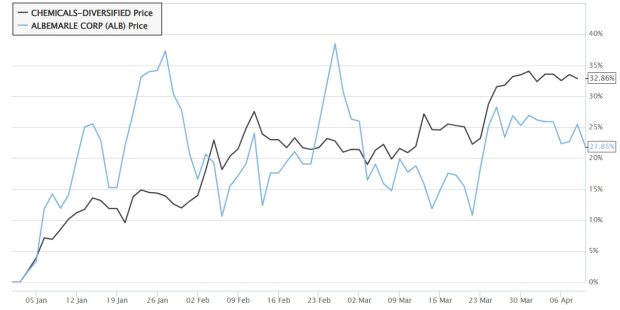

Albemarle Corporation’s ALB shares have gained roughly 21.9% year to date. The upside has been driven by the company’s solid earnings performance, supported by strong growth in the Energy Storage segment, cost-reduction initiatives and a rebound in lithium prices amid strengthening demand and tighter supply conditions. ALB has underperformed the Zacks Chemical - Diversified industry’s rise of around 32.9%.

ALB’s YTD Price Performance

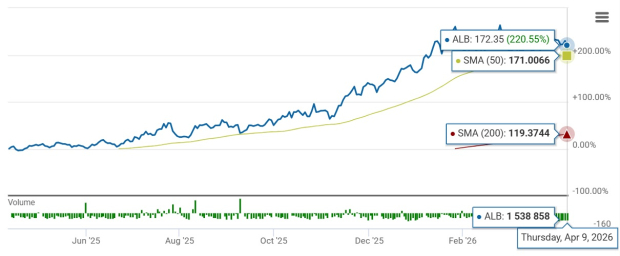

ALB stock broke above its 50-day simple moving average (SMA) on March 24, 2026. It is also currently trading above its 200-day SMA, suggesting a long-term uptrend.

Albemarle Trades Above 50-Day SMA

Let’s take a look at ALB’s fundamentals to analyze the stock better.

Lithium Project Expansion & Productivity Aid Albemarle

Albemarle is well-placed to gain from long-term growth in the battery-grade lithium market. The market for lithium batteries and energy storage remains strong, especially for EVs, offering significant opportunities for the company to develop innovative products and expand capacity. Lithium demand is expected to grow on the back of significant global EV penetration. ALB expects lithium demand to witness a compound annual growth rate (CAGR) of 10-20% from 2025 to 2030. Stationary storage is expected to be a significant driver for lithium demand along with EVs. Lithium demand increased more than 30% year over year, and the company expects demand to grow roughly 15-40% this year.

The company is strategically executing its projects aimed at boosting its global lithium conversion capacity. It remains focused on investing in high-return projects to drive productivity. Healthy customer demand, capacity expansion and plant productivity improvements are supporting its volumes. ALB saw higher sales volumes in its Energy Storage unit in the fourth quarter of 2025 on strong production from its integrated conversion facilities. The Salar yield improvement project in Chile has achieved a 50% operating rate, and the ramp-up continues to deliver encouraging outcomes. The ramp-up at the Meishan lithium conversion facility in China is also progressing ahead of schedule.

Albemarle is taking aggressive cost-saving and productivity actions in the wake of tumbling lithium prices. The company delivered roughly $450 million in cost and productivity improvements for full-year 2025, having surpassed its initial target of $300-$400 million. It expects additional cost and productivity improvements of $100-$150 million in 2026. ALB is taking actions to maintain its competitive position, including the initiation of a comprehensive review of cost and operating structure, optimization of the conversion network and reduction of capital expenditure. Its capital expenditures of $590 million for 2025 decreased 65% year over year.

ALB, in February 2026, announced that it will idle Train 1, the remaining operating train at its Kemerton lithium hydroxide processing plant in Western Australia, and place it into care and maintenance effective immediately. This move follows earlier actions in 2024 to idle Train 2 for care and maintenance and stop expansion plans for Trains 3 and 4. The Kemerton facility processes spodumene from the Greenbushes mine, one of the world’s best deposits. The move is a result of the ongoing efforts over the past two and a half years to reduce operating costs. The company expects higher flexibility and optionality to benefit adjusted EBITDA starting in the second quarter of 2026.

Higher lithium prices, driven by strong demand from EVs and energy storage systems, along with supply disruptions due to recent supply reductions in China, should also aid ALB’s performance. Lithium prices have rebounded lately from trough levels, supported by tightening supply and strong demand in China and globally.

Robust Financial Health Supports ALB’s Capital Allocation

Albemarle remains committed to driving shareholder value by leveraging healthy cash flows and strong liquidity. At the end of 2025, ALB had liquidity of around $3.2 billion, including cash and cash equivalents of around $1.6 billion. Its operating cash flow was around $1.3 billion in 2025, up roughly 86% from the prior-year period. ALB expects generated free cash flow of $692 million for full-year 2025, driven by strong cash conversion, lower capital spending and productivity measures.

The company remains focused on maintaining its dividend payout. It has raised its quarterly dividend for the 30th straight year. ALB offers a dividend yield of 0.9% at the current stock price. Its peers, Sociedad Quimica y Minera de Chile S.A. SQM and Rio Tinto Group RIO have a dividend yield of 0.2% and 5.2%, respectively.

Volume & Demand Headwinds Ail ALB

While the Energy Storage unit is expected to benefit from higher lithium prices in 2026, it faces volume pressure, which may affect the segment’s sales. The company expects energy storage sales volumes to be roughly flat in 2026, following inventory drawdowns in 2025. The normalization of inventories is likely to impact volumes in 2026.

The Specialties unit also faces challenges from softness in building and construction. High interest rates continue to curb spending in residential construction. Weaker demand in oil and gas applications is also expected to weigh on the segment’s sales and margins.

ALB’s Estimates Reflect Positive Sentiment

The Zacks Consensus Estimate for 2026 for ALB has been revised upward over the past 60 days. The consensus estimate for 2027 has been going up over the same time frame.

The Zacks Consensus Estimate for 2026 earnings is currently pegged at $8.15, suggesting a year-over-year rise of 1,131.7%. Earnings are expected to increase roughly 17.7% in 2027.

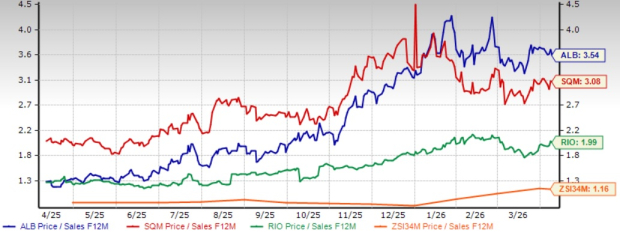

ALB: An Expensive Stock

ALB is currently trading at a forward price-to-sales ratio of 3.54, well above the industry. It is trading at a premium to Sociedad Quimica and Rio Tinto. Albemarle and Sociedad Quimica currently have a Value Score of D, while Rio Tinto has a Value Score of A.

ALB’s P/S F12M Vs. Industry, SQM and RIO

Conclusion: Hold Onto ALB Stock for Now

Albemarle is benefiting from its initiatives to expand global lithium conversion capacity and enhance productivity. The company is well-positioned to capitalize on the substantial growth opportunity in the battery-grade lithium market, supported by the global transition toward EVs. Higher lithium prices amid robust demand and tight supply conditions also provide a tailwind.

Rising earnings estimates and a strong growth outlook are other positives. However, volume pressures in Energy Storage and demand headwinds in Specialties could dampen its prospects. Its stretched valuation also might not offer an attractive entry point at this time. Considering these factors, holding onto this Zacks Rank #3 (Hold) stock will be prudent for investors who already own it.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Rio Tinto PLC (RIO): Free Stock Analysis Report

Albemarle Corporation (ALB): Free Stock Analysis Report

Sociedad Quimica y Minera S.A. (SQM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).