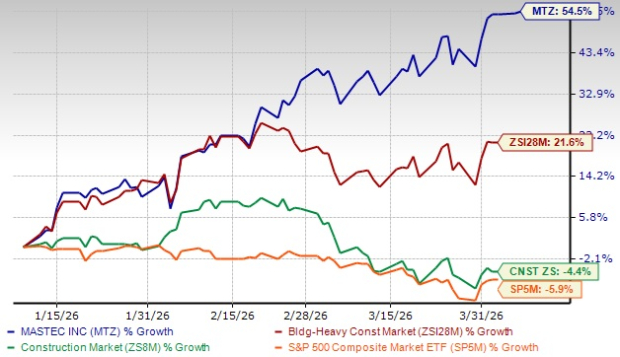

Shares of MasTec, Inc. MTZ have gained 54.5% in the past three months, significantly outperforming the Zacks Building Products - Heavy Construction industry’s 21.6% growth. The stock has further outperformed the broader Construction sector and the S&P 500, which have declined 4.4% and 5.9%, respectively, in the same period.

This Florida-based infrastructure construction company is seeing strong growth backed by rising investments across energy, communications and clean energy markets. Demand remains solid for grid upgrades, data centers, renewable projects and pipeline work. Expanding data center activity and telecom connectivity needs are driving higher project wins. A strong backlog and better project visibility support revenue growth ahead. Recent acquisitions are adding strength to construction management and water infrastructure capabilities, supporting long-term expansion.

MTZ Stock Outperforms Industry & Market

Image Source: Zacks Investment Research

However, the company faces some near-term challenges. Margin improvement remains uneven due to business mix and ongoing investments in new growth areas. Start-up costs related to new programs and scaling efforts are putting pressure on profitability. Project timing issues, including permitting delays, are affecting execution. Lower-margin construction management work in data center projects is also weighing on overall margins.

Let us take a closer look at the factors shaping MasTec stock’s prospects.

Backlog Expansion Enhances Visibility for MTZ

MasTec’s growing order book continues to strengthen revenue visibility. As of Dec. 31, 2025, the company reported an 18-month backlog of about $18.96 billion, up 33% year over year and 13% sequentially. The increase was broad-based across all four operating segments, with the strongest gains coming from the Pipeline Infrastructure and Clean Energy and Infrastructure businesses. Pipeline backlog expanded as energy infrastructure projects moved forward, while the clean energy segment benefited from higher renewable and infrastructure awards.

Furthermore, project visibility remains strong with additional opportunities tied to grid upgrades, renewable installations and digital infrastructure. With demand improving across key end markets, the expanding backlog provides a solid base for revenue growth in the coming periods.

Pipeline Recovery Drives Growth Momentum for MTZ

MasTec is seeing a strong recovery in its Pipeline Infrastructure business as project activity improves. The segment recorded a sharp ramp-up in volumes through 2025, supported by better execution and a favorable project mix. Margins also improved sequentially, reflecting stronger operating performance.

The company expects further growth supported by rising customer demand and increasing visibility around future project awards. MasTec also indicated that the business is moving toward historical peak levels over the next few years, supported by a strong opportunity pipeline.

Data Center Investments Expand MTZ’s Opportunity Base

Rising demand for digital infrastructure is creating new opportunities across data center projects. The company secured nearly $1 billion of data center-related work during the fourth quarter of 2025, marking a key step in expanding its presence in digital infrastructure.

These projects involve a mix of construction management and infrastructure services, allowing the company to leverage capabilities across multiple segments. Growing investments in artificial intelligence and cloud infrastructure are expected to drive further opportunities in this space.

Strategic Acquisitions Strengthen Long-Term Positioning

Recent acquisitions are expanding capabilities and market reach. The company acquired NV2A in the fourth quarter of 2025, enhancing construction management expertise, especially in complex infrastructure projects. It also acquired McKee Utility Contractors in early 2026, adding exposure to the growing water infrastructure market.

These acquisitions support the company’s strategy to scale operations and expand into structurally growing end markets. Strong cash flow generation also provides flexibility for additional growth investments.

Earnings Estimate Trend of MTZ

MasTec’s 2026 earnings estimate has increased to $8.61 per share from $8.54 over the past seven days. The estimated figure for 2026 earnings implies growth of 31.5% year over year on projected revenue growth of 19.2%.

Image Source: Zacks Investment Research

Hurdles to MTZ’s Growth Trend

Variability in capital spending and project timing remains a key concern for MasTec. Certain operations have seen uneven performance due to changes in customer investment cycles and delays in project execution. In the fourth quarter of 2025, the Power Delivery segment reported EBITDA margins of 8.2%, down 30 basis points from 8.5% in the prior-year period, impacted by unfavorable project mix and lower-than-expected volumes on the Greenlink transmission project.

Project timing challenges, particularly related to permitting delays, continue to affect execution visibility. Slower approvals and delayed project starts can temporarily reduce activity levels and impact near-term performance. While long-term infrastructure demand remains strong, such delays may lead to uneven revenue realization across periods.

MTZ Trading at Premium

MTZ stock is currently trading at a premium compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 36.54, as shown in the chart below.

Image Source: Zacks Investment Research

MasTec’s Position in a Competitive Infrastructure Market

MasTec operates in highly competitive energy, power and infrastructure markets, where it competes with established industry players such as EMCOR Group, Inc. EME, Quanta Services, Inc. PWR and Primoris Services Corporation PRIM. Each of these companies holds strong capabilities in different areas of infrastructure construction and engineering services.

EMCOR leverages a broad mechanical and electrical services network, allowing it to maintain strong regional coverage across industrial, commercial and utility markets. This footprint helps generate steady work from maintenance contracts, facility upgrades and distributed energy projects. Quanta Services remains a leading player in the electric power space, supported by deep expertise in transmission and distribution infrastructure and long-standing relationships with utility customers, positioning it to secure major grid modernization and high-voltage transmission projects. Primoris Services continues to expand its presence across solar, gas infrastructure and civil construction, supported by flexible project execution and long-term master service agreements.

At the same time, industry demand continues to expand as renewable energy deployment accelerates and utilities increase investments in grid modernization and electrification. Within this environment, MasTec benefits from its ability to deliver multi-scope infrastructure services across power, energy and communications networks. This integrated capability allows the company to participate in complex infrastructure projects that require multiple service offerings, providing a competitive edge alongside larger peers.

How to Play MasTec Stock?

MasTec is supported by strong demand across energy, communications and digital infrastructure markets. A growing backlog and expanding data center opportunities provide visibility into future revenues. The company is also seeing favorable estimate revisions for 2026, indicating improving earnings prospects as infrastructure spending remains strong.

However, margin pressure, project timing variability and ongoing investments may create near-term volatility. The stock is also trading at a premium valuation compared with peers, which may limit upside in the near term. With a Zacks Rank #3 (Hold), the stock appears suitable for holding, while new investors may wait for a better entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR): Free Stock Analysis Report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

Primoris Services Corporation (PRIM): Free Stock Analysis Report

MasTec, Inc. (MTZ): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).