Shares of ABM ABM have had a decent run over the past month. The stock has risen 7.7% against the industry's 0.9% decline. The Zacks S&P 500 composite fell 0.8% during the said time frame.

ABM has a Growth Score of B. This style score condenses key financial metrics to reflect a fair sense of the quality and sustainability of its growth.

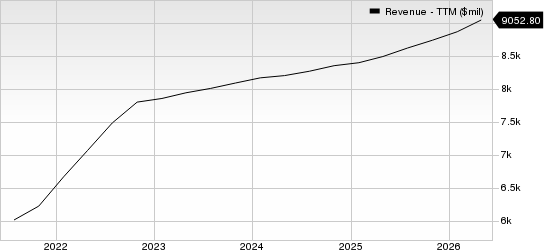

The company’s third-quarter fiscal 2026 earnings are expected to increase 19.5% year over year. Earnings for fiscal 2026 and fiscal 2027 are projected to rise 14.5% and 11.2%, respectively, year over year. Revenues are expected to increase 4.9% in fiscal 2026 and 2.5% in fiscal 2027.

Factors That Bode Well for ABM

ABM Industries is benefiting from its collective growth across segments, primarily driven by Technical Solutions, Aviation, Manufacturing & Distribution (M&D) and Education. The company reported that Technical Solutions revenues increased 27% year over year. Aviation and M&D revenues grew 20% and 17%, respectively, from the year-ago quarter, while revenues from Education rose 2% year over year during the second quarter of fiscal 2026.

ABM Industries Incorporated Revenue (TTM)

ABM Industries Incorporated revenue-ttm | ABM Industries Incorporated Quote

ABM’s Technical Solutions segment benefited from strong demand for data centers, battery energy storage systems and heating, ventilation and air conditioning (HVAC) projects. The company’s Manufacturing & Distribution segment was aided by semiconductor industry investments and technology-sector contract wins. The recent WGNSTAR acquisition has enhanced ABM's capabilities within semiconductor fabrication environments and contributed meaningfully to financial results.

Aviation revenues increased to $310.8 million in the last reported quarter, supported by strong passenger demand and recently awarded contracts, including a major engagement at Heathrow Airport. The Education segment delivered one of the strongest margin performances. In the second quarter of fiscal 2026, revenues from the Education segment increased to $232.2 million, while operating profit rose 19% and operating margin expanded 100 basis points to 7%.

ABM consistently rewards its shareholders through dividend payments and share repurchases. The company paid dividends of $57.5 million, $56.5 million and $65.6 million, while repurchasing shares worth $138.1 million, $56.1 million and $122.2 million in fiscal 2023, 2024 and 2025, respectively. These shareholder-friendly policies enhance shareholder value and make the stock attractive to investors.

ABM’s current ratio (a measure of liquidity) at the end of the second quarter of fiscal 2026 was 1.46, higher than the industry’s 1.13. A current ratio of 1 or more than 1 indicates the company is well-positioned to meet its short-term obligations.

Key Risks to Watch

ABM Industries faces risks from macroeconomic uncertainty, including tariff headwinds and changes in government policies that could raise input costs or delay infrastructure and public-sector projects. Trade tensions and shifting spending priorities may slow contract awards, while elevated labor costs could further pressure margins and temper growth.

ABM faces growing cost pressures as operating expenses weigh on margins and near-term earnings growth. Total operating costs increased by 4.2% in fiscal 2023, 4.1% in fiscal 2024 and 4.7% in fiscal 2025. This underscores the need for stronger cost controls to prevent expense growth from outpacing revenues and eroding profitability. In the second quarter of fiscal 2026, the operating expenses rose 9.3% year over year.

ABM’s Zacks Rank & Stocks to Consider

ABM Industries currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

A couple of better-ranked stocks in the Business Services sector are Trane Technologies plc TT and TransUnion TRU.

Trane Technologies carries a Zacks Rank #2 (Buy) at present. It has a long-term earnings growth expectation of 14.6%.

TT delivered a trailing four-quarter earnings surprise of 2.7%, on average.

TransUnion also holds a Zacks Rank of 2 at present. It has a long-term earnings growth expectation of 13.5%.

TRU beat earnings estimates in each of the last four quarters, with an average earnings surprise of 6.3%.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ABM Industries Incorporated (ABM): Free Stock Analysis Report

Trane Technologies plc (TT): Free Stock Analysis Report

TransUnion (TRU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).