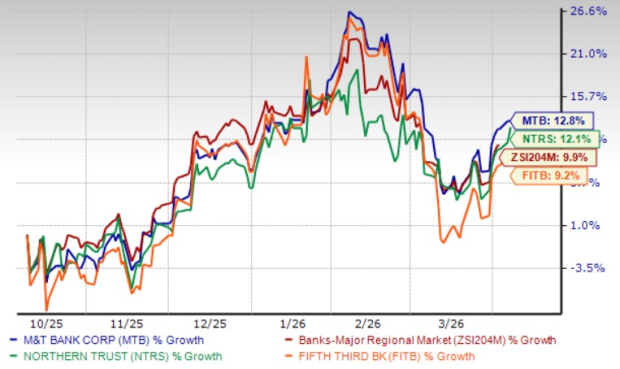

Shares of M&T Bank Corporation MTB have gained 12.8% in the past six months, outperforming the industry’s 9.9% growth. The stock has also fared better than its close peers, Northern Trust Corporation NTRS and Fifth Third Bancorp FITB. Shares of FITB and NTRS have gained 9.2% and 12.1%, respectively, over the same period.

Price Performance

Image Source: Zacks Investment Research

Given MTB’s outperformance relative to both industry and peers, investors may be wondering whether the stock remains a compelling addition to their portfolios. To assess this, let us take a closer look at its investment prospects.

Factors Driving MTB’s Performance

Robust Revenue Growth: M&T Bank has demonstrated strong organic growth, driven by a steady rise in revenues. Over the past seven years (2018-2025), its total revenues registered a compound annual growth rate (CAGR) of 7.8%. This expansion was largely supported by net interest income (NII), which expanded at a CAGR of 7.9%, while non-interest income increased at a CAGR of 3.9% during the same period.

Going forward, revenue growth is expected to be supported by higher NII, aided by loan growth and a favorable rate backdrop. Additionally, efforts to strengthen non-interest income through treasury management, capital markets, mortgage banking, and trust services are expected to support top-line growth. Management expects net interest income (tax-equivalent basis) to be in the range of $7.2–$7.35 billion, while non-interest income is projected to be between $2.67 and $2.77 billion in 2026.

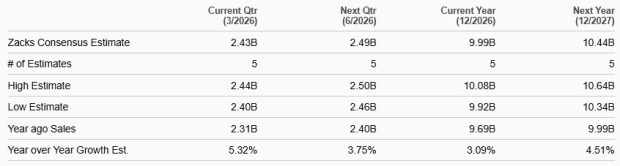

The Zacks Consensus Estimate for MTB’s 2026 and 2027 revenues is pegged at $9.9 billion and $10.4 billion, which indicates year-over-year growth of 3.1% and 4.5%, respectively.

Revenue Estimates

Image Source: Zacks Investment Research

Strategic Acquisitions to Strengthen Balance Sheet: The company’s acquisition-led strategy has played a key role in strengthening its balance sheet and expanding its franchise. In 2022, M&T Bank acquired People’s United for $8.3 billion, one of its major deals, which significantly enhanced scale and market presence. The acquisition added $36 billion in loans and $53 billion in deposits, strengthening the overall balance sheet. Earlier acquisitions, including Wilmington Trust in 2011 and Hudson City Bancorp in 2015, also supported asset growth and expanded the branch network across the United States.

Going forward, these strategic acquisitions continue to support franchise diversification and geographic reach. Deposits have grown at a seven-year (2018-2025) CAGR of 9.2%, while loans increased at a six-year CAGR of 6.6% through 2025. Management expects average loan and lease balances in the range of $140–$142 billion and average total deposit balances of $165–$167 billion in 2026. Additionally, a well-diversified deposit base and improving trends in consumer, commercial and industrial (C&I) and residential mortgage lending are expected to support further loan growth in the upcoming period.

Digital and AI Initiatives to Enhance Customer and Credit Capabilities: MTB is advancing its digital transformation through AI-enabled partnerships aimed at improving customer data integration and credit risk management. In August 2025, M&T Bank partnered with Amperity to unify customer data across its operations. This enables a consolidated view of customer interactions, helping enhance personalization, strengthen customer insights, and deliver more targeted financial solutions across channels.

Earlier, MTB expanded its collaboration with nCino in May 2024, integrating its Continuous Credit Monitoring Solution powered by nIQ and Rich Data Co’s AI decisioning platform. This AI-driven solution enhances credit monitoring by streamlining early warning indicators, improving visibility into cash flow health, and identifying lower-risk lending opportunities. Collectively, these digital and AI initiatives are expected to enhance customer engagement and operational efficiency, thereby supporting long-term competitive positioning.

Strong Liquidity Supports Capital Distribution: The company maintains a solid liquidity position. As of Dec. 31, 2025, its total debt of $13.1 billion (comprising short-term and long-term borrowings) was well below its cash and due from banks and interest-bearing deposits at banks of $18.8 billion.

Given this strength, M&T Bank continues to support shareholder returns through share repurchases. In March 2026, the board approved a new $5 billion common share repurchase program, replacing the prior $4 billion authorization approved in January 2025.

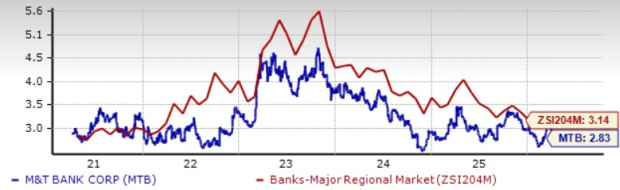

Apart from buybacks, the company has been consistently rewarding shareholders through dividends. In August 2025, M&T Bank raised its dividend by 11.1% to $1.50 per share. The company has increased its dividend four times over the past five years, while maintaining a payout ratio of 35%, reflecting a balanced approach between shareholder distributions and reinvestment in the business. Its dividend yield stands at 2.8%. Meanwhile, peer yields for Northern Trust and Fifth Third are 2.2% and 3.3%, respectively.

Dividend Yield

Image Source: Zacks Investment Research

What’s Hurting MTB’s Growth

Elevated Expense Base: The company continues to face pressure from an elevated expense base, with total expenses (GAAP, including intangible amortization) witnessing a CAGR of 7.6% over the last seven years (2018–2025). While management expects disciplined cost control to support positive operating leverage over time, expenses are likely to remain high as the company continues to invest in franchise expansion and operational capabilities. For 2026, MTB expects total GAAP expenses (including intangible amortization) in the range of $5.5–$5.6 billion, indicating sustained cost pressures in the near term.

Expense Trend

Image Source: Zacks Investment Research

Loan Concentration Risk: MTB remains significantly exposed to C&I and commercial real estate (CRE) loans, which together accounted for 62.9% of total loans and leases, net of unearned discount, as of Dec. 31, 2025. Given the evolving macroeconomic environment, this concentration exposes the bank to higher sensitivity in its credit portfolio. In the event of an economic slowdown, asset quality in these segments could come under pressure, which may adversely impact overall financial performance due to limited diversification.

Analyzing MTB’s Earnings Estimates & Valuation

The Zacks Consensus Estimate for M&T Bank’s 2026 earnings is pegged at $18.74 per share, which indicates year-over-year growth of 8.9%. The consensus mark for 2027 earnings is $20.86 per share, suggesting a rise of 11.3% year over year.

However, earnings estimates for both 2026 and 2027 have been revised downward over the past week.

Estimates Revision Trend

Image Source: Zacks Investment Research

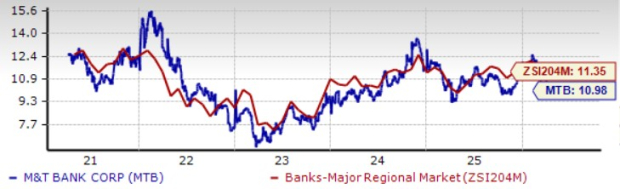

In terms of valuation, MTB stock appears inexpensive relative to the industry. The company is currently trading at a 12-month trailing price-to-earnings (P/E) ratio of 10.98X, which is lower than the industry’s 11.35X.

Price-to-Earnings F12 M

Image Source: Zacks Investment Research

Notably, Northern Trust holds a P/E ratio of 14.06X, while Fifth Third’s P/E ratio stands at 11.16X.

How to Approach the MTB Stock Now

Supported by steady organic growth and a strong regional franchise, M&T Bank is well-positioned to benefit from continued loan and deposit growth. Its improving lending mix and expanding digital and AI capabilities further support its long-term growth outlook.

However, rising expenses and high exposure to commercial lending remain near-term concerns. Recent downward earnings estimate revisions also signal some caution around profitability amid a challenging macroeconomic backdrop. Given this backdrop, investors should avoid rushing into M&T Bank stock at current levels. Instead, they should keep MTB stock on their radar and wait for a more attractive entry point. Existing shareholders may continue to hold the stock, as its strong franchise, stable capital returns and long-term growth initiatives are likely to support performance over the long-run.

The company currently carries a Zacks Rank #3 (Hold). You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Fifth Third Bancorp (FITB): Free Stock Analysis Report

M&T Bank Corporation (MTB): Free Stock Analysis Report

Northern Trust Corporation (NTRS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).