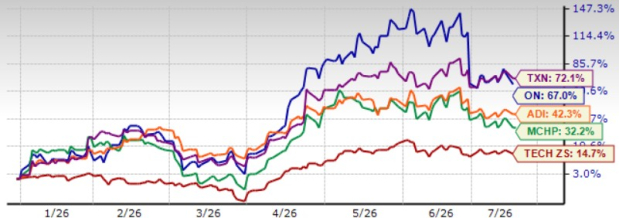

On Semiconductor ON or onsemi shares have jumped 67% year to date (YTD), outperforming the Zacks Computer and Technology sector’s appreciation of 14.7%. The outperformance can be attributed to strong demand for AI infrastructure, strong order levels, expanding automotive share and rapid commercialization of Treo intelligent sensing and networking products. The Synaptics acquisition expands ON’s long-term AI story.

Nevertheless, we believe the appreciation in onsemi shares will be limited in the near term due to volatility in the automotive end-market as well as stiff competition from the likes of Microchip MCHP, Analog Devices ADI and Texas Instruments TXN. Shares of Microchip, Analog Devices and Texas Instruments have returned 32.2%, 42.3% and 72.1%, respectively, YTD. So, what should investors do with the ON stock? Let’s dig deep to find out.

ON Stock’s Price Performance

Image Source: Zacks Investment Research

AI, Expanding Portfolio & Synaptics Buyout Aid ON’s Prospects

ON’s AI data center business has become a major growth engine. In the first quarter of 2026, AI data center revenues grew more than 30% sequentially, more than double year over year, and materially exceeded management's expectations. Onsemi now expects AI data center revenues to double in 2026, supported by wins across multiple XPU vendors, all leading hyperscalers and more than 30 active programs with Flex Power. This diversification reduces dependence on automotive while exposing onsemi to one of the fastest-growing semiconductor markets.

In terms of the automotive end-market, onsemi continues to gain share through higher semiconductor content rather than vehicle volume growth. The company maintained roughly 55% silicon carbide share among new EV models introduced at the Beijing Auto Show, won new 900V EV platform programs with NIO and Geely, expanded IGBT traction inverter wins with North American OEMs and continued benefiting from Chinese EV exports.

ON’s expanding portfolio has been a key catalyst. The rapid commercialization of Treo intelligent sensing and networking products, Gallium Nitride (GaN) power devices and next-generation automotive Ethernet solutions bodes well for onsemi’s prospects. Treo’s revenues increased more than 2.5 times sequentially, while the GaN design funnel exceeded $1.5 billion, positioning the company for new revenue streams beginning in 2027.

The announced acquisition of Synaptics significantly broadened onsemi’s long-term prospects. The company expects the transaction to expand its addressable market by $30 billion, creating a $243 billion total addressable market by 2030, while extending onsemi from AI infrastructure into physical AI, robotics, edge AI, industrial automation and connected computing. Management estimates a roughly $100 billion AI opportunity by 2030 at about 25% CAGR. The acquisition is expected to become earnings accretive within 18 months after closing, providing an additional long-term growth narrative beyond power semiconductors.

ON Suffers from Automotive Uncertainty & Stiff Competition

Although onsemi continues to win silicon carbide, IGBT and automotive Ethernet programs, global automotive production remains volatile, particularly outside China. The company has acknowledged that the recovery is being driven more by higher semiconductor content per vehicle than by unit volumes, leaving revenues exposed if EV demand or OEM production weakens further. Automotive still represents the company's largest end market, making macro uncertainty an important near-term headwind.

The company is facing intensifying competition from Infineon, STMicroelectronics, Wolfspeed, Microchip and Rohm in silicon carbide power devices. Analog Devices, Texas Instruments, Monolithic Power Systems and Infineon are competing aggressively in AI power semiconductors. Moreover, ON is facing integration and regulatory risks with the Synaptics acquisition.

ON’s Earnings Estimate Revision Shows Steady Trend

For the second quarter of 2026, onsemi guided revenues of $1.535-$1.635 billion and expects non-GAAP earnings in the range of 65-77 cents.

The Zacks Consensus Estimate for second-quarter 2026 earnings is pegged at 71 cents per share, unchanged over the past 60 days and indicating 33.96% growth over the year-ago quarter’s reported figure. The consensus mark for second-quarter 2026 revenues is pegged at $1.59 billion, suggesting 7.92% growth from the year-ago quarter’s reported figure.

ON Semiconductor Corporation Price and Consensus

ON Semiconductor Corporation price-consensus-chart | ON Semiconductor Corporation Quote

ON Shares Are Overvalued

onsemi shares are overvalued as suggested by a Value Score of D.

In terms of the forward 12-month price-to-earnings (P/E), the company is trading at 23.99X, higher than the median of 19.60X. Its peers Microchip, Analog Devices and Texas Instruments trade at 25.21X, 27.99X and 36.17X, respectively.

ON Stock’s Valuation

Image Source: Zacks Investment Research

Conclusion

ON is executing well on several strategic priorities, with AI infrastructure, expanding automotive content, Treo commercialization and the Synaptics acquisition strengthening its long-term growth profile.

However, much of this optimism appears reflected in the stock after its 67% YTD rally. Persistent automotive demand uncertainty, rising competition across power semiconductors and integration risks related to Synaptics could limit near-term upside. Given the stock's rich valuation and balanced risk-reward profile, investors may be better served by holding ON shares while monitoring execution on its AI and diversification strategy.

ON currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ON Semiconductor Corporation (ON): Free Stock Analysis Report

Analog Devices, Inc. (ADI): Free Stock Analysis Report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

Microchip Technology Incorporated (MCHP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).