Citigroup Inc. C used its second-quarter call to make a broader point than the headline beat. Management framed the quarter as evidence that the bank’s multiyear rebuild is producing stronger earnings power, while also creating room to invest more aggressively for future returns.

That message mattered because analysts pressed hard on why Citi kept its full-year return target unchanged despite a strong first half. Management’s answer was clear: it wants flexibility to accelerate organic investments, structural efficiency moves and funding actions rather than optimize for a single near-term waypoint.

Citi Ties the Quarter to a Stronger Franchise

Chair and CEO Jane Fraser said the quarter marked Citi’s best quarterly revenue in a decade, with double-digit growth for the firm and in four of five businesses. She emphasized that the result was not just market-driven, but tied to prior investments, tighter execution and a more durable earnings profile.

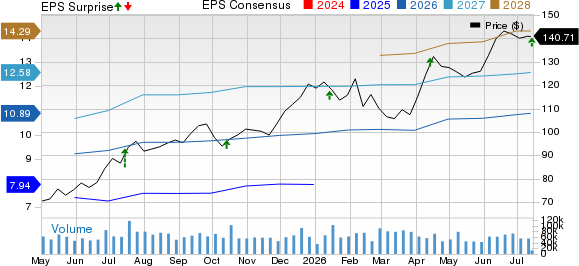

Citi reported revenue of $24.77 billion and EPS of $3.15, both ahead of the Zacks Consensus Estimate of $23.68 billion and $2.72, respectively.

Citigroup Inc. Price, Consensus and EPS Surprise

Citigroup Inc. price-consensus-eps-surprise-chart | Citigroup Inc. Quote

Fraser also pointed to capital return as a sign of confidence. Citi plans to raise its dividend by 12% and launched a $30 billion common stock repurchase program, with $4 billion bought back during the quarter and about $5 billion returned through buybacks and dividends overall.

C Benefits From More Than One Engine

Management highlighted that Services posted its highest quarterly revenue ever, with revenue up 18% and RoTCE above 30%. Fraser and CFO Gonzalo Luchetti both tied that performance to deeper client relationships, operating deposit growth and continued demand for cross-border capabilities.

Markets also remained a major contributor. Revenue rose 17%, with Equities up 45% and prime balances up nearly 60%, while Fixed Income benefited from strength in foreign exchange, spread products and commodities.

Banking and Wealth added to the breadth story. Banking revenue climbed 34%, helped by a 44% jump in investment banking revenue, while Wealth revenue rose 13% for a ninth straight quarter as client investment assets grew 14% and net new investment assets strengthened.

Citi Defends Its Full-Year Return Target

The central tension in the Q&A was Citi’s decision to keep its full-year 2026 RoTCE target at 10% to 11% even after generating 13.1% year to date. Luchetti said management wanted to preserve room for second-half seasonality, especially in Markets, and for a range of macro outcomes.

He also reaffirmed the full-year efficiency ratio target of around 60%, NII excluding Markets growth of about 5% to 6%, and a total U.S. credit card net credit loss rate of 4% to 4.5%.

What changed on the call was the emphasis. Fraser repeatedly told analysts Citi was focused on its near-term and medium-term return targets, not on maximizing a 2026 waypoint, and said a constructive environment would be used to pull forward investments that can support higher sustainable returns.

C Pushes Harder in Consumer Cards

U.S. Consumer Cards was the clearest example of that strategy. Revenue rose just 1%, but management said the business absorbed deliberate investment in products, partnerships and customer acquisition, including the onboarding of an additional American Airlines co-branded portfolio with more than $6 billion in loans and over 2 million accounts.

Luchetti said expenses are expected to grow faster than revenue for the next few quarters as Citi invests in engagement and acquisitions. He stressed that the bank is comfortable doing so because Cards is a high-returning business, with second-quarter RoTCE at 22%.

Management also sounded constructive on credit. Luchetti said the U.S. consumer remains resilient, with card delinquencies and net credit losses down year over year and performance running in line with or better than expectations.

Citi Sees More Room on Efficiency and Capital

Another important theme was self-help. Citi reduced headcount to 219,000 and incurred more than $800 million of severance year to date, as management continues to remove stranded costs, lower temporary transformation expenses and push productivity gains through technology and AI.

Fraser said much of the remediation work tied to Citi’s consent orders has now passed internal audit validation and can be handed to regulators. She added that Citi is already reducing related expenses as bodies of work are completed, rather than waiting for formal closure.

On capital, Citi ended the quarter with a 12.8% CET1 ratio, about 120 basis points above its current regulatory minimum. Luchetti also pointed to improving stress test results and a $500 million year-to-date reduction in disallowed deferred tax assets as evidence that the balance sheet story is improving alongside earnings.

C Keeps Playing the Long Game

The clearest takeaway from the call was tone. Citi did not argue that the second half must weaken. Instead, management argued that stronger operating momentum gives it more choices on where to invest and how quickly to execute structural actions.

That made the Q&A less about whether Citi could exceed its full-year target and more about whether it should optimize for that number. Fraser’s answer was that the bank is now in a position to think more about durability, market share and medium-term returns than about managing to a single annual figure.

What Zacks Signals Say on C

C carries a Zacks Rank #3 (Hold), along with a Value Score of D, Growth Score of C, Momentum Score of A and VGM Score of C. Under Zacks’ framework, the Rank is the first screen because it reflects earnings estimate revisions, while Style Scores serve as complementary indicators over a similar one- to three-month horizon. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

That combination points to stronger momentum characteristics than value or broad style appeal right now. Zacks also notes that stocks with the most favorable return profiles typically pair a Zacks Rank #1 or #2 (Buy) with Style Scores of A or B, while a Zacks Rank #3 can still be held with attention to the score hierarchy. The Zacks Rank can change as analysts revise estimates after the quarter.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Citigroup Inc. (C): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).