Independent refiners continue to benefit from a favorable industry backdrop, supported by healthy crack spreads, resilient fuel demand, constrained global refining capacity and ongoing geopolitical tensions in the Middle East, which have contributed to uncertainty in energy markets. Companies that can efficiently operate their refining assets while maintaining financial discipline are well positioned to capitalize on these favorable market conditions.

Two notable players in the sub-industry are Delek US Holdings, Inc. DK and PBF Energy Inc. PBF. While both operate diversified refining systems across the United States, their investment stories are quite different. Delek is building on operational improvements and the steady growth of its logistics business to drive more consistent earnings. PBF, meanwhile, is focused on completing the turnaround of its Martinez refinery while lowering costs through company-wide efficiency initiatives. With both companies benefiting from improving refining fundamentals, which stock deserves investors' attention today?

Delek Builds on Operational Strength

Delek entered 2026 with improving operational momentum despite reporting a GAAP net loss in the first quarter. The company generated adjusted EBITDA of $211.7 million, a sharp improvement from $33.6 million in the year-ago quarter, while adjusted earnings per share came in at 8 cents in the first quarter. Higher benchmark crack spreads, which climbed nearly 64% year over year, played a major role in supporting the company's profitability.

The refining segment remained Delek's primary earnings driver, generating adjusted EBITDA of $155.3 million following the successful completion of the planned turnaround at its Big Spring refinery. In addition, Delek Logistics continued to provide stable cash flows by delivering adjusted EBITDA of $132.4 million, supported by stronger wholesale margins and higher third-party volumes.

Another positive for Delek is its Enterprise Optimization Plan. Management expects the initiative to generate nearly $220 million in annual cash flow improvements, which should further strengthen profitability over time. Combined with its diversified business model, these initiatives provide Delek with greater earnings visibility and reduce its dependence on refining margins alone.

PBF Offers a Compelling Turnaround Opportunity

Unlike Delek, whose investment case is centered on operational consistency, PBF's investment thesis depends largely on the successful recovery of its refining operations.

The company reported first-quarter net income attributable to shareholders of $198.3 million, benefiting from insurance recoveries and improving operations following the Martinez refinery outage. Although adjusted earnings remained under pressure due to temporary operational challenges, management expects Martinez to return to planned operating rates shortly, restoring one of the company's most valuable assets.

PBF is also making steady progress through its Refining Business Improvement ("RBI") initiative. The program generated more than $230 million in annualized savings during 2025 and management expects cumulative annualized savings to exceed $350 million by the end of 2026. Along with nearly $1 billion in insurance recoveries related to the Martinez incident, these cost-saving initiatives could significantly improve earnings as refinery utilization normalizes.

While PBF's recovery story carries greater execution risk than Delek's, it also provides meaningful upside potential if management successfully delivers on the turnaround strategy.

DK vs. PBF: Performance, Valuation and Growth Outlook

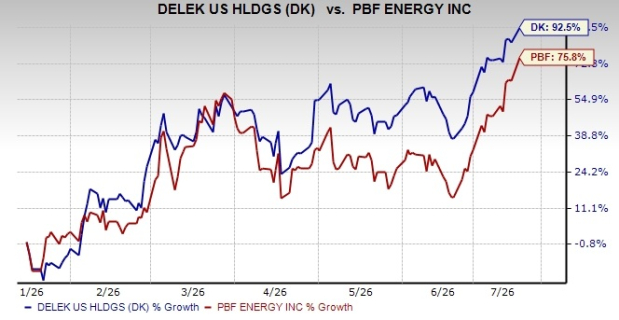

Both companies have benefited from improving industry conditions, but investors have rewarded Delek more aggressively. Over the past six months, DK’s shares have rallied 92.5%, outperforming PBF's impressive 75.8% gain. The stronger share-price performance reflects investors' confidence in Delek's consistent execution, operational improvements and diversified earnings base.

Image Source: Zacks Investment Research

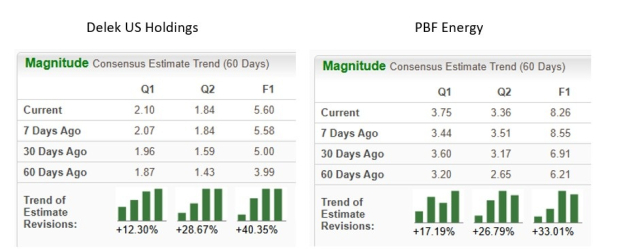

Market has also become increasingly optimistic about both refiners.

Image Source: Zacks Investment Research

Over the past 60 days, the Zacks Consensus Estimate for 2026 earnings has increased 40.35% for DK and 33.01% for PBF. The upward estimate revisions suggest analysts expect refining fundamentals to remain supportive while company-specific initiatives continue to improve earnings.

Valuation, however, paints a different picture.

Image Source: Zacks Investment Research

Delek currently trades at a forward 12-month P/E multiple of 14.73X, while PBF trades at just 7.89X. Although Delek commands a premium valuation due to its stronger operational execution and more diversified earnings streams, PBF's discounted multiple could offer attractive upside if the Martinez refinery continues operating smoothly and the RBI program delivers its targeted savings.

Which Stock Should Investors Choose?

Both Delek and PBF currently carry a Zacks Rank #3 (Hold), meaning neither stock has a ranking advantage. Instead, investors should evaluate the companies based on their risk tolerance and investment objectives. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Delek appears better suited for investors seeking a more balanced investment. The company benefits from improving refinery operations, stable cash flows from its logistics business and ongoing optimization initiatives that are expected to enhance long-term profitability. These strengths provide greater earnings visibility and justify its premium valuation. PBF, on the other hand, is the more aggressive investment choice.

The successful restart of the Martinez refinery, expanding cost savings under the RBI initiative and substantial insurance recoveries could drive a meaningful earnings rebound over the next several quarters. However, the investment thesis remains more dependent on flawless execution.

Overall, Delek stands out as the stronger all-around investment due to its operational momentum, diversified earnings profile and stronger financial visibility. PBF remains an attractive turnaround story and investors willing to accept higher execution risk may be rewarded if management successfully delivers on its recovery plans. For conservative investors, however, Delek's consistent execution and more predictable growth profile make it the better choice today

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Delek US Holdings, Inc. (DK): Free Stock Analysis Report

PBF Energy Inc. (PBF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).