Delta Air Lines DAL continues to stand out in a tough airline backdrop, with premium demand, loyalty revenue and corporate travel helping support growth.

The stock’s story is not one-sided. Fuel, labor and recovery-related costs still pressure margins, keeping the risk-reward setup balanced even as Delta’s revenue mix looks stronger than many peers.

Delta Revenue Mix Supports Stability

Delta’s business is not driven only by base ticket sales. Premium products, loyalty travel awards, travel-related services, American Express remuneration and third-party maintenance, repair and overhaul activity all add depth to the revenue base.

That matters in an industry where airfare demand can shift quickly. A more diversified model can help smooth results when leisure pricing softens, fuel rises or corporate demand changes pace.

United Airlines UAL is a relevant comparison because it is also a major U.S. network carrier competing for premium, corporate and international travelers. American Airlines AAL offers another peer reference point for investors evaluating airline revenue mix and balance-sheet sensitivity.

DAL Is Seeing Broad Demand Strength

Delta’s first-half 2026 results showed the value of that mix. Total operating revenues rose 16% year over year to $35.6 billion, while adjusted total revenue per available seat mile increased 10%.

Premium products revenue grew 16%, supported by strong leisure, corporate and loyalty demand. The company also benefited from higher card spend, expanding SkyMiles engagement and growth in third-party maintenance activity.

The strength was not limited to one market. Domestic, Atlantic, Latin America and Pacific passenger revenues all increased in the June quarter from the prior-year period, reinforcing the breadth behind Delta’s demand profile.

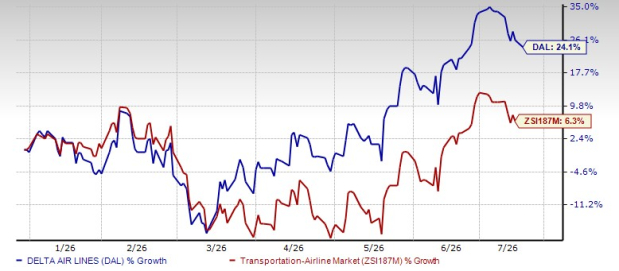

Driven by upbeat air-travel demand, shares of Delta have gained in double digits (% wise) so far this year, outperforming its industry, despite high fuel costs.

YTD Price Comparison

Delta Balances Growth With Capacity Discipline

Delta’s lower-capacity bias should be viewed as a margin-protection strategy rather than a weak demand signal. In a high-cost environment, adding capacity too aggressively can dilute pricing and expose earnings to fuel volatility.

Management has emphasized protecting margins while recapturing higher fuel costs. That approach is especially important when macro conditions remain uneven and consumer behavior can shift quickly.

For investors, the discipline is central to the outlook. Airlines do not win only by filling more seats. They also need to fill the right seats at profitable fares while controlling how much cost they add to the system.

DAL Cash Flow Keeps Flexibility Intact

Delta’s financial flexibility remains a key support. The company ended the June quarter with $7.7 billion of liquidity, including $3.1 billion of undrawn revolver capacity.

Debt reduction also remains part of the story. Adjusted net debt was $13.6 billion at quarter-end, down $709 million from the end of 2025.

Delta is still investing in the business while returning capital to shareholders. The company affirmed its full-year 2026 free cash flow outlook of $3-$4 billion and announced a 15% increase to its dividend beginning in the September quarter.

That balance gives DAL room to invest in aircraft, technology and customer experience while continuing to support its investment-grade balance sheet.

Delta Signals Show Balanced Momentum

The bottom line is that Delta has several attractive operating traits, but the stock is not free of risk. The company’s premium demand, loyalty engine and cash generation support the case for resilience.

At the same time, fuel costs, wage inflation and capacity decisions can quickly affect airline margins. That explains why the stock’s current signals are constructive but not decisive.

DAL currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The stock also has a VGM Score of A, with a Value Score of A and Momentum Score of A.

Those scores point to favorable valuation and trading characteristics. The Growth Score of C is more measured, reinforcing the idea that DAL’s outlook is solid but still tied to cost volatility and execution.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Delta Air Lines, Inc. (DAL): Free Stock Analysis Report

United Airlines Holdings Inc (UAL): Free Stock Analysis Report

American Airlines Group Inc. (AAL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).