Things have been getting from bad to worse for FMC Corporation (FMC). The stock is down over 22% for the year and has lost 92% from its all-time high that it reached in April 2022. Currently, it is trading near the lowest price level in over two decades even as the company explores “strategic options,” including a possible sale.

As is usually the case with troubled companies, FMC slashed its dividend by a whopping 86% last year, a possibility I had discussed in one of my articles. However, despite the cut, FMC still has a dividend yield of nearly 3%, which is well over twice the S&P 500 Index ($SPX).

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

In my previous article, I had noted that despite the crash, I would prefer to sit out on FMC. With the stock now down sharply from even those levels, let’s explore whether it is a “buy” now.

www.barchart.com

www.barchart.comWhy Has FMC Stock Been Falling?

Loss of patent protection on some of its most profitable, higher-margin flagship chemicals, particularly the insecticide ingredient Rynaxypyr, has been a key headwind for FMC. This has opened the door for aggressive generic competitors, particularly in Latin America and Asia, leading to lower prices. FMC is also battling intense competition in diamide. To make things worse, the company’s balance sheet is saddled with a lot of debt, which has only increased over the last year.

Working on Deleveraging

FMC had a gross debt burden of $4.5 billion at the end of March, which, for context, is over three times its current market cap. The gross debt to trailing 12-month earnings before interest, tax, depreciation, and amortization (EBITDA) was 5.7x, which is also high for comfort. In order to retire its maturing debt, the company issued secured notes with an interest rate of 8%. However, the new notes would only add to its interest burden as the proceeds would be primarily used to retire its unsecured notes, which carried an interest rate of just 3.2%.

FMC has been working on deleveraging its balance sheet and is targeting a debt reduction of $1 billion. As part of that initiative, it has secured a $400 million equity investment by the Tessenderlo Group and announced a $114 million property sale-leaseback in Newark, Delaware. In May, it announced the sale of its India business for $252 million and expects to close the transaction by the end of this year. Meanwhile, those banking on an outright sale of FMC might be in for disappointment, as the recent asset sales and investment from Tessenderlo Group seem to signal that selling out the company is not the strategic direction that FMC management is considering.

While these transactions would help FMC lower its debt burden, it expects to be only breakeven on free cash flows this year as lower earnings, restructuring expenses, and slightly higher capex would offset improvements in working capital and cash realization from the liquidation of its inventory in India.

FMC Is Bringing New Molecules to the Market

FMC is also looking to structurally lower costs by shifting production to low-cost sources in Asia and expects to complete the process in the first quarter of 2027. It is also working on several new molecules, which would help enhance its revenues over the medium to long term. Earlier this month, it submitted the regulatory dossier for its rimisoxafen to the U.S. Environmental Protection Agency (EPA), which is the first global regulatory submission for the herbicide active ingredient. Previously, in May, it received regulatory approvals for Isoflex active in the EU, which marked the first time since 2019 that the region approved a new herbicide.

Here's Why FMC Stock Looks Like a Buy

FMC expects its earnings to bottom out in the first half of this year and expects sequential improvement beginning in the back half of the year. It expects earnings to rise further in 2027 and 2028—something that analysts are also modeling with current consensus estimates calling for a 32.7% increase in 2027 earnings per share (EPS). The stock trades at a forward price-to-earnings (P/E) multiple of 6.59x, while the 2027 multiple looks even more tempting at under 5x. However, given FMC’s massive debt pile, it would be prudent to look at the forward enterprise value (EV)-to-EBITDA multiple, which is currently 7.68x.

I would bet on FMC stock at these levels as the company turns around the business and addresses its balance sheet issues. It, however, remains a speculative and high-risk buy even though there could be significant upside if the company’s turnaround is successful.

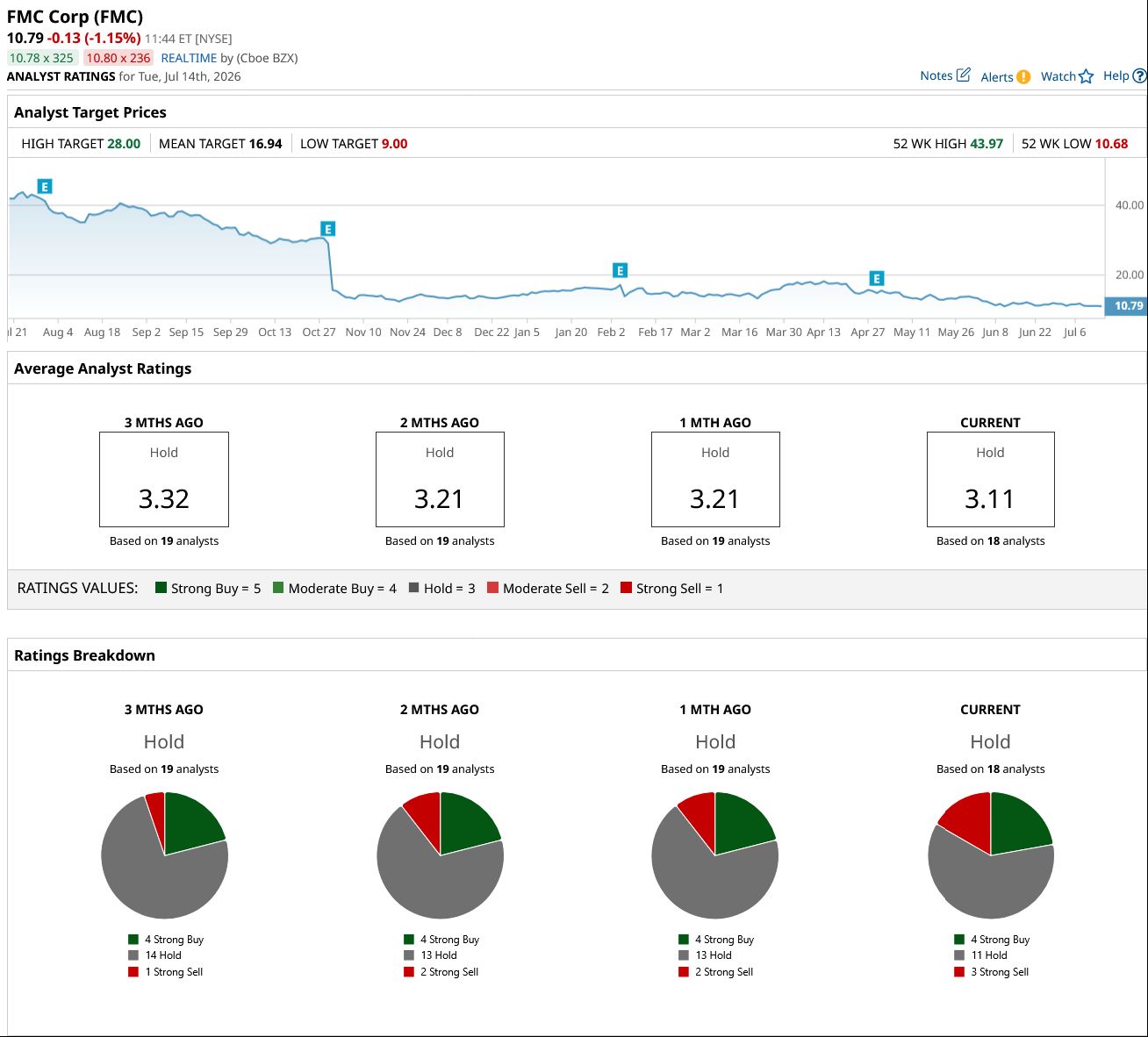

What Analysts Are Saying

Sell-side analysts also see strong upside in FMC, and the mean target price of $16.94 is 55% higher than current price levels. That said, FMC has faced a flurry of downgrades and target price cuts from sell-side analysts over the last couple of years as brokerages revised their ratings to reflect the challenging situation the company finds itself in.

www.barchart.com

www.barchart.com On the date of publication, Mohit Oberoi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

This Dividend Stock Trading Near Multi-Year Lows Is a Risky Buy With Significant Upside Potential Its Dividend Looks Secure, But Don’t Chase JPM Stock After Q2 Earnings. Here’s Why. IBM Stock Suffered an Ugly Earnings Sell-Off. DELL Stock Could Be a Big Winner. Apple Acquired a New Data Observation Startup Called SigScalr. What That Means for AAPL Stock Moving Forward.