Amazon (AMZN) is heading back to the bond market, this time looking to raise at least $25 billion. The plan, revealed in an SEC filing, splits the debt into eight parts that mature between three and 40 years. Officially, the money is for general corporate purposes, including debt repayment and funding investments. In reality, it’s all about feeding Amazon’s AI infrastructure. Barclays, Goldman Sachs, JP Morgan, and Morgan Stanley are running the deal, with Amazon signaling this to be its last debt raise of the year.

The numbers behind Amazon’s AI push explain the reason it needs the cash. The company plans to spend roughly $200 billion in 2026, a big jump from $131 billion in 2025. Even for a company as cash-rich as Amazon, spending on this scale is hard to fund from cash alone. Prior to this, Amazon had already raised around $54 billion in the U.S. and Europe, along with another $10 billion in Canada. CEO Andy Jassy has defended the heavy spending, calling AI a once-in-a-lifetime opportunity that’s worth betting big on.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Amazon isn’t alone in this. Tech giants, including Alphabet (GOOG) (GOOGL), Meta Platforms (META), and Nvidia Corporation (NVDA), have all rushed to borrow for the same reason. As a result, the global debt related to AI is now around $335 billion this year, more than double last year’s total. Combined, these hyperscalers could spend over $700 billion on AI in 2026. While the demand for this debt has been strong, concerns about whether all this spending will actually pay off are starting to mount.

About Amazon Stock

Amazon is a technology and e-commerce company operating across online retail, digital advertising, cloud computing, and entertainment. Its products and services include its e-commerce marketplace, Amazon Web Services, Alexa, and Prime Video. Founded in 1994, the company is headquartered in Seattle, Washington and led by Jassy.

Year-to-date (YTD), Amazon’s stock has been up 8.95%, almost in line with the S&P 500 Index’s ($SPX) 10.2% gain during the same period. From late March to early May, the stock surged dramatically by 40%. However, the company’s plans to invest roughly $200 billion in 2026 have kept investors concerned about the near-term returns. The investment is primarily aimed at AI infrastructure and data centers, which is what the recent bond sale will help fund.

www.barchart.com

www.barchart.com Amazon’s valuation looks fair given the strength and scale of its business. The forward GAAP price-to-earnings ratio of 28.50 times lacks a meaningful historical average for comparison. The reason is that heavy investment in recent years has distorted the GAAP earnings. The forward price-to-sales ratio of 3.23 times sits just marginally above the 5-year average of 2.90x, indicating a modest premium to its historical norms.

The EPS growth outlook supports the premium. The company is expected to grow steadily through at least 2029 with no real decline in sight. The estimated growth of 21% in 2026, accelerating to 27% in 2028, is significant for a company with a $2.66 trillion dollar market cap already. While the net debt of over $92 billion may seem manageable for now, it explains why investors have been concerned about Amazon continuing to invest heavily.

The AI spending has put pressure on the firm’s free cash flow in the near term. This is why the stock price hasn’t risen much after a genuinely strong quarter. However, the company remaining highly profitable is the reason lenders have been so willing to fund Amazon’s latest bond sale.

Amazon Posts Record Operating Margin As AI Spending Climbs

Amazon reported its first-quarter fiscal 2026 earnings on April 29. Revenue grew 17% year-over-year (YOY) to $181.5 billion, beating the $177.3 billion consensus. AWS surged 28%, marking its fastest growth in the last 15 quarters. The company also posted its highest-ever operating margin of 13.1%, with worldwide operating income reaching $23.9 billion. CEO Andy Jassy noted a growing AWS backlog of $364 billion as a sign of strong demand across its cloud customers.

Looking ahead, Amazon guided second-quarter revenue of $194 billion to $199 billion, above the analyst consensus again. The main worry for investors remains the company’s heavy spending. Amazon plans to invest around $200 billion in capital expenditure in 2026, with most of it directed toward AI infrastructure. The CEO stated that the company will keep investing aggressively in the coming years to meet AWS demand. The management believes that the custom Trainium chips will help save tens of billions of dollars in capex each year while improving margins. The recent bond sale is part of the way Amazon is funding this next phase of AI investment. The company announces its next quarterly earnings on July 30, and you can read more about it at our AMZN earnings preview.

What Analysts Are Saying About Amazon Stock

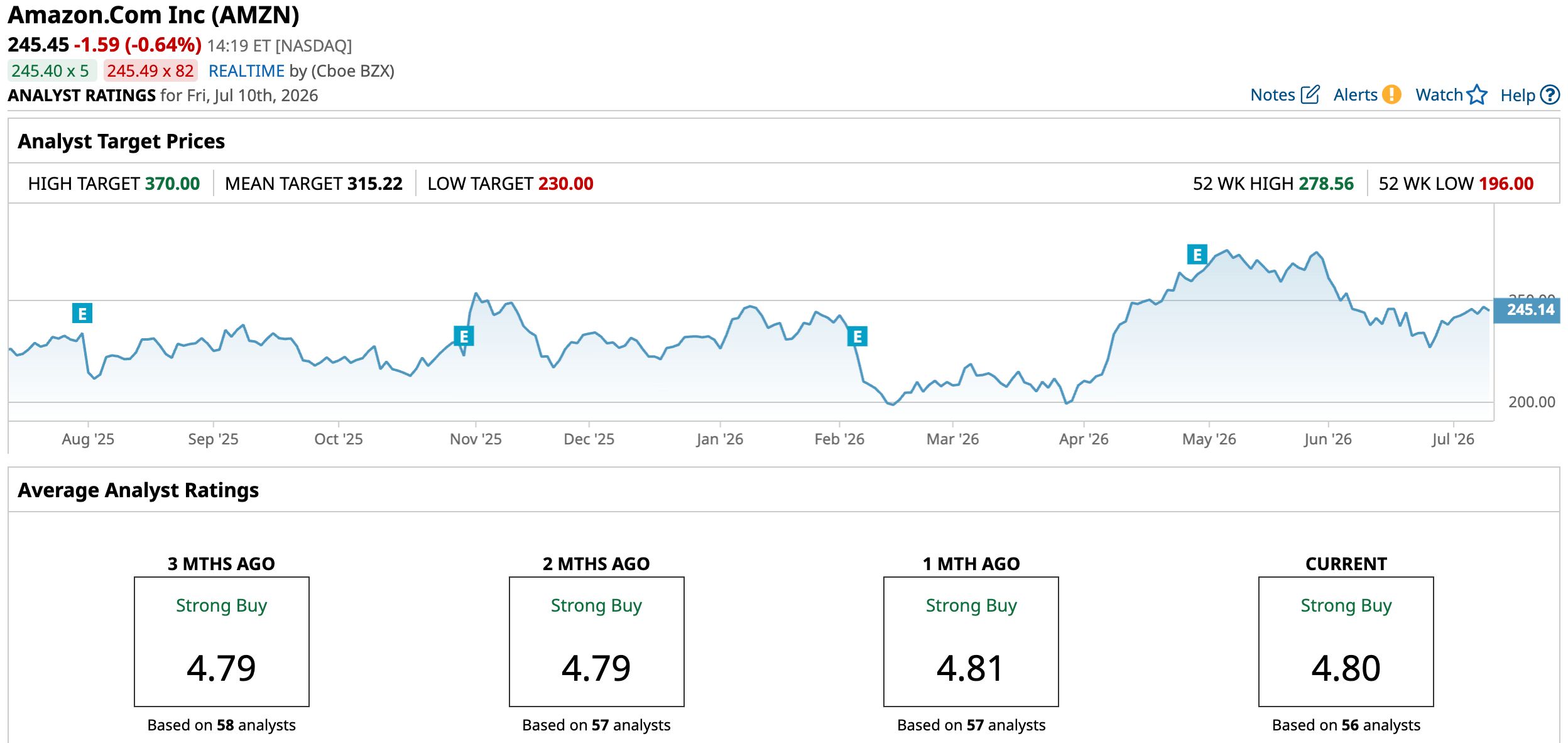

Goldman Sachs analyst Eric Sheridan increased Amazon’s price target from $325 to $335 while maintaining a “Buy” rating. The positive outlook reflects confidence in the firm’s positioning in AI and cloud. While TD Cowen analyst John Blackledge marginally reduced his price target from $350 to $340, the target still sits above the current stock price. The analyst has also maintained a "Buy" rating for Amazon.

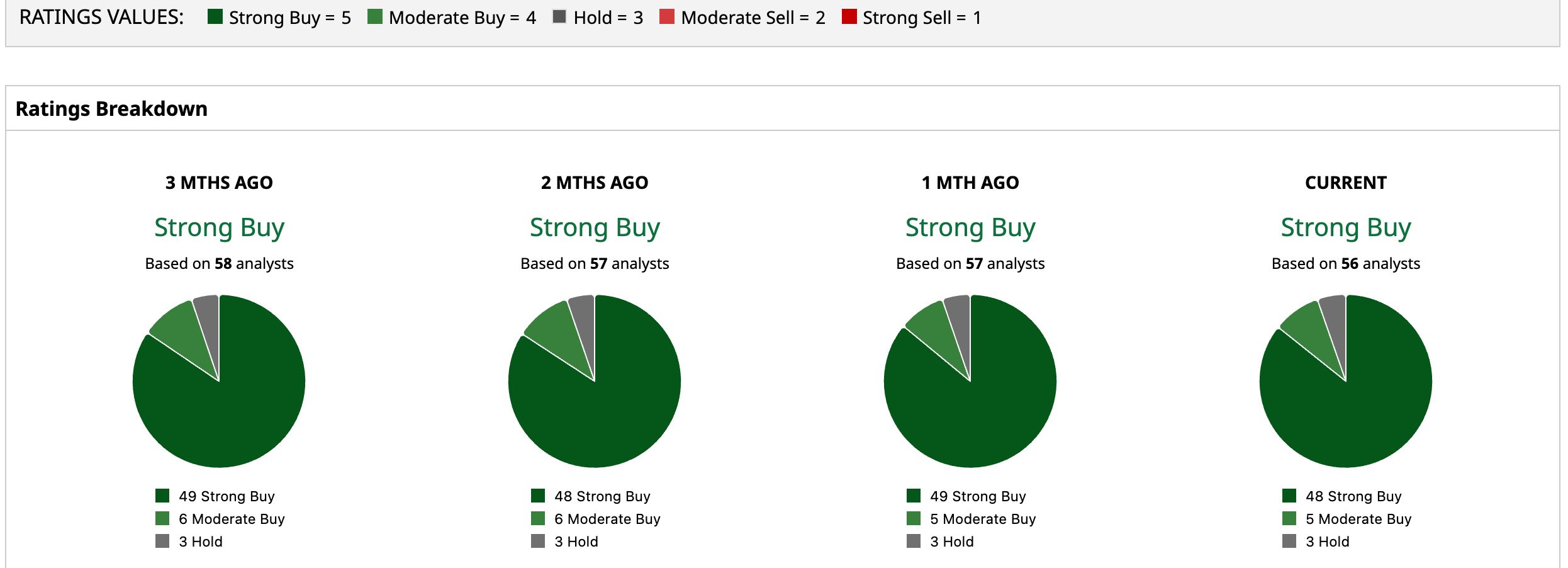

Based on the 56 Wall Street analysts, Amazon holds a consensus “Strong Buy” rating with a mean price target of $315.22, indicating 28.4% upside. Not one analyst suggests selling the stock, with even the lowest price target sitting close to the current stock price. The overall bullish view is supported by Amazon’s continued momentum in AWS.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Broadcom Lands $30 Billion Chip Deal With Apple. Why It’s a Win-Win for AAPL and AVGO. Amazon Is Spending So Much on AI That Even Its Cash Isn’t Enough. Why Investors Shouldn’t Be Worried. A $225 Million Reason to Sell FuelCell Energy Stock Now The 2 Best (and 1 Worst) Single-Country ETFs to Buy from the World Cup’s Round of 16