H.B. Fuller Company FUL presents a familiar value-stock dilemma. The shares look inexpensive, earnings support has improved and the company is pushing into higher-margin medical markets.

The caution is equally real. Volume softness, raw-material inflation, supply disruptions and acquisition-related leverage make this more than a simple low-multiple story.

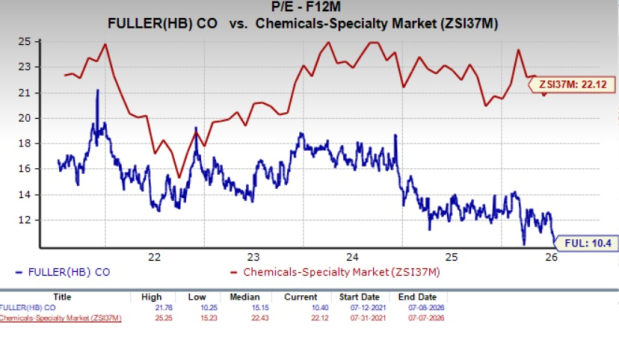

FUL Looks Cheap on Forward Earnings

FUL trades at 10.4X forward 12-month earnings, below the Zacks sub-industry at 22.12X, the Zacks sector at 13.23X and the S&P 500 at 21.14X.

That multiple is also near the bottom of its five-year range of 10.25X to 21.76X, with a five-year median of 15.15X. For value investors, that compression makes FUL worth revisiting.

Image Source: Zacks Investment Research

Avery Dennison Corporation AVY gives investors another materials-science reference point tied to adhesive and labeling markets. RPM International Inc. RPM offers a specialty coatings, sealants and building-products comparison for investors tracking applied-materials demand.

H.B. Fuller Has Earnings Support

The earnings picture has not broken down. The fiscal 2026 earnings estimate has moved 2.1% higher over the past four weeks, while the company’s latest quarter delivered positive sales and earnings surprises.

In the second quarter of fiscal 2026, H.B. Fuller reported adjusted earnings of $1.41 per share, up 19% year over year. Revenues rose 6% to $950.3 million, with organic growth of 2.6%.

Guidance also provides support. Management projects fiscal 2026 adjusted EBITDA of $650-$675 million and adjusted earnings of $4.60-$4.90 per share, excluding the proposed Advanced Medical Solutions acquisition.

H. B. Fuller Company Price and Consensus

H. B. Fuller Company price-consensus-chart | H. B. Fuller Company Quote

Why FUL Is Not a Clean Value Story

The discount is not risk-free. Management’s fiscal 2026 framework includes low- to mid-single-digit volume declines in the second half, with consumer-linked flexible packaging still soft.

Automotive demand also remains weak across regions. That keeps H.B. Fuller dependent on pricing, mix and restructuring savings to defend margins.

Raw materials add another pressure point. Nearly 90% of raw materials were higher sequentially in the second quarter, and more than 50 force majeure events remained in place.

H.B. Fuller and the AMS Risk Tradeoff

The Advanced Medical Solutions deal strengthens the long-term story. The proposed acquisition expands H.B. Fuller’s exposure to procedure-driven medical markets and could improve mix, growth and margins.

The deal is valued at about £715 million and is expected to add roughly $300 million in annual revenues. H.B. Fuller also targets about $55 million in annual revenue and cost synergies by 2031.

The tradeoff is leverage and execution. Pro forma net leverage is expected to be roughly 4X at close, with a target return to 2.5X-3X within two years.

FUL Scores Point to a Mixed Buy Case

The bottom line is that FUL screens attractively, but it is not a clean growth acceleration story. The stock’s value case rests on a low multiple, improving estimates and margin execution, while the risk case rests on volumes, inflation and acquisition leverage.

FUL currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

It also has a VGM Score of A, Value Score of A and Momentum Score of A, which supports the view that the stock has favorable value and sentiment characteristics.

The Growth Score of C keeps the signal balanced. For cautious investors, FUL looks more like a selective value opportunity than a no-risk bargain.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

H. B. Fuller Company (FUL): Free Stock Analysis Report

Avery Dennison Corporation (AVY): Free Stock Analysis Report

RPM International Inc. (RPM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).