Amazon’s AMZN Online Stores segment is gaining traction as a steady driver of retail revenue growth, supported by improving demand quality and a favorable category mix. The rising contribution of high-frequency purchase categories is strengthening customer engagement and increasing repeat transactions within the platform.

A key catalyst is the rapid expansion of everyday essentials and grocery, growing twice as fast as other categories in the United States and accounting for one in three units sold. These categories drive higher purchase frequency, enabling Amazon to deepen wallet share and improve revenue visibility. As more consumers rely on the platform for routine consumption, Amazon is reinforcing its position as a primary shopping destination rather than a discretionary marketplace.

This demand strength is further supported by selection expansion across beauty, fashion and value-oriented assortments. A broader product range enhances discovery and conversion, enhancing discovery and conversion while competitive pricing anchors the platform's retail value proposition. These factors are driving sustained volume growth, with paid units increasing 12% year over year in the fourth quarter of 2025, reflecting healthy underlying demand trends.

Fulfillment infrastructure investments have amplified this momentum. Same-day delivery coverage now reaches more than 2,300 cities and towns across the United States, compressing the purchase-to-delivery window and reinforcing consumer preference for the platform. The Add to Delivery feature accounts for 10% of weekly Prime-fulfilled volume, indicating further consolidation of household spend within the ecosystem.

However, macro uncertainties, including geopolitical risks and potential pressure on discretionary spending, could temper near-term momentum. The Zacks Consensus Estimate for AMZN's first quarter 2026 online stores revenues is pegged at $62.8 billion, up 9.4% year over year. Indicating that the durability of demand-led growth will be key to sustaining further retail upside.

Competitive Intensity in Online Stores

Amazon’s Online Stores segment competes with eBay EBAY and Etsy ETSY in driving online marketplace engagement. eBay focuses on value-driven and resale categories, while Etsy caters to niche, handcrafted and personalized goods, both emphasizing discovery-led transactions.

Unlike Amazon’s frequency-driven model anchored in essentials, eBay and Etsy rely more on discretionary and occasion-based purchases. While eBay and Etsy benefit from asset-light marketplace structures, Amazon’s Online Stores strategy is more tightly integrated with high-frequency consumption, enabling stronger repeat purchase behavior and customer retention.

AMZN’s Share Price Performance, Valuation & Estimates

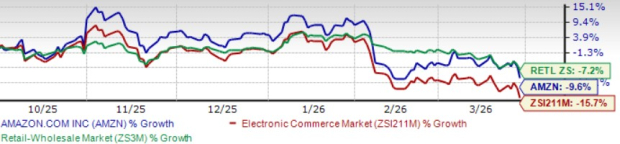

Amazon shares have declined 9.6% in the past six-month period compared with the Zacks Internet – Commerce industry and the Zacks Retail-Wholesale sector’s decline of 15.7% and 7.2%, respectively

AMZN’s 6-Month Price Performance

Image Source: Zacks Investment Research

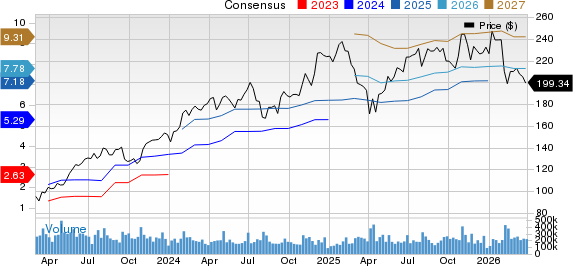

From a valuation standpoint, AMZN stock is trading at a forward 12-month price/earnings ratio of 24.46X, higher than the industry’s 20.48X. Amazon has a Value Score of C.

AMZN’s Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for AMZN’s 2026 earnings is pegged at $7.78 per share, indicating an 8.51% increase from the figure reported in the year-ago quarter.

Amazon.com, Inc. Price and Consensus

Amazon.com, Inc. price-consensus-chart | Amazon.com, Inc. Quote

Amazon currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

eBay Inc. (EBAY): Free Stock Analysis Report

Etsy, Inc. (ETSY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).