Circle Internet Group (CRCL) is a global financial technology company founded in 2013 and best-known as the issuer of USD Coin (USDC), the world's second-largest stablecoin by market capitalization. Based in New York, Circle operates a full-stack internet financial platform built around three pillars: Arc Blockchain and Developer Infrastructure, Circle Digital Assets and Services, and Circle Applications.

With USDC representing more than 60% of all stablecoin transaction volume globally, $77 billion in circulation, and a landmark U.S. Office of the Comptroller of the Currency (OCC) approval in July 2026, Circle has emerged as the defining regulated stablecoin infrastructure company at the intersection of traditional finance and decentralized payments.

Join 200K+ Subscribers: Find out why the midday Barchart Brief newsletter is a must-read for thousands daily.

Circle Stock Lags

Circle currently has a market cap of approximately $15 billion, with CRCL stock trading near $61 per share, a long way from the all-time high of $262.97. Circle now trades 23% above the 52-week low of $49.90, while the 52-week range of $49.90 to $262.97 reflects extreme volatility driven by crypto market cycles, interest rate sensitivity, and stablecoin regulatory developments.

Compared to the Russell 1000 Index, which has broadly advanced in 2026 on improving large-cap sentiment, CRCL stock has dramatically underperformed its benchmark on a trailing basis. Shares are down roughly 77% from the all-time high as falling reserve return rates, rising competition from Open USD (OUSD), and broader crypto sector headwinds have weighed heavily on a stock that once commanded a premium fintech valuation.

www.barchart.com

www.barchart.com Circle Delivers Mixed Results

Circle reported first-quarter 2026 diluted EPS of $0.21, beating the Zacks consensus estimate of $0.15 by 40%. Total revenue and reserve income of $694 million grew 20% year-over-year (YOY) but missed the consensus estimate of $715 million by about 3%. Despite the top-line shortfall, USDC onchain transaction volume surged 263% YOY to $21.5 trillion, while USDC in circulation grew 28% to $77 billion at quarter-end, underscoring the explosive adoption of Circle's stablecoin infrastructure across global payments and decentralized finance (DeFi) ecosystems.

Reserve income remained the core earnings engine at $652.5 million, accounting for 94% of total revenue, up 17% YOY. Meanwhile, other revenues doubled to $41.6 million. Adjusted EBITDA grew 24% YOY to $151 million, maintaining a healthy 53% margin, while revenue less distribution costs (RLDC) reached $287 million, up 24% YOY with a margin of 41%. Net income from continuing operations declined 15% to $55 million, reflecting higher distribution costs and a 66-basis-point decline in the reserve return rate to 3.5%, as lower interest rates compressed Circle's yield on USDC reserves.

Management reaffirmed its full-year 2026 outlook, targeting other revenue of $150 million to $170 million, a RLDC margin of 38% to 40%, and adjusted operating expenses of $570 million to $585 million. Looking further ahead, Circle maintained its multiyear through-cycle USDC circulation compound annual growth rate (CAGR) target of 40%, backed by the Arc network — which raised $222 million in a presale at a $3 billion fully diluted network valuation from investors including a16z, BlackRock (BLK), Ark Invest, and Apollo — and the July 2026 OCC approval granting Circle federal banking charter status for First National Digital Currency Bank. The latter is a landmark regulatory milestone that positions the company to compete directly with traditional financial institutions in digital asset custody and settlement.

Circle Downgraded by Mizuho

Circle shares fell after Mizuho Securities downgraded the stock to “Underperform” from “Neutral,” slashing its price target to $50 from $85. That fresh price target implies meaningful downside from current levels.

Analyst Dan Dolev flagged Open USD's pass-through revenue model — which is backed by more than 140 partners including Mastercard (MA), Stripe, and BlackRock — as a structural threat to Circle's core business model. Dolev also warned that Open USD's GENIUS Act compliance and aggressive partner network could fundamentally erode Circle's float-capture economics, with Mizuho's revised 2027 EBITDA estimate coming in approximately 25% below consensus. Adding to the concern, Circle's revenue-sharing agreement with Coinbase (COIN), its largest distributor, is due for renewal in August. Dolev noted that Coinbase's endorsement of Open USD could meaningfully shift the negotiating dynamic against Circle.

Should You Buy CRCL Stock?

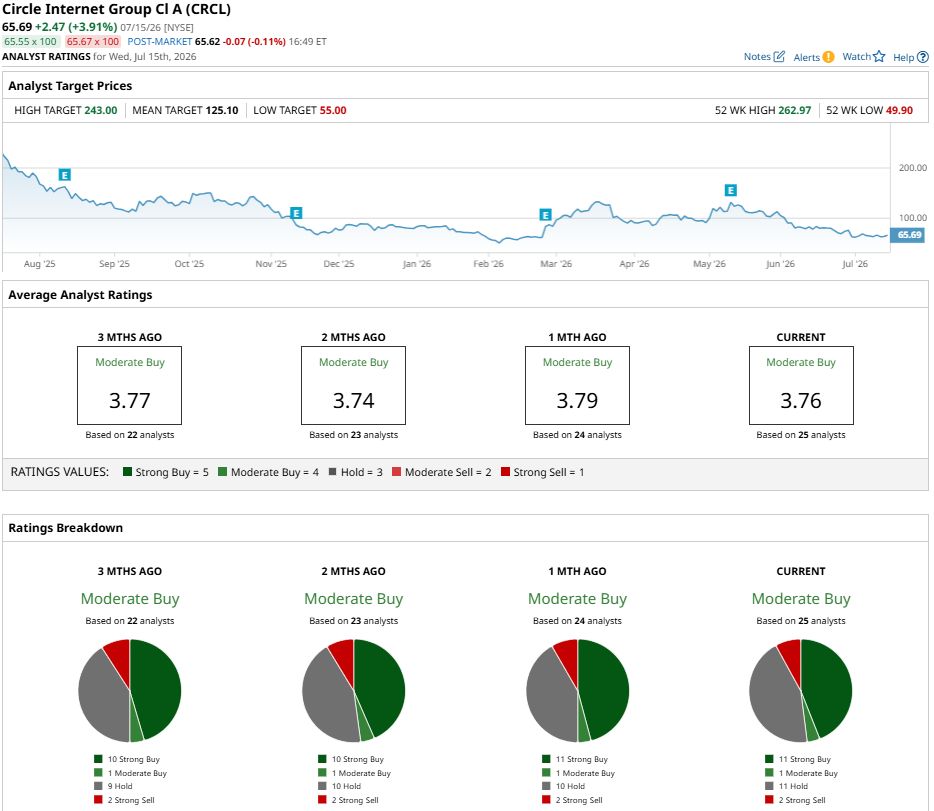

The recent downgrade from Mizuho crystallizes the central bear case for Circle. Still, Wall Street remains broadly optimistic. CRCL stock holds a consensus “Moderate Buy” rating across 25 analyst ratings. That breaks down to 11 "Strong Buy" ratings, one “Moderate Buy,” 11 “Hold" ratings, and two “Strong Sell” recommendations. The mean price target of $121.95 implies striking potential upside of 98% from current levels. A deeply divided analyst picture reflects both the enormous long-term stablecoin opportunity and the very real near-term existential threat that Open USD represents.

www.barchart.com

www.barchart.com On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wall Street Just Punished Netflix’s Guidance, But the Real Story Could Send the Stock Much Higher After This Stock Popped on Earnings, Options Traders Are Betting $6.8 Million on a Short Call Diagonal Spread Why Circle Stock Is the Most Divisive Name in Fintech Right Now Why Piper Sandler Likes AST SpaceMobile (ASTS) Stock Over Other Space Stocks