Lifetime Brands LCUT continued to make progress in its international business in the first quarter of 2026, delivering sales growth despite ongoing challenges in several overseas markets. Management attributed the improvement to strategic efforts aimed at expanding the company’s presence with larger national retail accounts while improving operational efficiency across international operations. These initiatives helped offset difficult consumer demand trends in parts of Europe, particularly the U.K.

International segment sales increased 10.6% year over year to $12.8 million. Excluding foreign-exchange impacts, sales rose 2.5%, driven by stronger performance in the Asia-Pacific region and increased business with national retail accounts in the U.K. The company noted that its international strategy has shifted away from a historical focus on independent retailers toward larger accounts that offer greater scale and growth opportunities.

Profitability trends also improved across the international segment. The gross margin expanded to 36.7% from 35.3% a year earlier, supported by a more favorable customer and product mix. Distribution expenses as a percentage of goods shipped declined, benefiting from higher sales volumes and improved inventory management at third-party distribution facilities. These improvements demonstrate the company’s focus on creating a more efficient international operating model.

Another contributor to progress has been Project Concord, Lifetime Brands’ international restructuring initiative. The program is designed to streamline operations, reduce overhead costs and improve profitability. While certain legal and structural delays postponed the final phase of the project, management expects the remaining work to be completed in the first half of 2026, providing additional support for future financial performance.

Looking ahead, management remains optimistic about the international business. Greater alignment of product offerings across regions, expanding relationships with national retailers and continued benefits from restructuring efforts are expected to support growth and margin improvement. These initiatives form part of the company’s broader growth strategy, which underpins its fiscal 2026 net sales guidance of $650-$700 million.

ARHS & WSM’s Sales Outlook vs. LCUT

Arhaus ARHS reported first-quarter 2026 net revenues of $314 million, up 0.9% year over year and marking the highest first-quarter revenues in its history. Arhaus saw strength across custom upholstery, outdoor furniture, product launches, and its interior design and trade channels, which continued to drive higher-value projects and customer engagement. Management noted strong customer response to its expanded product assortment and outdoor collections.

Arhaus reiterated its 2026 outlook, projecting net revenues of $1.43-$1.47 billion, indicating growth of 3.7-6.6%, supported by improved inventory availability, marketing initiatives and continued momentum in design and trade businesses.

Williams-Sonoma WSM delivered a strong first-quarter fiscal 2026, with net revenues rising to $1.81 billion and comparable sales increasing 4.8%. Growth was broad-based across the portfolio, with all brands posting positive comps, including strong performances from West Elm, Williams-Sonoma and Pottery Barn Kids. Williams-Sonoma also saw strength in both furniture and non-furniture categories, while its B2B division grew 13.7%, supported by robust trade and contract business demand.

Williams-Sonoma reiterated its fiscal 2026 outlook, expecting comparable revenue growth of 2-6%, total revenue growth of 2.7-6.7% and an operating margin of 17.5-18.1%, reflecting confidence in its growth initiatives despite macroeconomic uncertainty.

LCUT’s Price Performance, Valuation & Estimates

Lifetime Brands’ shares have skyrocketed 129% in the past six months compared with the industry’s growth of 4.9%.

Image Source: Zacks Investment Research

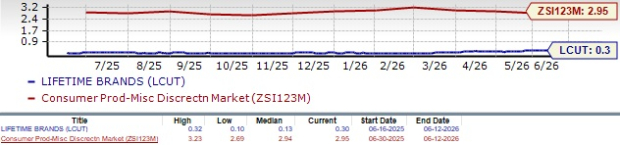

From a valuation standpoint, LCUT trades at a forward price-to-sales ratio of 0.30X, below the industry’s average of 2.95X. It has a Value Score of A.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for LCUT’s 2026 earnings implies a year-over-year decline of 9.9%, whereas the same for 2027 indicates an uptick of 36.3%. Estimates for 2026 and 2027 have been revised upward by 12 cents and 22 cents, respectively, in the past 60 days.

Image Source: Zacks Investment Research

Lifetime Brands currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Williams-Sonoma, Inc. (WSM): Free Stock Analysis Report

Lifetime Brands, Inc. (LCUT): Free Stock Analysis Report

Arhaus, Inc. (ARHS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).