If you look at the headlines of financial publications today, you will see a picture which at any other point would have created a crisis of biblical proportions in the markets. Geopolitical tension in the Middle East is breaking records, oil (CLK26) quotes are pricing in the risks of blocking key transport arteries, and the U.S. Federal Reserve is keeping interest rates at high levels.

At the same time, American stock indexes demonstrate striking stability. Any correction is bought up with phenomenal speed, and the bears have repeatedly found themselves ground up by algorithms and capital professing the “Buy the Dip” strategy. But here is the caveat: it is important to understand the psychological factor, as the markets found themselves literally infected by growth. Investors feel infallible, and therefore, the bears right now can do absolutely nothing with the American market.

Join 200K+ Subscribers: Find out why the midday Barchart Brief newsletter is a must-read for thousands daily.

What lies behind this paradox? Why did markets forget to fall the way they did until 2008?

To answer this question, we must step beyond the frames of standard technical analysis and look at the fundamental evolution of the very nature of money and approaches to economic management. We have witnessed how monetarism found a “pill of immortality” for financial markets. But as with any powerful medicine, it comes with its own price.

The Paradox of Stability: From the Great Depression to the Pandemic

Historically, a recession was perceived as an economic catastrophe. This was an uncontrollable process of destruction, accompanied by cascading defaults, the physical stopping of enterprises, mass unemployment, and a severe liquidity deficit. The economy “cleansed itself” through pain, bankruptcies, and social upheavals. However, the last 15 years visually demonstrate that this mechanism is broken or, more precisely, forcibly disconnected.

The best stress test of the new system was the 2020 pandemic. Think about it. The world faced an unprecedented physical stopping of the economy in modern history. Supply chains were torn, factories stopped, and people were locked in their homes. By all laws of classic economics, this should have led to a collapse comparable to 1929. The S&P 500 Index ($SPX) did collapse, but the collapse was proportionally small compared to the scale of the real disaster. The market lost less than 50%, and the recovery took a matter of months, after which indexes rushed to new historical maximums. This was a harsh stress test, and it’s hard to imagine anything worse. Plus, the ease with which the markets coped with it definitively proves that deep drawdowns are likely a thing of the past.

The pandemic proved to investors that in the modern system, a “bottom” does not exist, because under any economic failure, regulators are ready to substitute a bottomless pool of liquidity.

Evolution of Money: How the Financial Sector Became the ‘Second Economy’

To understand how we arrived here, we need to remember old economic schools. Under the Gold Standard and even in the first decades after it, the quantity of money in the system was rigidly tied to the real economy. The classic equation of exchange stated that the money mass must correspond to the quantity of produced goods and services. If capital withdrew liquidity from the system (for example, due to a crisis of trust), then a literal drought of liquidity ensued. There was physically not enough money to service the trade turnover, which led to a deflationary spiral.

At the same time, the paradigm changed. The financial sector — markets of debt, derivatives, corporate bonds — expanded to such cyclopean scales that it turned into a separate, independent universe. This sector began to demand colossal volumes of liquidity simply for the maintenance of its own life activity, for refinancing old debts and issuing new ones.

The modern monetarist formula no longer ties money exclusively to the commodity economy. Today, the volume of liquidity must not only service the real economy but also continuously feed the “financial sponge.” If the regulator attempts to limit the money mass only by the needs of the real economy, ignoring trillion-dollar debt obligations, this sponge will momentarily suck out all money from the system, provoking a global margin call.

Simply put, if this giant debt sector is not watered with fresh money, it will aggressively dehydrate the real economy. It will simply pull liquidity out of real factories, salaries, and consumers’ pockets for the sake of repaying financial obligations. This is exactly why money is now always printed with a reserve, covering the needs of both goods and debts.

2008: The Crossing of the Rubicon and the Triumph of Monetarism

The ideas of monetarism captured the minds of economists since the crises of the 1970s, but 2008 became the testing ground where these theories were applied in practice at the terminal stage.

When the mortgage crisis threatened to bring down the entire world banking system, the U.S. Federal Reserve made a historical decision to flood the fire with freshly printed money. Quantitative easing (QE) became that very “pill.” The Fed took upon itself the role of the creditor of last resort on an unseen scale, buying out toxic assets and saving system-forming institutions.

From this moment, the world changed forever. Regulators proved that a chain reaction of bankruptcies and a hard landing of the economy can be prevented. The method of monetarism worked. 2008 marked the beginning of the full-fledged practical realization of monetarism, and it must be understood: No one will likely ever depart from this method again.

For markets, this became a signal that any serious turmoil from now on is treated by one universal recipe — an injection of liquidity. This is exactly why modern bears are doomed to failure. They try to play by the rules of the 20th century in a world where central banks are ready to endlessly rewrite the rules of the game to prevent a systemic crash. A recession from a fatal diagnosis turned into a temporary ailment, which is treated by turning on the printing press. But here is the caveat: this “pill of immortality” has its own side effect, which forever changed the goal-setting of central banks.

Inflation as a Global Insurance Premium

Having rid the world of the destructive consequences of classic recessions, monetarists faced an inevitable mathematical law: Someone must pay for the saving of the system. And inflation became the means of payment.

Today, the global economy has tacitly concluded a new social contract, choosing permanent inflation as an insurance premium against the risk of repeating the Great Depression. From the point of view of the system’s survivability, this is an incredibly profitable deal. Thanks to the intervention of central banks, we no longer see cascading defaults, 25% unemployment, and lines for free soup. The motor of the economy does not stall, consumption does not stop, and the social structure of society avoids radical upheavals and revolutions. This is a small, absolutely justified price. Inflation is a price worth paying so that there are no starving people, no hard economic landings tearing countries to pieces. We literally bought our way out of these catastrophes.

A small price for stability? On a macroeconomic scale, absolutely. At the same time, this “pill” has its own long-term side effects.

Firstly, an economy that never passes through a harsh phase of cleansing inevitably accumulates an army of “zombie companies” — businesses existing exclusively on borrowed time and credit. This hinders technological progress and weighs on labor productivity. Secondly, a powerful Cantillon effect arises: financial institutions and asset owners receive first access to the printed liquidity, while the money reaches the real economy in an already depreciated form. As a result, inflation turns into a hidden tax on labor in favor of capital, fundamentally widening the abyss between the rich and the poor. The volatility of markets is suppressed at the expense of the volatility of the currency itself.

The Fed’s Sisyphean Task and the Era of ‘Eternal Struggle’

In this new paradigm, the role of the regulator itself changes fundamentally. Today, the Federal Reserve is reminiscent of an operator of a giant thermostat who is deprived of the opportunity to simply maintain a comfortable temperature.

Now it has only two operating modes: either turn the heating to full power (flooding the crisis with liquidity) so the economy doesn’t freeze in a recession, or open all windows wide open (raising rates and shrinking the balance) so the system doesn’t suffocate from inflationary smoke. Waiting for some neutral policy now is senseless. The Fed essentially has only two options left. The logic of the system has driven it into a tight corner: it must save the economy during shocks and is forced to fight inflation in the intervals between.

We have entered an epoch of permanent maneuvering. As soon as the economy feels normal, the Fed throws all its forces into the fight against inflation. But the moment a real threat appears on the horizon (a “black swan,” a pandemic, a geopolitical shock, or a liquidity crash in the banking sector), the regulator immediately unpacks its monetarist instruments and begins to save the markets. And when the smoke dissipates, the cycle launches itself anew — the Fed is again forced to fight inflation, birthed by its own rescue efforts.

This “backwards-forwards” movement means that inflation has turned from a temporary phenomenon, caused by a deficit of goods or logistical shocks, into a chronic, systemic disease.

In my view, inflationary pressure is now forever woven into the very fabric of the modern financial system. The question of inflation now becomes a question of eternal struggle, to which the market simply needs to get accustomed.

The institutional Fuse: Why We Do Not See Hyperinflation

Against the backdrop of this eternal struggle and colossal infusions of liquidity, a logical question arises for many. Some shout: “Since the printing press works with such force, it is logical to expect hyperinflation!” Why hasn’t it arrived, as it did in the 1970s? The answer lies in that same year, 2008, and in the fuse that was brilliantly written into the banking regulation system — the Basel III agreement.

After the 2008 crisis, banking norms were significantly tightened. Regulators perfectly understood that if they flooded the system with liquidity, they needed to tie the banks’ hands so that this money wouldn’t splash out into the streets as an uncontrollable stream of credit. A strict valuation of assets adjusted for risk was introduced. For example, oil is accounted for in bank capital with a 50% discount. Mortgages are also heavily discounted, and borrower quality requirements grew drastically.

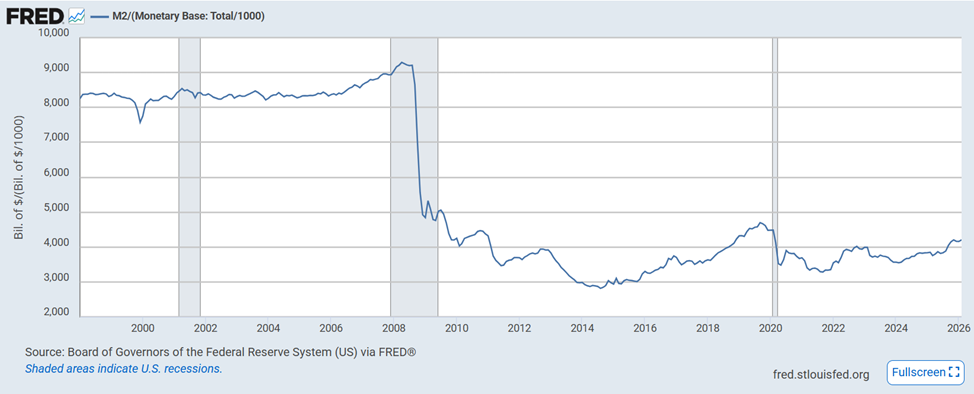

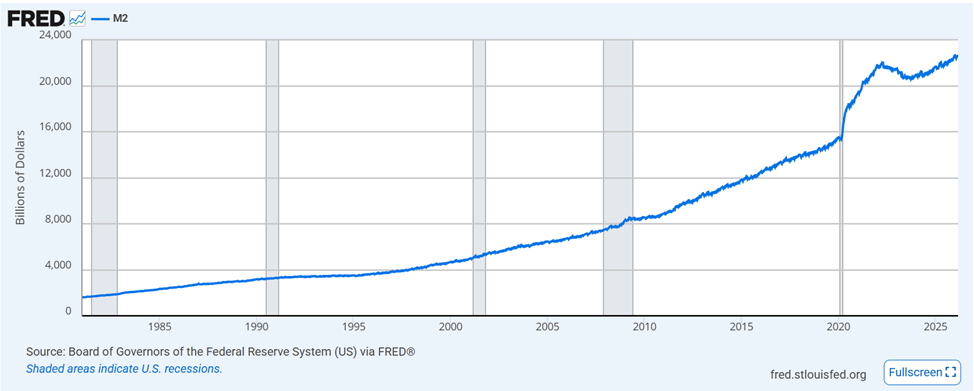

This system acts as a powerful brake, preventing inflation from spiraling out of control. Ordinarily, consumer credits and super-fast turnover of money would have provoked an explosive growth of inflation. But Basel III prevents this. This is exactly why we see an interesting phenomenon: the monetary base (the Fed’s balance) can grow at huge paces, but the M2 aggregate (the broad money mass, money in the real economy) crawls upward extremely slowly. This structure absorbs liquidity, saving markets, but limits the multiplier effect.

The Effect of the Compressed Spring: The Inertia of M2 and the Trap for the Regulator

However, this protective mechanism has a reverse side that few think about. Basel III initially brakes inflation, preventing the multiplier from sharply soaring, but it does not destroy the printed liquidity — it conserves it. Imagine the broad money mass M2 as a giant compressed spring, a powerful shock absorber, or a recoil system of a heavy artillery gun.

The mechanism works like this: when the Fed takes a sharp “shot” of liquidity during a crisis, the monetary base (M0) soars momentarily. The aggregate M2 cannot soar synchronously because banking norms rigidly hold back this impulse. But here is the caveat: the colossal energy of this infusion does not disappear! It turns into accumulated potential. M2 begins to crawl upward with a delay, slowly but inevitably seeping into the system. The base expanded, and therefore the mass inevitably strives upward, pulling the entire economy up with it.

This creates a paradoxical situation, turning the fight against inflation into a real trap. When the Fed decides the crisis has passed and begins to fight rising prices, it faces colossal inertia. The Fed is already slamming on the brakes, raising rates, but M2 — like the heaviest freight train — continues to crawl upward on the energy of past infusions. And it will crawl for a very long time.

This is exactly why the regulator is forced to wage this eternal struggle with inflation, and why it’s failing so badly. It is impossible to defeat inflation fully and quickly because beneath it lies the massive potential of M2, which continues to feed the system with old money.

The Myth of 2%: Why the Ideal Is Unreachable

Here we approach the main paradox of the current Fed policy: the famous inflation target of 2%. Markets continue frantically to follow PCE and CPI data, hoping for a return to this coveted number. But in current monetarist realities, achieving 2% is an illusion.

The 2% target in the modern world is not a destination. It is a psychological anchor, the “ideal gas” of macroeconomics, necessary exclusively for managing the inflationary expectations of business and the population. If the Fed tomorrow admits that 2% is unreachable and moves the target to 4%, the market will immediately price in 6%. This is simply a philosophical ideal to which the regulator will strive, but we shouldn’t deceive ourselves into believing we will ever conclusively achieve it.

The truth is that every new crisis, once flooded with liquidity, creates a step-change in prices. The base expands, and returning to old price levels is impossible. Plus, given the cyclopean size of the U.S. national debt (and other developed countries), real inflation at 2% and a harsh monetarist policy would be a death sentence for the budget. The system vitally needs inflation at the 3%-4% level to imperceptibly wash away the value of this colossal debt.

Therefore, the Fed is doomed to run in place. The regulator will endlessly strive for 2% in the intervals between crises, but achieving this ideal on a stable basis will be a huge problem because, around the next corner, a new crisis is always waiting, requiring a fresh injection of liquidity.

What Does This Mean for the Investor?

Understanding these mechanics answers the question of why American indexes refuse to fall even against the backdrop of the heaviest geopolitical crises and high rates. Investors, algorithms, and large funds have likely realized that the bear market in its classic understanding is dead. Money has ceased to be a means of unconditionally preserving value. For capital not to burn in the furnace of permanent inflation (by which the system pays for its survival), it must constantly be put to work.

The constant growth of the S&P 500, historical maximums of gold, and the phenomenon of cryptocurrencies are not simply the consequence of corporate profits or faith in technologies. In many ways, this is a mirror reflection of the devaluation of fiat money itself in relation to real, hard assets. When the market knows that during any truly deep fall the regulator will step in with a limitless checkbook, the only logical and mathematically justified strategy remains to buy any drawdown.

A recession has ceased to be a death sentence. Now it is simply a reboot of the system with a discount on assets, before the printing press is plugged back in. Wall Street has already grown accustomed to this new normal. The rules of the game have fundamentally changed, and to survive in this market, investors must accept this fact, completely throwing away the old patterns and fears of the 20th century.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

The Death of the Bear Market: Why Classic Recessions Are a Thing of the Past and Inflation Is the New Norm Stocks Slip Before the Open as Oil Rebounds Amid Fragile U.S.-Iran Ceasefire, PCE Inflation and GDP Data in Focus 1 Trade to Make Now as U.S., Iran Agree to 2-Week Ceasefire S&P Futures Soar as Oil Prices Plummet on U.S.-Iran Ceasefire, FOMC Minutes on Tap