DexCom, Inc. DXCM is well positioned for growth in the coming quarters, supported by the significant potential of the continuous glucose monitoring (CGM) market. A strong fourth-quarter 2025 performance and a series of favorable coverage decisions are expected to contribute further. Risks related to stiff competition persist.

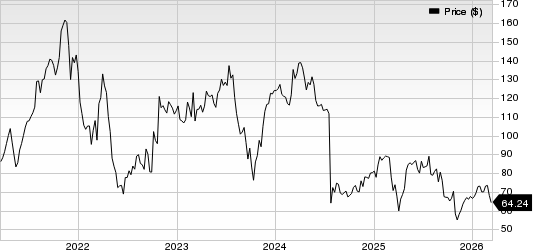

This Zacks Rank #3 (Hold) company’s shares have lost 16% in the past six months compared to the industry’s 7.3% growth. The S&P 500 Index has gained 1.3% in the same time frame.

DXCM, a renowned medical device company and provider of continuous glucose monitoring (CGM) systems, has a market capitalization of $24.72 billion. It projects a 20.6% growth rate over the next five years and anticipates maintaining a strong performance going forward.

Image Source: Zacks Investment Research

DexCom’s earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters and missed in one, the average surprise being 3.82%.

Let’s delve deeper.

Expanding Addressable Market Through Type 2 Diabetes Coverage: DexCom’s long-term growth outlook is supported by the expanding coverage landscape for CGM devices, particularly among type 2 diabetes patients not using insulin. Management highlighted that Medicare coverage expansion for this population could unlock access for nearly 12 million additional patients, significantly enlarging the addressable market.

Private insurers have already begun expanding coverage for non-insulin users, supported by growing clinical evidence demonstrating improved health outcomes and cost savings. As reimbursement broadens globally, DexCom is well positioned to drive sustained user growth and strengthen its leadership in the CGM market.

Product Innovation Led by G7 15-Day Sensor Platform: DexCom’s innovation pipeline remains a critical growth catalyst, highlighted by the rollout of the G7 15-day sensor, which extends wear duration while improving accuracy and reliability. Early feedback from physicians and patients has been positive, with the longer wear time reducing sensor replacements and enhancing patient convenience. The company expects the platform to gradually replace earlier sensors across its portfolio, providing both margin expansion and broader market reach. Over time, the 15-day platform may also enable DexCom to penetrate emerging markets where longer wear cycles help reduce overall cost per patient.

Strong International Growth Momentum: DexCom’s international segment continues to outpace its U.S. business, with 18% reported revenue growth in the fourth quarter and 15% organic growth. Strong demand across key markets such as Germany, the U.K. and France highlights the company’s success in expanding CGM access globally.

In France, expanded reimbursement for type 2 diabetes patients significantly accelerated adoption, demonstrating the scalability of DexCom’s evidence-driven market access strategy. Management believes the long-term opportunity outside the United States could eventually surpass the domestic market as coverage improves and the company expands into additional countries.

Downsides

Increasing Competitive Pressure in the CGM Market: The CGM market remains highly competitive, with rival technologies launching new sensors and expanding international presence. DexCom management acknowledged that competitors are actively introducing new products and expanding distribution globally.

While the company believes its accuracy and product ecosystem provide differentiation, competitive pricing, reimbursement access and technological innovation from rivals could pressure its market share in certain regions. Sustaining leadership in the CGM category will require continued investment in both hardware and digital platforms to maintain clinical and technological advantages.

Margin Volatility From Manufacturing Expansion: DexCom’s profitability outlook faces near-term pressure from investments in manufacturing capacity, particularly the planned ramp-up of its Ireland production facility. During the early stages of operation, the facility will generate fixed overhead costs before reaching full production capacity, which management expects to weigh on gross margins temporarily. While the facility should improve long-term supply-chain scalability and cost efficiency, the transitional period could create short-term margin volatility and raise operating expenses in 2026.

Dependence on Coverage Decisions for Future Growth: DexCom’s growth trajectory remains closely tied to reimbursement decisions by government programs and insurers. Management emphasized that its 2026 outlook assumes the current coverage environment remains largely unchanged, underscoring the sensitivity of revenue projections to potential reimbursement policy shifts.

Delays in Medicare decisions for non-insulin type 2 patients or slower-than-expected payer adoption could limit new patient additions and slow revenue growth. Given the company’s reliance on expanding reimbursement to drive adoption, regulatory or policy delays remain a key uncertainty for long-term demand.

Estimate Trend

DexCom has witnessed a positive estimate revision trend for 2026. In the past 30 days, the Zacks Consensus Estimate for 2026 earnings per share has moved up 2 cents to $2.49.

The consensus mark for the company’s first-quarter revenues is pegged at $1.18 billion, indicating a 13.6% improvement from the year-ago quarter’s reported number. The consensus estimate for first-quarter earnings is pinned at 47 cents per share, implying an improvement of 46.9% year over year.

DexCom, Inc. Price

DexCom, Inc. price | DexCom, Inc. Quote

Stocks to Consider

Some better-ranked stocks in the broader medical space are Intuitive Surgical ISRG, Align Technology ALGN and Cardinal Health CAH.

Intuitive Surgical, sporting a Zacks Rank #1 (Strong Buy), has an estimated long-term growth rate of 15.7%. ISRG’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 13.24%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Intuitive Surgical’s shares have gained 8.9% against the industry’s 7.3% decline over the past six months.

Align Technology, carrying a Zacks Rank #2 (Buy), has an estimated long-term growth rate of 10.1%. ALGN’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 6.16%.

ALGN’s shares have climbed 26.9% compared with the industry’s 16.7% growth over the past six months.

Cardinal Health, carrying a Zacks Rank of 2, has an estimated long-term growth rate of 15%. CAH’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 9.3%.

CAH’s shares have rallied 46% compared with the industry’s 16.7% growth over the past six months.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Align Technology, Inc. (ALGN): Free Stock Analysis Report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

DexCom, Inc. (DXCM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).