Ulta Beauty Inc. ULTA is showing that demand for beauty products remains solid, even as consumers stay careful with spending. Its fourth-quarter fiscal 2025 update suggests shoppers are still buying beauty products, but they are paying closer attention to value, affordability and where they spend. The bigger question now is not whether demand is there, but how long this strength can continue if economic pressures remain.

The latest quarterly numbers support the idea that demand is still healthy. In the fourth quarter of fiscal 2025, comparable sales rose 5.8%, backed by a 4.2% rise in average ticket and a 1.6% jump in transactions. For the full year, comparable sales rose 5.4%, with average ticket up 3.3% and transactions increasing 2%.

Net sales climbed 11.8% in the quarter to $3.9 billion and 9.7% in fiscal 2025 to $12.4 billion. These results show that shoppers were not only spending more per visit but were also continuing to make purchases in a category that has remained relevant, even in a cautious spending environment.

However, the tone around demand is balanced rather than overly optimistic. Ulta Beauty pointed to continued consumer resilience during fiscal 2025, but also noted a strong focus on value and affordability. Beauty engagement remained healthy, yet the company also acknowledged broader economic volatility and rising global conflicts as factors that could affect consumer behavior in fiscal 2026.

Image Source: Zacks Investment Research

Caution shows up in the Zacks Rank #3 (Hold) company’s guidance. Ulta Beauty expects beauty category growth in the 2%-4% range in fiscal 2026, in line with historical averages. Its comparable sales growth outlook of 2.5% to 3.5% also suggests demand should remain intact, though at a more normalized pace.

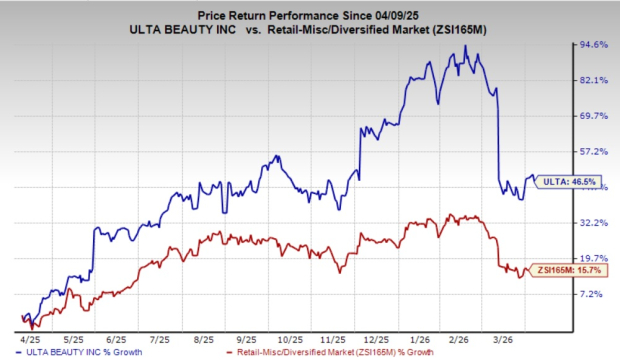

Overall, beauty demand still looks resilient, but its durability will likely depend on whether consumers continue to treat the category as worth prioritizing. Shares of Ulta Beauty have rallied 46.5% in the past year, outperforming the industry’s gain of 15.7%.

Stocks to Consider

Five Below, Inc. FIVE, which operates as a specialty value retailer, currently sports a Zacks Rank #1 (Strong Buy). FIVE delivered a trailing four-quarter earnings surprise of 63.4%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Five Below’s current fiscal-year sales and earnings suggests growth of 11.3% and 19.2%, respectively, from the year-ago figures.

Deckers Outdoor Corporation DECK, which designs, markets and distributes footwear, apparel and accessories, currently carries a Zacks Rank #2 (Buy) at present.

The Zacks Consensus Estimate for Deckers Outdoor’s current fiscal-year sales calls for growth of nearly 8.9%, and the estimates for earnings suggest an 8.5% increase from the year-ago figure. DECK delivered a trailing four-quarter earnings surprise of 36.9%, on average.

Tapestry, Inc. TPR, a provider of accessories and lifestyle brand products, currently carries a Zacks Rank of 2. TPR delivered a trailing four-quarter earnings surprise of 12.8%, on average.

The consensus estimate for Tapestry’s current fiscal-year sales and earnings suggests growth of 11.2% and 26.5%, respectively, from the year-ago figures.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Deckers Outdoor Corporation (DECK): Free Stock Analysis Report

Ulta Beauty Inc. (ULTA): Free Stock Analysis Report

Five Below, Inc. (FIVE): Free Stock Analysis Report

Tapestry, Inc. (TPR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).