DICK'S Sporting Goods, Inc. DKS started fiscal 2026 on a strong note, delivering a 6% increase in comparable sales in the first quarter, well ahead of many retail peers. The performance was fueled by a 5.5% increase in average ticket and a modest rise in transactions, highlighting both healthy consumer demand and the company's ability to drive higher spending per visit. Management noted that growth was broad-based across footwear, apparel and hardlines, reinforcing the strength of the DICK'S brand and its ability to gain share in a competitive sporting goods landscape.

The numbers behind the quarter underscore the consistency of DICK'S Sporting’s growth story. Comparable sales increased 6%, building on a 10.5% two-year stacked comp increase and a 15.8% three-year stacked comp increase. The company also added approximately 1.5 million new athletes to its customer database during the quarter. Notably, management reported no signs of consumer trade-down behavior across income groups, with customers continuing to spend on both premium and value-oriented products. These trends suggest that DICK'S Sporting is benefiting from strong brand loyalty and continued market-share gains.

Several strategic initiatives are helping support this momentum. The company's experiential retail concepts, including House of Sport and Field House, continue to generate strong traffic, customer engagement and profitability. At the same time, DICK'S Sporting is expanding its digital ecosystem through GameChanger, the DICK'S Media Network and the upcoming AI-powered Coach by DICK'S platform. These investments are creating additional touchpoints with athletes while strengthening the company's omnichannel capabilities and long-term competitive positioning.

Looking ahead, management raised the lower end of its comparable-sales guidance for fiscal 2026 to 2.5%-4%, reflecting confidence in the core DICK'S business despite ongoing macroeconomic and geopolitical uncertainty. While higher supply-chain costs and integration expenses related to Foot Locker remain headwinds, the company continues to benefit from strong merchandise assortments, growing private brands and favorable customer engagement trends. The key question for investors is whether DICK'S Sporting can sustain its market-share gains and comp momentum as comparisons become tougher in the second half of the year.

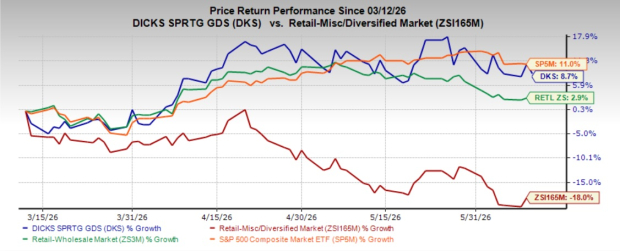

DKS’ Zacks Rank & Share Price Performance

Shares of this Zacks Rank #3 (Hold) company have gained 8.7% in the past three months compared with the broader Retail-Wholesale sector’s 2.9% rise and the S&P 500’s 11% growth. However, the industry has lost 18% during the same timeframe.

DKS Stock's Past Three-Month Performance

Image Source: Zacks Investment Research

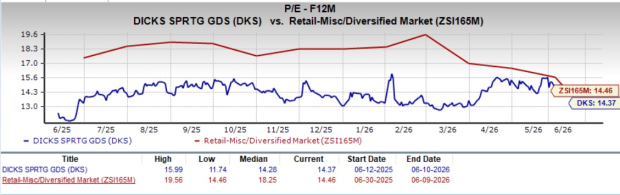

Is DKS a Value Play Stock?

DKS shares are currently trading at a forward 12-month price-to-earnings (P/E) multiple of 14.37X, a discount compared with the industry’s average of 14.46X. At this level, DKS is offering compelling value to investors looking for exposure to the retail sector.

DKS P/E Ratio (Forward 12 Months)

Image Source: Zacks Investment Research

Key Picks

Ross Stores ROST, a leading U.S. off-price retailer operating Ross Dress for Less and dd's DISCOUNTS stores, carries a Zacks Rank #2 (Buy) at present. ROST delivered a trailing four-quarter earnings surprise of 10.2%, on average. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The consensus estimate for Ross Stores’ current fiscal-year sales and earnings suggests growth of 8.6% and 16.3%, respectively, from the year-ago figures.

Five Below, Inc. FIVE, which operates as a specialty value retailer, currently carries a Zacks Rank #2. FIVE delivered a trailing four-quarter earnings surprise of 70.1%, on average.

The Zacks Consensus Estimate for Five Below’s current fiscal-year sales and earnings suggests growth of 14.3% and 30.4%, respectively, from the year-ago figures.

The TJX Companies TJX, a major off-price apparel and home fashions retailer, carries a Zacks Rank #2 at present. TJX delivered a trailing four-quarter earnings surprise of 8.8%, on average.

The Zacks Consensus Estimate for The TJX Companies’ current fiscal-year sales calls for growth of nearly 5.8%, and estimates for earnings suggest an 8.9% increase from the year-ago figure.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The TJX Companies, Inc. (TJX): Free Stock Analysis Report

Ross Stores, Inc. (ROST): Free Stock Analysis Report

DICK'S Sporting Goods, Inc. (DKS): Free Stock Analysis Report

Five Below, Inc. (FIVE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).