AXT Inc. AXTI appears well positioned for a potentially record-breaking second quarter, as management has indicated that the period could mark the company's strongest-ever quarter for Indium Phosphide revenues. This growth is likely to be driven by surging demand for AI infrastructure and improving shipment visibility.

The company reported $13.6 million in Indium Phosphide revenues in the first quarter, reflecting a significant increase from the previous quarters. On its first-quarter earnings call, management explicitly stated that the second quarter is expected to surpass the company’s previous quarterly revenue record. This anticipated growth is supported by an Indium Phosphide backlog exceeding $100 million, the highest in the company’s history.

A major near-term catalyst is AXTI’s improving revenue visibility despite ongoing export restrictions. Management disclosed that it has already secured approximately $34 million in revenues for second-quarter through shipments that either have export permits in place or do not require permits at all, giving AXT unusually high confidence in near-term execution. This revenue base alone points to continued sequential growth from first-quarter revenues of $26.9 million, reinforcing expectations for accelerating business momentum.

The strongest growth driver remains the booming demand for AI-related optical networking infrastructure. Management highlighted that hyperscaler-driven data center expansion in the United States and rapidly growing AI supply chain investments in China are fueling unprecedented demand for Indium Phosphide wafers. China-related Indium Phosphide revenues more than doubled in the first quarter and are expected to double again in the ongoing quarter, reflecting powerful end-market demand trends.

Importantly, the upside could extend beyond current guidance. Management emphasized that additional export permit approvals could generate significant incremental revenues above the $34 million baseline, potentially enabling AXTI to deliver its strongest-ever quarter for Indium Phosphide revenues.

Peer Updates

MKS Instruments MKSI entered 2026 with strong momentum, and management’s second-quarter outlook suggests the upcycle is accelerating. The company expects second-quarter revenues to be $1.2 billion, up from $1.08 billion in the first quarter. The growth is likely to be supported by high-teens sequential semiconductor revenue growth and over 25% year-over-year expansion.

The biggest catalyst is rising AI-driven semiconductor capital spending, particularly demand for advanced DRAM, NAND upgrades, logic/foundry nodes and backend semiconductor manufacturing. Management highlighted exceptionally strong bookings for remote plasma systems, RF power solutions, dissolved gas systems and photonics products, all critical to advanced chip manufacturing.

With new manufacturing capacity in Malaysia coming online and management expecting a prolonged semiconductor upcycle extending into late 2026, MKSI appears well positioned for sustained revenue acceleration and margin expansion through the remainder of the year.

ASE Technology’s ASX first-quarter results reinforce its position as one of the biggest beneficiaries of the AI semiconductor packaging boom. The company expects 7-9% sequential consolidated revenue growth in the second quarter. However, a bigger story lies in accelerating demand for its advanced packaging business, particularly LEAP services, where management raised its 2026 revenue outlook above $3.5 billion, nearly 10% higher than its prior guidance.

AI-related demand continues to reduce seasonal weakness, with advanced packaging and testing revenues growing despite a typically softer first quarter. Management expects ATM revenues to rise 9-11% sequentially in the second quarter, while margins are projected to improve steadily through 2026 as newly installed LEAP capacity begins ramping meaningfully in the fourth quarter. Management anticipates even stronger incremental LEAP revenue growth in 2027, signaling robust momentum that extends well beyond 2026.

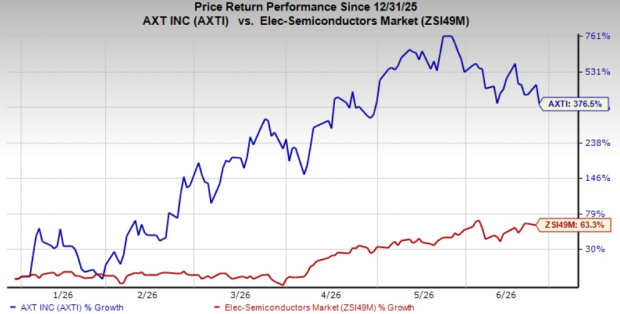

AXTI’s Price Performance, Valuation and Estimates

Shares of AXTI have skyrocketed 376.5% so far this year compared with the industry’s 63.3% growth.

Image Source: Zacks Investment Research

From a valuation standpoint, AXT trades at a forward price-to-sales ratio of 29.5X, significantly above the industry average. It is also higher than its five-year median of 1.48. AXTI carries a Value Score of F.

Image Source: Zacks Investment Research

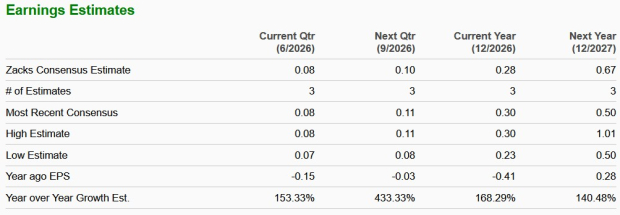

The Zacks Consensus Estimate for AXT’s fiscal 2026 earnings implies a 168.3% improvement from the year-ago period’s level.

Image Source: Zacks Investment Research

The stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

MKS Inc. (MKSI): Free Stock Analysis Report

ASE Technology Holding Co., Ltd. (ASX): Free Stock Analysis Report

AXT Inc (AXTI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).