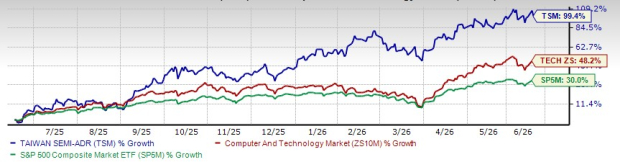

Shares of Taiwan Semiconductor Manufacturing TSM, popularly known as TSMC, have nearly doubled over the past year, significantly outperforming the broader Computer and Technology sector’s 48.2% gain and the S&P 500’s 30% rise.

With TSM stock recently trading around $426, investors are increasingly asking whether the rally has become excessive or whether the company remains one of the most compelling ways to participate in the AI infrastructure buildout.

TSMC: One-Year Stock Comparison

Image Source: Zacks Investment Research

AI Demand Continues to Drive Strong Financial Performance

TSMC has been increasingly attracting investor attention due to its central position in the AI supply chain. Whether it is NVIDIA NVDA, Advanced Micro Devices AMD, Broadcom AVGO, or hyperscale cloud providers designing custom AI chips, most depend on TSMC's advanced manufacturing capabilities. As AI adoption expands, the company stands to benefit from rising chip volumes, growing demand for leading-edge technologies and continued capacity additions. This unique position makes TSMC one of the key enablers of the ongoing AI boom.

Recent results suggest demand remains exceptionally strong. In first-quarter 2026, revenues climbed 39% year over year, while gross margin expanded 740 basis points (bps) to 66.2%. High-performance computing accounted for 61% of total revenues, backed by the growing influence of AI and data-center workloads on the company’s business. Advanced technologies, defined as 7-nanometer and below, represented 74% of wafer revenues.

Management recently noted that AI-related demand remains extremely robust, driven by the transition from generative AI toward agentic AI applications that require greater compute intensity. TSMC raised its 2026 outlook and now expects revenue growth above 30% in U.S. dollar terms while increasing capital spending toward the high end of its $52 billion to $56 billion range.

Capacity Constraints Highlight TSMC's Competitive Position

Supply remains constrained. Management repeatedly emphasized that demand for leading-edge technologies and advanced packaging continues to exceed available capacity and expects conditions to remain tight into 2027. The company is expanding N3 and N2 production globally while continuing to invest aggressively in future nodes such as A14.

Why Some Investors Are Worried

Despite TSMC's strong fundamentals, the stock has nearly doubled over the past year and AI-related names across the semiconductor industry have experienced significant expansions. Any slowdown in AI infrastructure spending, delays in customer deployments, or faster-than-expected capacity additions could eventually moderate growth rates. In addition, TSMC's heavy reliance on a small group of large AI customers means that shifts in spending plans by major chip designers could affect future demand trends.

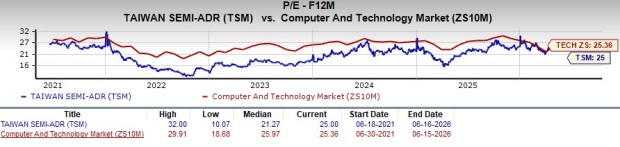

Does the Valuation Signal a Bubble?

Image Source: Zacks Investment Research

TSMC is trading at a forward 12-month P/E of 25.0x, which is below the Computer & Technology sector's 25.36x. Historically, TSM's median forward P/E over the past five years has been about 21.3x. So the stock is trading at a premium to its own history, but not at a significant premium to the broader technology sector despite its superior growth outlook. The higher multiple is supported by accelerating AI demand, industry-leading profitability and management's expectation of more than 30% revenue growth in 2026.

TSMC’s valuation is no longer inexpensive. However, as long as AI infrastructure spending remains elevated and TSMC retains its technology leadership, the company appears positioned to remain one of the primary beneficiaries of the AI supercycle.

Our Take

TSMC's strong share price performance has been supported by improving fundamentals rather than multiple expansion alone. The company continues to benefit from robust AI-related demand, technology leadership in advanced semiconductor manufacturing and persistent supply constraints in leading-edge nodes and advanced packaging. While the stock trades above its historical valuation range, it remains reasonably valued relative to the broader technology sector given its growth profile. With management projecting revenue growth of more than 30% in 2026 and the stock carrying a Zacks Rank #2 (Buy), TSM appears to be a compelling investment at current levels. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Advanced Micro Devices, Inc. (AMD): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Broadcom Inc. (AVGO): Free Stock Analysis Report

Taiwan Semiconductor Manufacturing Company Ltd. (TSM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).