Corpay, Inc.'s CPAY top-line growth is driven by organic expansion, fueled by higher transaction volumes and increased revenue per transaction from key payment services. Its multi-channel approach helps customer engagement, while strategic buyouts enhance its customer base. Strong shareholder-friendly policies are an added advantage.

Meanwhile, higher interest expenses, seasonality issues and foreign exchange risks pose significant concerns for the company. Low liquidity further pressures profitability and scalability.

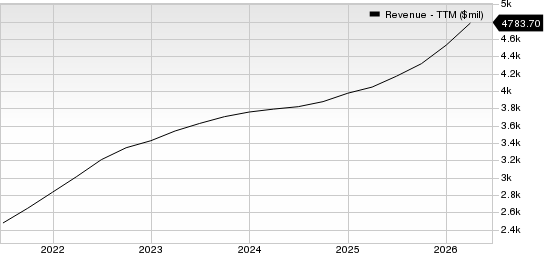

How Is CPAY Faring?

Corpay continues to drive organic growth through higher transaction volumes and increased revenue per transaction in its payment programs. It consistently generates solid organic revenue growth, fueled by increasing sales, improving retention and business initiatives. The company reported organic revenue growth of 10%, 20% and 10% in 2023, 2024 and 2025, respectively.

Corpay, Inc. Revenue (TTM)

Corpay, Inc. revenue-ttm | Corpay, Inc. Quote

The company leverages its multi-channel approach, which integrates comprehensive digital channels, a direct sales force and strategic partner relationships, to effectively market its solutions to existing and prospective customers. It continues to expand its online, end-to-end capabilities, enabling customers to buy, onboard and manage their accounts independently, while allowing its sales force to operate more efficiently by enhancing their prospecting efforts via digitally sourced leads.

Acquisitions and strategic investments have been key drivers of CPAY’s long-term growth, helping to increase its customer base, workforce and operational capabilities, while expanding its range of services across various global industries. The acquisition of GPS Capital Markets in December 2024 expanded its corporate payments business. In the same year, the company acquired Paymerang, which boosted CPAY’s growth and profitability, while strengthening its Corporate Payments segment.

The company consistently rewards its shareholders through share repurchases. It repurchased shares worth $686.9 million, $783 million and $1.3 billion in 2023, 2024 and 2025, respectively. Such moves indicate the company’s commitment to returning value to shareholders and help instill investor confidence in the business.

Meanwhile, Corpay is witnessing higher interest expenses due to an increase in the London Inter-Bank Offered Rate and additional borrowings. Although the growth rate of interest expenses is declining on a year-over-year basis, the bottom line is likely to remain under pressure from higher interest costs. Interest expenses increased 111.7%, 9.8% and 5.4% in 2023, 2024 and 2025, respectively.

CPAY experiences seasonality issues in its fuel card, workforce payment solutions and gift card businesses. The holiday season and fluctuating consumer spending patterns affect its gift card business, resulting in higher revenues during the third and fourth quarters and lower revenues in the first and second quarters. The company’s workforce payment solutions business is affected during the first and fourth quarters due to weather conditions, U.S. holidays, Christmas celebrations in Russia in January, and lower business activity in Brazil due to the summer break and the Carnival celebrations.

CPAY’s global presence exposes it to foreign exchange rate fluctuations. Any appreciation or depreciation of the U.S. dollar against currencies like the British pound, Brazilian real, Canadian dollar, Russian ruble, Mexican peso, Czech koruna, euro, Australian dollar and New Zealand dollar could affect the company’s financial results.

The company’s current ratio (a measure of liquidity) at the end of the first quarter of 2026 was 0.98, lower than the industry average of 1.1. A current ratio of less than 1 often indicates that the company may not be well-positioned to pay off its short-term obligations.

CPAY reported impressive first-quarter 2026 results. It reported earnings of $5.80 per share, which topped the Zacks Consensus Estimate by 5.5% and increased 28.6% from the year-ago quarter. Total revenues of $1.26 billion surpassed the consensus estimate by 4.4% and rose 25.4% year over year.

Corpay currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Earnings Snapshots of Some Other Service Providers

Rollins, Inc. ROL reported impressive first-quarter 2026 results. ROL’s adjusted earnings of 24 cents per share matched the consensus mark and rose 9.1% from the year-ago quarter. ROL’s total revenues of $906.4 million surpassed the consensus mark by 1.3% and increased 10.2% year over year.

Waste Connections, Inc. WCN posted impressive first-quarter 2026 results. WCN’s adjusted earnings of $1.23 per share outpaced the consensus mark by 3.4% and rose 8.9% from the year-ago quarter. WCN’s total revenues of $2.37 billion beat the consensus mark by 0.7% and increased 6.4% year over year.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Waste Connections, Inc. (WCN): Free Stock Analysis Report

Rollins, Inc. (ROL): Free Stock Analysis Report

Corpay, Inc. (CPAY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).