Novo Nordisk NVO shares have rallied 11.2% over a month as investors regained confidence in the company's obesity growth story following a series of favorable regulatory, commercial and strategic developments.

A major catalyst was the United Kingdom becoming the first country in Europe to approve the daily Wegovy pill (oral semaglutide 25 mg) for obesity, marking its third global authorization after the United States and the UAE. The approval strengthens Novo Nordisk's leadership in oral GLP-1 therapies while expanding its addressable patient population. NVO expects the approval and launch of the Wegovy pill in other select markets in the second half of 2026.

Momentum strengthened further with the launch of the Medicare GLP-1 Bridge program on July 1, allowing eligible Medicare beneficiaries to access both the Wegovy injection and pill for a $50 monthly copay through 2027. The program significantly expands patient access and follows strong market traction for the Wegovy pill, which surpassed three million U.S. prescriptions in just over five months since its January 2026 launch. Investor confidence also benefited from the Novo Nordisk Foundation's EUR 60.2 million CardioMetabolic Bridge initiative, which aims to accelerate next-generation therapies for obesity, diabetes and cardiovascular disease.

However, NVO continues to face significant challenges. Medicare Bridge also provides identical reimbursement for its rival Eli Lilly's LLY GLP-1 therapies, Zepbound injection and Foundayo pill, for obesity, eliminating any meaningful coverage advantage for Wegovy. Competition is therefore shifting toward clinical differentiation, where Lilly gained momentum with Zepbound's superior weight-loss efficacy in head-to-head studies and Foundayo's more convenient once-daily oral dosing. Although Wegovy retains an important edge as the only obesity therapy approved to reduce the risk of major adverse cardiovascular events, NVO will need to increasingly rely on its broader clinical profile and long-term outcomes to defend market share.

Beyond competitive pressures, Novo Nordisk continues to contend with U.S. pricing pressure, softer injectable GLP-1 prescription trends, reduced Medicaid obesity coverage, the proposed "Most Favored Nation" pricing framework, gradual semaglutide exclusivity erosion and elevated investments in R&D, manufacturing and commercialization. Although management raised guidance after first-quarter results, it still expects declines in both sales and operating profit in 2026, highlighting continued pressure on the core business. Let's delve deeper to better understand NVO's key strengths against its near-term challenges.

Semaglutide — Still NVO’s Primary Top-Line Driver

Novo Nordisk’s growth continues to be driven by its semaglutide franchise — Ozempic [type II diabetes (T2D) injection], Wegovy and Rybelsus (oral pill for T2D) — which forms the backbone of one of the industry’s broadest diabetes and obesity portfolios. Ozempic and Wegovy remain the company’s key revenue generators, while expanded distribution agreements with major U.S. pharmacies, telehealth providers and other platforms have improved access to authentic FDA-approved Wegovy and largely addressed the compounded-drug challenge.

The company is broadening semaglutide’s commercial opportunity through multiple label expansions. Wegovy is now approved not only for obesity but also for reducing major cardiovascular events, improving HFpEF symptoms and easing obesity-related knee pain from osteoarthritis. Novo Nordisk has also secured approvals for higher-dose Wegovy injections in the United States and Europe.

Novo Nordisk is also strengthening its diabetes franchise. Ozempic remains the only GLP-1 approved to slow kidney disease progression and reduce cardiovascular death in T2D patients, while additional label expansions are being pursued in peripheral artery disease. Rybelsus has been approved for cardiovascular-risk reduction in T2D patients in the United States and Europe, and the company recently launched oral Ozempic for adults with T2D. Positive late-stage data in pediatric T2D and planned label-expansion filings for both Rybelsus and oral Ozempic could further expand the reach of its oral GLP-1 portfolio.

NVO’s Competition Heating Up in the Obesity Space

Competition in obesity treatment is intensifying as Eli Lilly has emerged as Novo Nordisk’s biggest rival. Lilly now competes in both injectable and oral obesity therapies with Zepbound and the recently launched oral GLP-1 drug, Foundayo. LLY has further strengthened its position by securing broader reimbursement support from major U.S. pharmacy benefit managers, including CVS Caremark, which should improve patient access and support prescription growth.

The obesity space has drawn much of the spotlight over the past year because of the sizeable and still underpenetrated market opportunity. Smaller biotech firms, such as Viking Therapeutics VKTX and Structure Therapeutics GPCR, are also advancing GLP-1–based therapies to challenge the incumbents. Viking Therapeutics’ dual GIPR/GLP-1 receptor agonist, VK2735, is being developed as both oral and subcutaneous formulations for the treatment of obesity. Viking Therapeutics plans to advance oral VK2735 into phase III development for obesity in the fourth quarter of 2026.

Structure Therapeutics’ phase II ACCESS study on its orally administered GLP-1 RA, aleniglipron, demonstrated significant weight loss across all doses. Structure Therapeutics expects to initiate the late-stage program of aleniglipron in obesity in the second half of 2026.

NVO Expands Footprint in Rare Diseases and Liver Care

Beyond its GLP-1 portfolio, Novo Nordisk is broadening its presence in rare diseases. The company has submitted a regulatory filing seeking approval for Mim8 in hemophilia A in the United States. NVO has also secured both EU and U.S. approvals for Alhemo to treat hemophilia A and B, with or without inhibitors.

The FDA has also granted accelerated approval to Wegovy as the first GLP-1 therapy to treat noncirrhotic metabolic dysfunction-associated steatohepatitis with moderate-to-advanced liver fibrosis. This marked a significant milestone in liver care by offering patients a treatment that can both halt disease activity and reverse liver damage.

NVO Focuses on Next-Generation Drugs

Novo Nordisk is also developing several next-generation obesity candidates in its pipeline, especially targeting the lucrative U.S. market. NVO has submitted a regulatory filing seeking the approval of CagriSema injection, a follow-up drug to Wegovy, for obesity. It is also gearing up to launch a dedicated late-stage program evaluating cagrilintide as a monotherapy for obesity.

Meanwhile, Novo Nordisk’s mid-stage asset, amycretin, has shown strong weight-loss efficacy in a phase II study and is slated to enter phase III soon. The company has bolstered its pipeline through several major collaborations and acquisition deals.

NVO also received FDA approval for Awiqli, the first once-weekly long-acting basal insulin (icodec) for adults with T2D, to be used alongside diet and exercise for glycemic control. Already approved in several global markets, the drug’s U.S. clearance further strengthens its diabetes portfolio and reinforces its position in the treatment landscape.

NVO’s Stock Price, Valuation & Estimates

Year to date, Novo Nordisk shares have lost 3.9% against the industry’s 12.5% growth. The company has also underperformed the sector and the S&P 500 during the same time frame, as seen in the chart below.

NVO Stock Underperforms the Industry, Sector & the S&P 500

Novo Nordisk is trading at a discount to the industry, as seen in the chart below. Going by the price/earnings ratio, the company’s shares currently trade at 14.70 forward earnings, which is lower than 18.86 for the industry. The stock is trading much below its five-year mean of 29.25.

NVO Stock Valuation

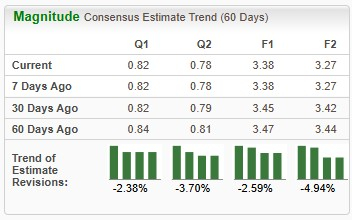

Earnings estimates for 2026 have deteriorated from $3.47 to $3.38 per share over the past 30 days. During the same time frame, Novo Nordisk’s 2027 earnings estimates have decreased from $3.44 to $3.27.

NVO Estimate Movement

Here’s How to Play NVO Stock

While Novo Nordisk, currently carrying a Zacks Rank #4 (Sell), remains one of the strongest franchises in diabetes and obesity care, the recent share price rebound appears to reflect much of the positive near-term news, including expanding access for Wegovy, continued momentum for its oral GLP-1 portfolio and favorable regulatory developments. At the same time, consistent downward earnings estimate revisions underscore investor concerns around slowing growth, pricing pressure and rising competitive intensity. Although the stock now trades at a discount to its historical valuation, a sustained re-rating will likely require clearer evidence that the company can stabilize market share and return to durable earnings growth.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Looking ahead, Novo Nordisk's long-term outlook remains supported by its broad GLP-1 franchise, expanding pipeline and multiple lifecycle management opportunities. However, near-term execution risks remain elevated as Eli Lilly continues to gain traction in both injectable and oral obesity therapies, while policy changes and reimbursement dynamics create additional uncertainty. With meaningful growth drivers already balanced by persistent competitive and operational headwinds, investors may prefer to await stronger evidence of commercial stabilization and improving earnings momentum before becoming more constructive on the stock.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Novo Nordisk A/S (NVO): Free Stock Analysis Report

Eli Lilly and Company (LLY): Free Stock Analysis Report

Viking Therapeutics, Inc. (VKTX): Free Stock Analysis Report

Structure Therapeutics Inc. Sponsored ADR (GPCR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).