Robinhood Markets HOOD and StoneX Group SNEX are financial services companies that connect clients with global markets through brokerage, trading and investment platforms. However, their business models, customer bases and growth profiles differ considerably.

SNEX operates a diversified financial services franchise spanning commercial hedging, institutional execution, clearing, payments and retail trading. HOOD, meanwhile, has evolved from a commission-free trading application into a broader consumer financial platform offering brokerage, cryptocurrency, retirement, banking, advisory and credit products.

StoneX offers exposure to global transaction volumes and institutional risk-management demand, while Robinhood provides a more direct play on the digitization of personal finance and the growing participation of younger investors in capital markets.

Both Robinhood and StoneX are well-positioned to benefit from the growing demand for brokerage and financial services. However, their distinct business models, growth trajectories and risk profiles make the investment choice less straightforward. A closer comparison of their financial performance, profitability, growth prospects and valuations should reveal which brokerage stock offers the more compelling risk-reward opportunity in the current market.

The Case for Robinhood

Robinhood primarily targets individual investors through a technology-driven platform. Its revenues come from transaction-based activities, interest earned on customer balances and margin loans, subscription fees, securities lending and other financial products.

The company’s performance is consequently influenced by retail trading activity, cryptocurrency markets, interest rates and customer asset growth. This was further reinforced by Robinhood’s first-quarter 2026 results, which demonstrated that it is no longer dependent on a single trading category. This points to increasing wallet share. Customers are not only trading through Robinhood but are also transferring more assets, borrowing on margin, saving for retirement, subscribing to Gold and adopting newer banking, credit and advisory products.

HOOD is attempting to become a comprehensive financial platform rather than merely an online broker. The company is also expanding internationally and entering additional markets, including Canada and the Asia-Pacific. Its acquisition of Bitstamp broadened its cryptocurrency capabilities and institutional reach, while its initiatives in private markets, tokenization, futures and event contracts increase the number of products it can offer existing users.

Each new service creates potential cross-selling opportunities. Robinhood can acquire a customer through stock or cryptocurrency trading and subsequently offer that customer a retirement account, subscription, credit card, managed portfolio or banking product. This ecosystem approach could raise revenue per customer and reduce the company’s long-term dependence on transaction-based revenues.

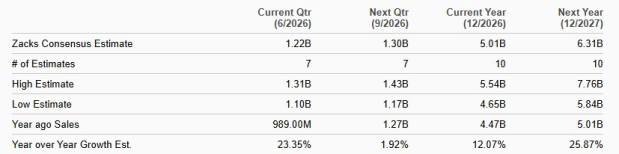

This supports steady top-line growth across market cycles. The Zacks Consensus Estimate for sales indicates 12.1% and 25.9% growth for 2026 and 2027, respectively.

Sales Growth

Image Source: Zacks Investment Research

The Case for StoneX

StoneX serves a broader mix of commercial, institutional and retail clients. Its services include commodity risk management, listed and over-the-counter derivatives, securities execution, foreign exchange, clearing, physical commodities and cross-border payments. The company has more than 80,000 institutional, commercial and payments clients, along with more than 400,000 self-directed retail accounts, across almost 180 countries.

StoneX has been expanding its operations, product capabilities and global presence through targeted acquisitions. Recent buyouts include R.J. O’Brien, Benchmark, Bamboo, Octo, JBR and Right Corporation in fiscal 2025, followed by WCS International Ltd, Plantureux et Associés and Intercam Securities and Intercam Advisors in fiscal 2026. These have helped the company expand across commodities, wealth management, clearing, investment banking, payments, fixed income, metals and agricultural brokerage.

StoneX is rolling out AI-enabled automation across settlement instruction repair, validation, reconciliation and client service chatbots to increase straight-through processing in Payments, while also accelerating software delivery across the organization. The company’s breadth across listed and OTC derivatives, securities, physical commodities, payments and self-directed retail clients has converted the recent heightened volatility into record net operating revenues.

As of March 31, 2026, average client equity plus money market/FDIC sweep balances reached almost $15.2 billion, reinforcing recurring net interest/fee income alongside transactional activity. This multi-segment, volatility-levered business model will likely continue to monetize client activity through commissions, spreads, fees and interest, positioning the company to compound revenues if volatility and client engagement remain elevated.

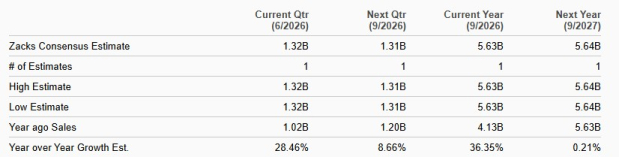

The Zacks Consensus Estimate for sales indicates 36.4% and 0.2% growth for fiscal 2026 and fiscal 2027, respectively.

Sales Growth

Image Source: Zacks Investment Research

Valuation Favors StoneX, Growth Favors Robinhood

Valuation is the clearest argument for StoneX. SNEX is currently trading at a 12-month trailing price-to-book (P/B) of 3.33X, substantially below HOOD’s 10.55X.

P/B TTM

Image Source: Zacks Investment Research

HOOD’s premium leaves less room for execution problems. A slowdown in trading volumes, weaker cryptocurrency activity, regulatory restrictions, falling interest income or disappointing adoption of new products could pressure the shares. It also faces regulatory uncertainty surrounding payment for order flow, cryptocurrency services and event contracts.

Meanwhile, StoneX carries different risks. Its businesses involve credit, counterparty, liquidity and market exposures, while its acquisition-driven strategy creates integration and execution challenges. The R.J. O’Brien deal has meaningfully expanded the company, but it has also increased expenses, financing requirements and operational complexity.

Nonetheless, despite Robinhood’s richer valuation, its premium reflects a substantially larger consumer opportunity and a more scalable technology platform. The company’s rapid deposit growth, expanding product portfolio and strong engagement suggest it can compound revenue beyond traditional brokerage activities.

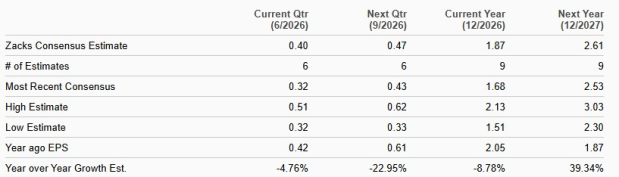

Analysts seem to be of this view too. Over the past week, the Zacks Consensus Estimate for HOOD’s earnings has been revised upward to $1.87 and $2.61 for 2026 and 2027, respectively. This suggests that though earnings are expected to fall 8.8% this year, the trend will reverse in 2027, with earnings projected to soar 39.3%.

HOOD Earnings Estimates

Image Source: Zacks Investment Research

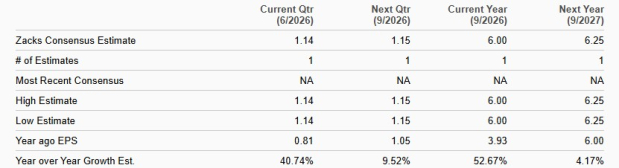

On the other hand, SNEX’s earnings estimates have remained unchanged over the past seven days at $6 for fiscal 2026 and $6.25 for fiscal 2027. This reflects earnings growth of 52.7% and 4.2% for fiscal 2026 and fiscal 2027, respectively.

SNEX Earnings Estimates

Image Source: Zacks Investment Research

The Smarter Buy: Robinhood or StoneX?

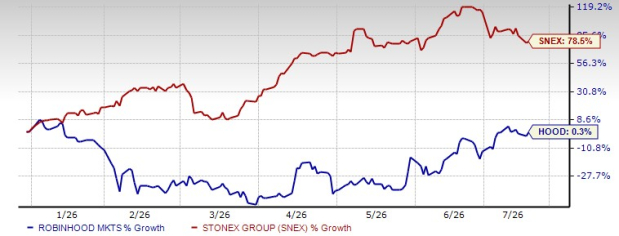

So far this year, shares of Robinhood have gained just 0.3%, while the StoneX stock has jumped 78.5%. Hence, in terms of investor sentiment, SNEX has the edge.

YTD Price Performance

Image Source: Zacks Investment Research

StoneX is an attractive financial services company with diversified operations, strong institutional capabilities and considerably lower earnings multiple. Value-oriented investors seeking steadier exposure to global trading, clearing and risk-management activity may prefer SNEX.

Robinhood, however, appears to offer the stronger long-term upside. Its customer assets and deposits are growing rapidly, Gold subscriptions are expanding, margin and retirement balances are reaching records, and newer businesses such as banking, advisory, credit, prediction markets and international crypto are widening its revenue opportunity.

While valuation demands continued execution, making HOOD more volatile and less suitable for highly risk-averse investors, the combination of customer growth, product innovation, operating leverage and expanding wallet share gives it a more powerful growth runway. For investors willing to tolerate valuation and regulatory risks in exchange for higher growth potential, Robinhood is the better brokerage stock to bet on now.

At present, HOOD carries a Zacks Rank #2 (Buy), while StoneX carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

StoneX Group Inc. (SNEX): Free Stock Analysis Report

Robinhood Markets, Inc. (HOOD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).