Alphabet (GOOG) (GOOGL) will release its second-quarter earnings on July 22. Over the past year, the company has emerged as the best-performing member of the "Magnificent Seven," reflecting the market’s growing confidence in its ability to capitalize on its investments in artificial intelligence (AI) capabilities.

Accelerating AI-driven innovation provides a solid foundation for another strong quarter. As AI becomes increasingly embedded across Alphabet’s products and services, the company appears well-positioned to drive higher user engagement, improve advertising efficiency, and expand its enterprise cloud footprint.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Against this backdrop, there are two key factors that make a bullish case for Alphabet ahead of its second-quarter earnings report.

www.barchart.com

www.barchart.com Advertising Strength to Drive Another Quarter of Double-Digit Revenue Growth

Alphabet has delivered double-digit revenue growth for several consecutive quarters, and that momentum is likely to continue. A resilient digital advertising business, supported by expanding AI capabilities, is expected to remain the primary driver of revenue growth.

The company generated $77.3 billion in advertising revenue during the first quarter, an increase of 15.5% year-over-year (YoY). The growth reflects that Alphabet's aggressive AI investments are producing measurable financial benefits. AI is strengthening its core business by improving advertising performance while creating new monetization opportunities across Google's ecosystem.

Search remains the biggest contributor to Alphabet's advertising business, generating $60.4 billion in first-quarter revenue. AI-powered features, including AI Overviews, are helping boost user engagement, improve search quality, and enhance monetization. As Google continues expanding these AI experiences, Search should remain a dependable growth engine.

YouTube is also benefiting from Alphabet's AI strategy, with advertising revenue increasing 11% in the first quarter. The company is integrating its Gemini models across its advertising platform to improve audience targeting, automate creative optimization, and enhance campaign performance. Better advertising outcomes encourage marketers to spend more, strengthening Alphabet's competitive position and supporting long-term pricing power.

Together, the continued strength of Search and YouTube advertising provides a solid foundation for another quarter of strong revenue growth.

Google Cloud to Sustain Strong Momentum

Another major reason to stay bullish on Alphabet is the explosive momentum in Google Cloud, which remains one of the company's strongest growth engines. Further, AI is playing a key role in accelerating the segment’s growth.

Google Cloud generated $20 billion in first-quarter revenue, up 63% YoY. The momentum will likely continue in Q2, driven by strength in Google Cloud Platform (GCP).

AI solutions could continue to be the biggest contributor to cloud growth, driven by strong customer adoption of Google's industry-leading AI models, including Gemini 3. Infrastructure services are also likely to deliver solid growth as Google continues expanding deployments of GPUs and TPUs to meet rising AI workloads. Beyond AI, core GCP could again remain a major growth engine, benefiting from healthy demand for cloud infrastructure, cybersecurity, and data analytics services. Meanwhile, Google Workspace will sustain momentum, supported by both an expanding customer base and higher average revenue per user.

Google Cloud's profitability continues to improve at an exceptional pace. Operating income surged to $6.6 billion, roughly tripling from a year ago. Meanwhile, operating margin expanded from 17.8% to 32.9%.

The growth story is far from over. Alphabet's cloud backlog has nearly doubled to $462 billion, with management expecting more than half of that contracted business to convert into revenue over the next two years. As enterprises continue investing aggressively in AI infrastructure and applications, Google Cloud appears well-positioned to deliver years of strong revenue growth and higher margins.

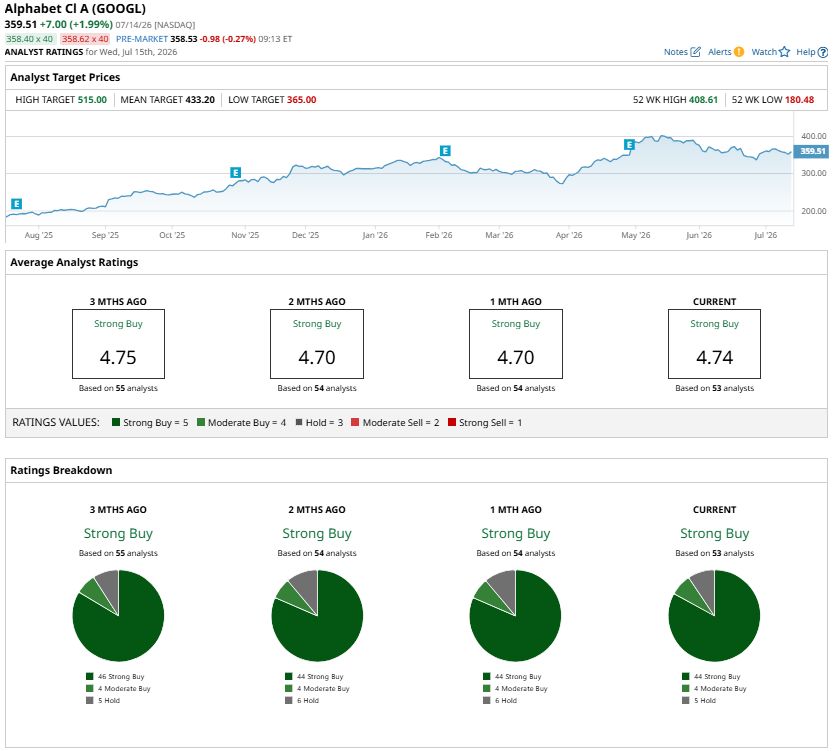

GOOGL Stock Sports a “Strong Buy” Rating

Alphabet’s second-quarter earnings report will likely highlight strong momentum across both its advertising and cloud businesses. AI will continue driving higher engagement, improving monetization, and accelerating cloud adoption. With resilient ad demand, robust Google Cloud growth, expanding profitability, and a sizable backlog providing long-term revenue visibility, Alphabet appears well-positioned to deliver another strong quarter.

Analysts expect Alphabet to report earnings of $2.86 per share in Q2, up 23.8% YoY. Moreover, Wall Street maintains a “Strong Buy” consensus rating on GOOGL stock ahead of Q2 earnings.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

2 Reasons to Feel Bullish on GOOGL Stock Ahead of Alphabet’s Q2 Earnings Stocks Slip Before the Open as Chipmakers Extend Slide, U.S. Retail Sales Data and Earnings on Tap This Dividend Stock Trading Near Multi-Year Lows Is a Risky Buy With Significant Upside Potential AEHR Stock Skyrockets After Q2 Earnings Beat-and-Raise