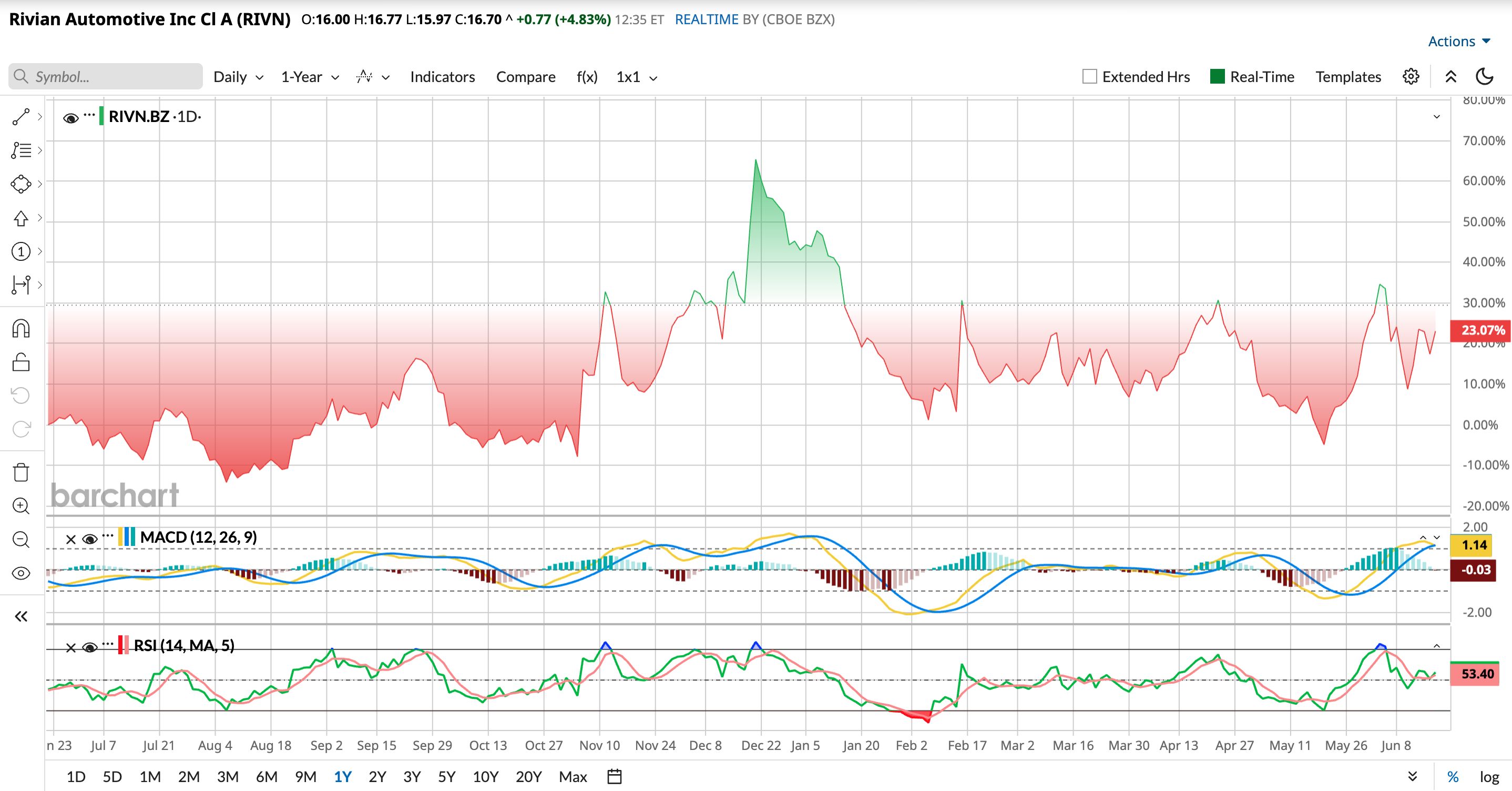

Rivian stock has had to weather plenty of storms over the past year. Shares sank to a low of $11.57 in August 2025 before roaring back to $22.69 by December, showing just how quickly sentiment can shift in the EV space. While the stock has since given back some of those gains and now sits 26.4% below its peak, it remains well above last year’s lows. In fact, RIVN has managed to stay up 24.1% over the past 52 weeks.

The bigger picture is a tale of two markets. On one hand, RIVN has struggled in 2026, falling 15.7% YTD and 5.76% over the past six months as investors wrestle with ongoing losses and a challenging EV environment. On the other hand, recent trading suggests the stock may be finding its legs again. Shares are up 5% over the last three months and have gained roughly 20.49% over the past month alone.

Technically, the clouds may be starting to part. The 14-day RSI sits near a neutral 54.64, indicating the stock is neither overheated nor oversold. Meanwhile, the MACD oscillator shows signs of bullishness, with positive histogram bars.

It is not a home run yet, but investors appear willing to give Rivian the benefit of the doubt as the company trims costs, restructures operations, and bets big on the R2 to drive profitability.

www.barchart.com

www.barchart.com Valuation-wise, RIVN stock trades at 2.89 times forward sales, a premium to many of its auto industry peers. For valuation hawks, that could make the stock a tough pill to swallow, as investors are still paying up today for Rivian’s future growth and profitability potential.

A Snapshot of Rivian’s Q1 Numbers

Rivian’s fiscal Q1 earnings, released on April 30, signaled that the company is still navigating losses but making meaningful progress. The company delivered a better-than-expected performance, with revenue climbing 11.4% year-over-year (YOY) to $1.38 billion, while its adjusted loss narrowed to $0.54 per share. The improvement was largely driven by stronger vehicle deliveries and continued momentum in the company’s software and services business.

Digging deeper, Rivian’s automotive revenue came in at $908 million, down 2% YOY. The decline was mainly tied to lower sales of regulatory credits and a greater mix of commercial vans, which typically generate less revenue per vehicle. However, a 20% jump in vehicle deliveries helped soften the impact. During Q1, Rivian delivered 10,365 vehicles, bringing cumulative deliveries to 175,565 vehicles.

Meanwhile, the software and services segment revenue surged 49% YOY to $473 million, fueled by software development work, electrical architecture services, vehicle repairs, maintenance, and remarketing activities. The growth highlights Rivian’s efforts to build revenue streams beyond simply selling vehicles.

Production, however, told a different story. Rivian built 10,236 vehicles during the quarter, down 30% annually as the company shifted resources toward preparing for the launch of the R2. That transition reached a major milestone when salable R2 production began at Rivian’s Normal, Illinois facility.

Gross profit fell to $119 million from $206 million a year earlier, while gross margin narrowed to 9% from 17%. Operating expenses climbed to $1 billion as Rivian continued investing in growth, pushing its loss from operations to $881 million.

Still, Rivian’s balance sheet remains relatively solid. The company ended the quarter with $4.8 billion in cash and short-term investments and total liquidity of $5.4 billion. Investors are closely watching cash burn, though, as Rivian posted negative free cash flow of $1.08 billion during the quarter, with capital expenditures of $372 million.

Looking ahead, management expects to deliver between 62,000 and 67,000 vehicles in 2026. Adjusted EBITDA is anticipated to be between negative $2.10 billion and negative $1.80 billion, while capex is projected to be between $1.95 billion and $2.05 billion. The company believes rising R2 production will unlock meaningful cost efficiencies, making the success of the new SUV the key factor in Rivian’s path toward profitability.

For fiscal 2026, analysts expect losses to widen by 3% annually to $3.10 per share, and then narrow by 22.6% YOY to -$2.00 per share loss in fiscal 2027. The path to profitability is still a challenging one, but if the R2 launch delivers as hoped, it may not be as far away as it once seemed.

Rivian Tightens Costs With Another Workforce Reduction

Rivian is trimming its workforce again as the EV maker continues its march toward profitability. According to reports first published by The Wall Street Journal and later confirmed by the company, the latest round of layoffs affects employees in service and customer-focused teams, making it another step in Rivian’s broader restructuring effort.

The company described the move as a reorganization of select teams aimed at helping it grow more efficiently while keeping costs under control. While Rivian did not disclose an exact number, the cuts account for less than 2% of its workforce. With around 15,200 employees across North America and Europe at the end of 2025, that suggests roughly 300 positions could be impacted.

Notably, the layoffs appear to be concentrated in customer-facing functions rather than manufacturing, meaning Rivian’s production plans for the newly launched R2 SUV remain largely untouched.

This is not the first time Rivian has taken such measures. In fact, it marks at least the fourth workforce reduction since early 2024. The most significant recent cut came in October 2025, when the company eliminated about 600 jobs, or 4.5% of its staff. CEO RJ Scaringe said those reductions were driven by softer EV demand following the end of federal tax incentives and by preparations for the company’s next growth phase centered on the R2.

Why the Timing Raised Eyebrows

What makes these layoffs stand out is their timing. Rivian announced the workforce reductions just days after beginning deliveries of its highly anticipated R2 SUV, a vehicle widely viewed as the company’s biggest growth opportunity yet.

The R2 is designed to bring Rivian to a much larger audience. The Performance Launch Package starts at $57,990, while the Premium trim is priced at $53,990. A Standard version carrying a $48,490 price tag is expected in 2027, with an even lower-priced $45,000 base model planned for later.

For Rivian, the R2 is more than just another vehicle launch. It is the product expected to help transform the company from a cash-burning EV startup into a high-volume automaker capable of generating sustainable profits. That is why the decision to trim service, sales, and customer-related teams so soon after the launch has caught investors’ attention.

Rivian says the move is about operating more efficiently. But it also underscores the balancing act the company faces – reducing costs and narrowing losses while simultaneously supporting the rollout of what could be the most important vehicle in its history.

What Do Analysts Expect for Rivian Stock?

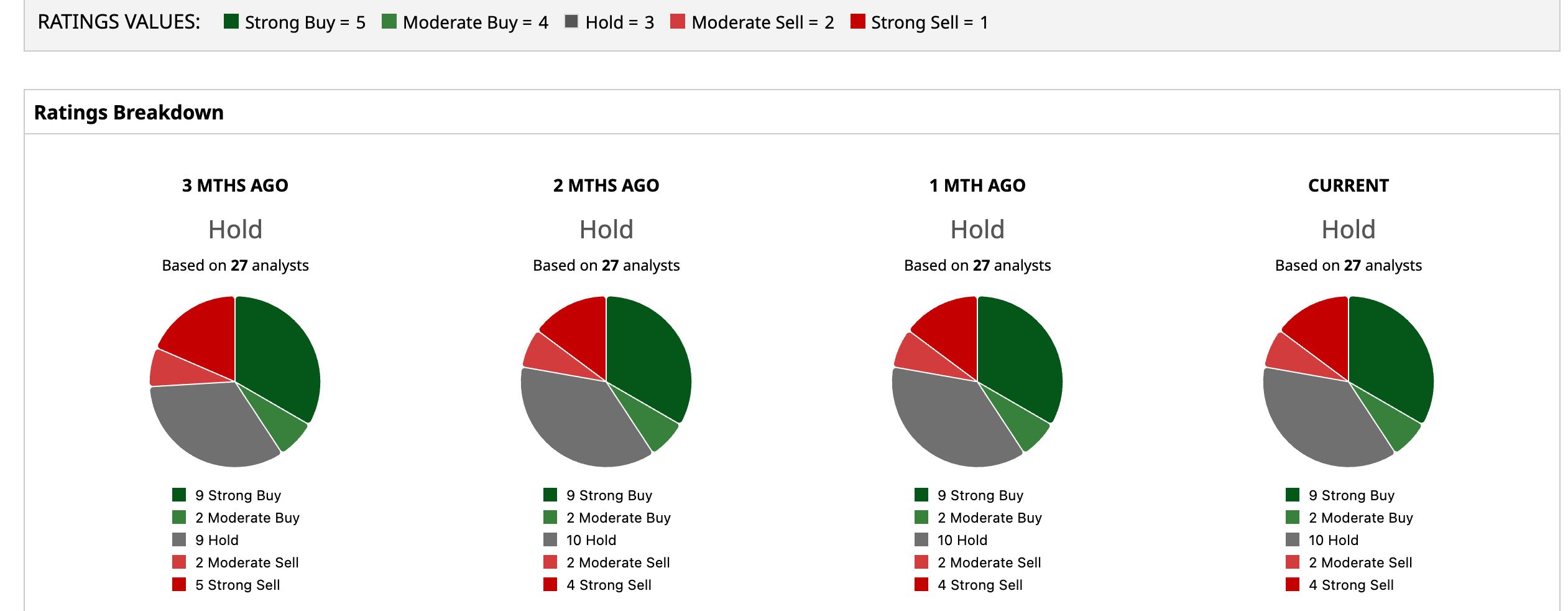

A few clouds may be hanging over Rivian, but Wall Street has not thrown in the towel on RIVN stock. The EV maker carries a consensus “Hold” rating from 27 analysts covering the stock. Among them, nine suggest a “Strong Buy,” two advise a “Moderate Buy,” 10 have a “Hold,” two recommend a “Moderate Sell,” while the remaining four analysts are outright skeptical, recommending a “Strong Sell.”

While Wall Street’s average price target of $17.77 points to an 6.66% upside potential, the most bullish analysts believe RIVN could still have plenty of room to run, with targets as high as $25, representing 50% above current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Conclusion

For shareholders, the story now comes down to execution. RIVN stock has struggled in 2026 as investors waited for clear signs that Rivian could grow sales while moving closer to profitability. The company has now pushed back its profit target beyond 2027 as it spends heavily on both the R2 rollout and autonomous driving technology. While the Uber partnership and potential 50,000-vehicle robotaxi opportunity are exciting, those benefits remain largely tied to technology Rivian has yet to fully prove.

At the same time, the latest layoffs show management is serious about controlling costs. The challenge is making those cuts without hurting customer service, just as thousands of new R2s hit the road. If Rivian can successfully ramp R2 production, keep costs in check, and show progress toward profitability, RIVN stock could regain momentum. If not, investors may continue to question whether the company is trying to accomplish too much at once.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

From ‘Hold’ to ‘Buy’: Here Is Why Truist Just Changed Its Mind on DDOG Stock Dear Investors: Don’t Act Your Age, Act Your Risk Tolerance Rivian Is Cutting Staff Again. What That Means for RIVN Stock. SanDisk Stock Looks Wildly Overbought, But SNDK’s Chart and Fundamentals Say It Can Keep Climbing