MP Materials Corp. MP has become more than a rare earth mining story. Its shift into separated products, metal, alloy and magnet manufacturing gives investors a clearer view of a domestic supply chain buildout.

The harder question is price. MP’s operating progress is improving, but the stock still carries a premium valuation while the company ramps several capital-intensive projects at once.

Why MP Stock Has Started Looking More Credible

MP’s first-quarter 2026 results made the business model look more tangible. Revenues rose 49% year over year to $90.6 million, beating the Zacks Consensus Estimate of $75 million. Adjusted earnings were three cents per share, above the consensus mark of a loss of one cent.

Adjusted EBITDA was $36.6 million against a loss of $2.7 million a year earlier. Operating cash use narrowed to $1.9 million from $63.2 million, helped by higher product sales, prior-quarter price protection collections and a $19 million 45X credit receipt.

MP produced a record 917 metric tons of NdPr up 63% year over year, while NdPr sales volumes rose 117% to 1,006 metric tons. That supports the case that separated rare earth output is moving into measurable volume growth.

Why MP Materials Still Looks Expensive

Valuation is the biggest obstacle to a clean buy case. MP trades at 13.78X forward 12-month sales, well above 1.59X for the Zacks sub-industry, 2.6X for the Zacks Basic Materials sector and 5.06X for the S&P 500.

The premium also sits above MP’s own five-year median of 11.32X, although the multiple has ranged from 5.59X to 38.89X over that span. Investors are already paying for a sizable portion of the future buildout.

The near-term upside case looks tempered. The $52 price target is only modestly above the $49.46 stock price as of July 15, 2026. Execution gains still need to keep arriving.

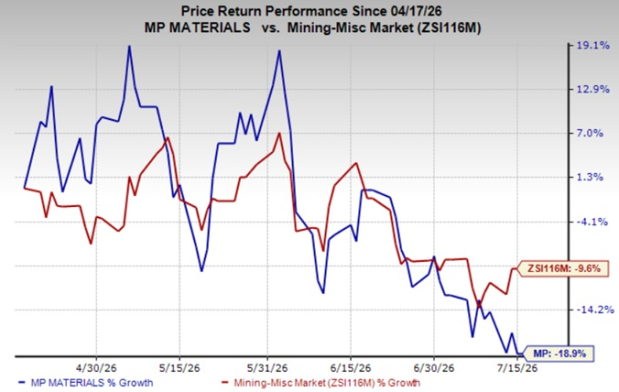

Shares of MP have declined 18.9% in the past three months against the industry’s 9.6% fall.

What Keeps MP From a Cleaner Bull Case

MP still has a profitability problem. The company has reported operating losses for 11 consecutive quarters as it shifts from concentrate sales toward higher-value separated rare earth products.

The cost base is rising with the strategy. Cost of sales climbed 52% in the first quarter of 2026 due to higher sales volumes of NdPr oxide, metal and magnetic precursor products. Selling, general and administrative expenses rose 39.2%, while start-up costs surged 503%.

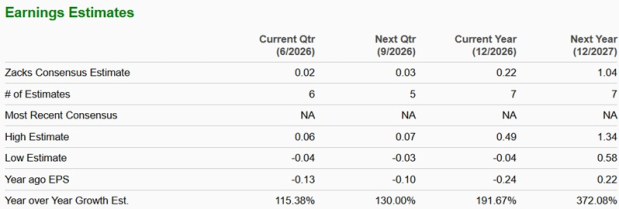

The Zacks Consensus Estimate for MP Materials’ 2026 earnings is pegged at 22 cents per share, indicating an improvement from the loss of 24 cents in 2025. The estimate for 2027 is $1.04 per share, indicating a 372% year-over-year improvement.

Image Source: Zacks Investment Research

However, both the estimates have been revised downward, as shown in the chart below.

Image Source: Zacks Investment Research

The downstream transition remains unfinished. Independence is ramping magnet manufacturing and qualification, Mountain Pass is moving toward heavy rare earth production, and the 10X facility requires construction and commissioning. Any delay in customer acceptance, yield improvement or qualification could push revenue and cash flow further out.

How Liquidity Strengthens the MP Materials Case

MP’s balance sheet is a key reason the story remains investable despite those risks. Cash, cash equivalents and short-term investments totaled $1.74 billion as of March 31, 2026, compared with $1.83 billion at the end of 2025.

The company also had no borrowings under its $275 million revolving credit facility and $203 million of remaining borrowing capacity. That liquidity gives MP room to fund Mountain Pass investments, heavy rare earth refining, Independence scale-up and 10X construction.

Albemarle Corporation ALB gives investors exposure to another minerals supply chain tied to electrification. Energy Fuels Inc. UUUU, a producer of uranium, rare earth elements and other critical minerals, reflects domestic resource security interest.

What MP Ratings Say About Investor Timing

MP’s setup looks more balanced than one-sided. The stock currently carries a Zacks Rank #3 (Hold), which fits a company showing operational improvement but still facing valuation, cost and execution hurdles. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Style Scores send a similar message. MP has a Momentum Score of A, pointing to stronger market interest and estimate-revision support. However, its Value Score of F, Growth Score of D and VGM Score of D argue against treating the stock as a high-conviction buy at the current entry point.

For now, MP offers a credible domestic rare earth growth platform with enough liquidity to keep building. The stock’s premium valuation and unfinished operating ramp make patience more appropriate than aggressive buying.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

MP Materials Corp. (MP): Free Stock Analysis Report

Albemarle Corporation (ALB): Free Stock Analysis Report

Energy Fuels Inc (UUUU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).