Newly listed Cerebras Systems (CBRS) has had a tough run since its listing. Down about 20%, the company is set to report its Q1 and first set of quarterly earnings today after market hours. And the biggest cheerleader of AI stocks in the market, Dan Ives-led Wedbush, remains bullish about the company, irrespective of its sombre start as a public company.

www.barchart.com

www.barchart.com Maintaining its “Outperform” rating on CBRS, the firm has a price target of $270 on the stock. The price target would denote an upside potential of 20.3% from current levels for a company that gained fame for its huge dinner plate-sized chips.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Cerebras

Founded in 2015, Cerebras Systems is an AI infrastructure company that develops accelerators, supercomputing systems, wafer-scale processors, and large-scale inference/training infrastructure. The company is also increasingly offering Inference-as-a-Service (IaaS) and AI cloud services.

The company's market cap has slid to $48.2 billion from the highs of $65 billion in its IPO days.

Yet, Wedbush is still wedded to CBRS stock. Should you? Let's find out.

Cerebras Play

In my most recent analysis of Cerebras, I had tried to make sense of why Cathie Wood bought a substantial number of the company's shares while delving into what it is offering and why it is relevant in the world of inference and agentic AI, a market that is projected to reach $139 billion by 2034.

Well, I had touched upon SRAM or Static Random Access Memory in that piece. While in the age of DRAM, what SRAM offers is noteworthy. Sample this. The Nvidia (NVDA) B200 HBM3e memory bandwidth stands at 8 terabytes per second, whereas the WSE 3 on-chip SRAM bandwidth reaches 21,000 terabytes per second. This creates a massive 2,600 times advantage in favor of the Cerebras system.

Although software improvements and optimizations have helped narrow this substantial bandwidth gap for Nvidia in practice, similar advancements will also benefit the WSE 3 platform. At its core, this represents a fundamental physical edge that cannot be fully overcome by traditional graphics processing unit designs. Supporting evidence of this strength can already be seen in the fact that as of early 2026, their Wafer-Scale Engine architecture (like the WSE-3) holds speed records for running large open-weight models.

For agentic AI, specifically, the value proposition is quite simple: Agents make rapid sequential calls to a model, and every millisecond of latency compounds across a chain of reasoning steps. On Moonshot's trillion-parameter Kimi K2.6 model, independently benchmarked by Artificial Analysis, Cerebras delivered 981 output tokens per second, making it 6.7 times faster than the next fastest GPU cloud provider, with a full agentic coding response completing in 5.6 seconds versus 163.7 seconds on the model's official endpoint.

That speed gap is precisely why hyperscalers have started signing on. OpenAI is integrating up to 750 megawatts of Cerebras compute into its inference stack through 2028, specifically to support latency-sensitive agentic and voice applications, in a deal reportedly worth more than $20 billion. Amazon's (AMZN) AWS has also signed Cerebras to power inference on its Bedrock platform alongside Trainium silicon, giving Cerebras a foothold inside two of the largest cloud ecosystems in the world rather than competing as a standalone vendor.

For the future, Cerebras is responding with deeper hyperscaler partnerships rather than insisting on owning the entire stack alone. Cerebras could position its chips as a decode accelerator that offloads the bandwidth-intensive part of inference while a partner's hardware handles compute-heavy prompt processing, a strategy already underway through the AWS Trainium tie-up.

Financials Fortified With a Sturdy Backlog

Cerebras delivered consistent financial progress in fiscal 2025. Total revenue reached approximately $510 million, reflecting a 76% increase from the prior year. Hardware revenue rose to $358.4 million from $211.9 million in 2024, while cloud revenue advanced to $151.6 million from $78.3 million.

Yet, this has the potential to grow tenfold in just about two years, thanks to Cerebras's massive backlog of $24.6 billion. Moreover, the company expects 15% of it to be recognised by the end of 2027

Coming back to the current times, Cerebras reported net income of $237.8 million for the year, a significant turnaround from a $481.6 million loss in 2024. This improvement was largely driven by other income of $390.7 million, compared with a negative $378.2 million contribution in the previous period.

Cash flow from operations shifted to a net use of cash in 2025. The company used $10.1 million in operating cash flow for the year, in contrast to a positive inflow of approximately $452 million in 2024. Nevertheless, this development does not appear particularly concerning, as Cerebras ended 2025 with a cash balance of $701.7 million, which remains relatively close to its total liabilities of $971.3 million.

Analyst Opinion of CBRS Stock

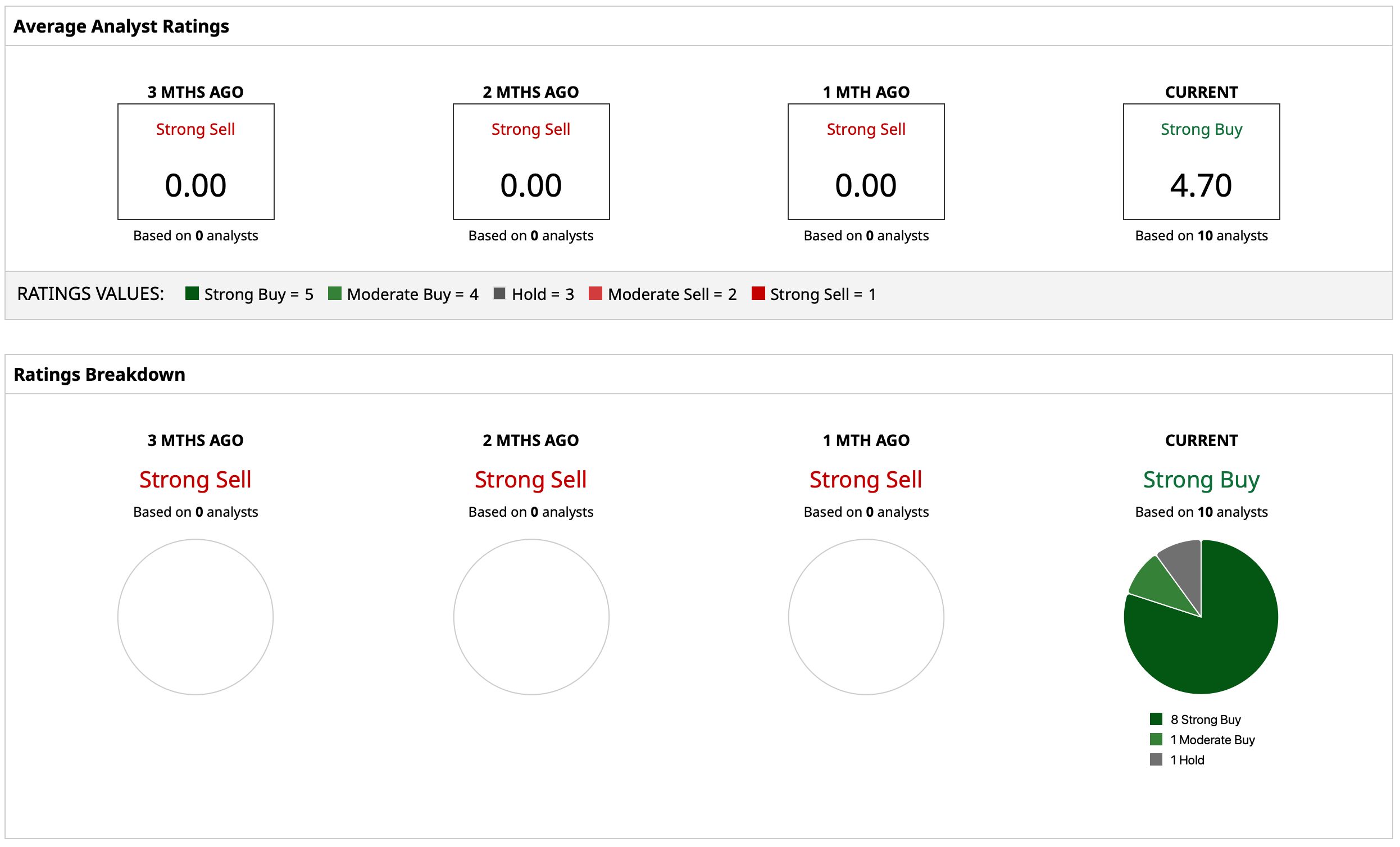

Overall, analysts have assigned a consensus rating of “Strong Buy” for CBRS stock, with a mean target price of $288.89. This denotes an upside potential of about 35% from current levels. Out of 10 analysts covering the stock, eight have a “Strong Buy” rating, one has a “Moderate Buy” rating, and one has a “Hold” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Amkor Technology Is a ‘Picks-and-Shovels’ Winner Up 327% as AI Chip Stocks Lead the Way Attractively Valued Micron Stock Seems Poised for Further Upside After Q3 Earnings Lululemon Shareholders Can Partly Blame Nike for LULU Stock’s Latest Bearish Price Surprise Wedbush Gives a Thumbs Up to Cerebras Ahead of Its First Quarterly Earnings. What This Means for CBRS Stock Investors.