Amazon (AMZN) released its 2025 annual shareholder letter on April 9. Among other things in the letter, CEO Andy Jassy was unapologetic about Amazon's burgeoning capex, which is set to hit a record high of $200 billion this year. For context, the 2026 capex guidance is well ahead of last year’s $131 billion in capital expenditures and would mark the highest-ever annual capex by any company in history.

AMZN stock crashed following the fourth-quarter 2025 confessional. The drawdown wasn’t on account of the $0.03 that the company missed on the bottom line but rather the massive rise in 2026 capex guidance, which was more than $50 billion higher than what the Street was expecting.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com CEO Andy Jassy Is Unapologetic About AI Capex

Jassy didn’t just defend the rising capex — the bulk of which is going toward building artificial intelligence (AI) infrastructure — but was also quite upbeat about the technology. “When you identify disproportionate inflections, bet big,” said the CEO. Terming AI as a “seminal shift,” he has “strong conviction” that AI is neither “over-hyped” or a “bubble" for Amazon, adding that “margins and ROIC [return on invested capital] will be appealing."

“We are willing to make large capex investments and endure short-term FCF [free cash flow] headwinds for the substantial medium to long-term FCF surplus,” said Jassy in an apparent bid to calm nerves over the expected negative free cash flow this year.

However, markets have been fatigued by such bullish AI comments from tech leaders. These comments are no longer cherished like they were a couple of years ago. Instead, the focus is on hard numbers, which the executive provided quite a bit of in the letter.

Jassy said that Amazon is not investing $200 billion on a “hunch” and that the company has commitments for a “substantial portion” of the capex, which will be monetized over the next two years.

Amazon Sees Strong Growth in AI Business

For the first time, Amazon provided absolute numbers for Amazon Web Services' (AWS) AI revenues, which Jassy said were running at an annualized pace of $15 billion in Q1 2026. The company also provided an update on its custom AI chip business, which Jassy said is “on fire" with an annual revenue run rate in excess of $20 billion and “growing triple digit percentages.” The CEO stressed that Amazon is currently monetizing its chips through Elastic Compute Cloud (EC2), and if its chip business was standalone, it could have sold chips worth $50 billion to AWS and third-party customers.

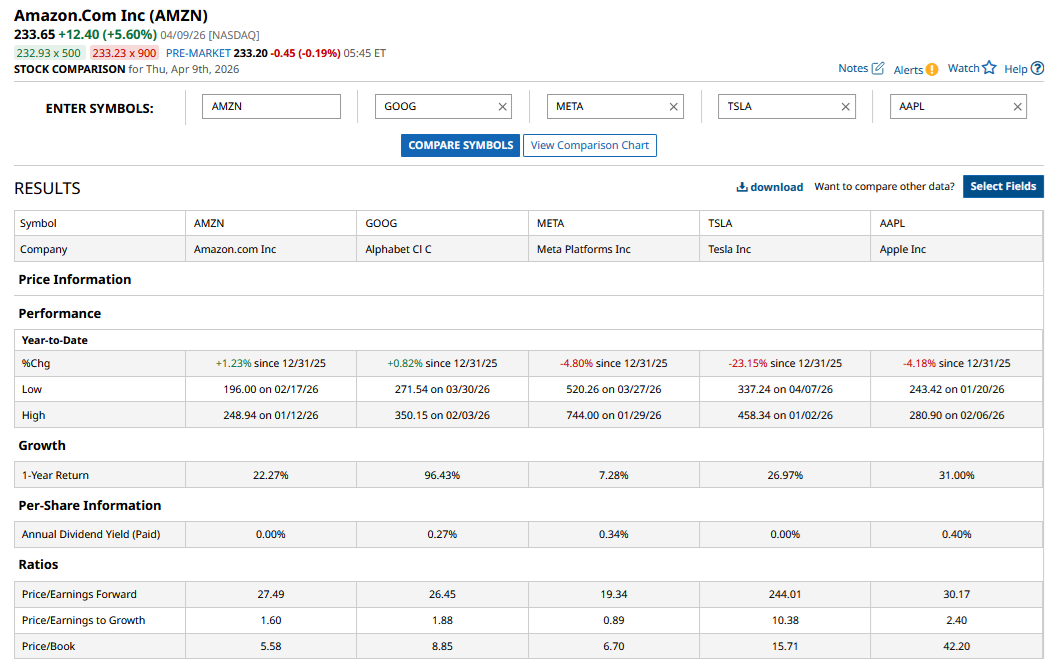

Incidentally, one of the reasons Alphabet (GOOGL) stock has outperformed Big Tech peers over the last year is due to the optimism over its chip business. With Amazon also announcing big plans for that segment — and with Jassy noting that two large AWS customers wanted to buy all of the Graviton instance capacity this year — the strong demand for these chips is evident.

www.barchart.com

www.barchart.com Should You Buy AMZN Stock?

I have been bullish on AMZN stock and have used the dip this year to add to my positions. Apart from driving AWS growth, AI should help make Amazon’s e-commerce platform an even better proposition by improving customer experience. Over 300 million people used Amazon’s Rufus shopping agent in 2025 and, with further enhancements, that number is set to rise further.

Prime is another key part of Amazon’s flywheel. Not only does it bring in subscription and ad revenue, but these customers tend to order more frequently on the e-commerce platform.

Amid sagging growth for its e-commerce business, Amazon has been focusing on grocery. In the shareholder letter, Jassy said that the grocery segment saw $150 billion in gross sales last year, making it the second-largest grocer in the United States.

The company continues to expand its target market, and Amazon Leo — which would be a competitor to Elon Musk’s Starlink — is set for a mid-2026 launch. Amazon is also expanding its Zoox autonomous ride-hailing service. Finally, building robots for third-party customers is something the company might explore in the future as well.

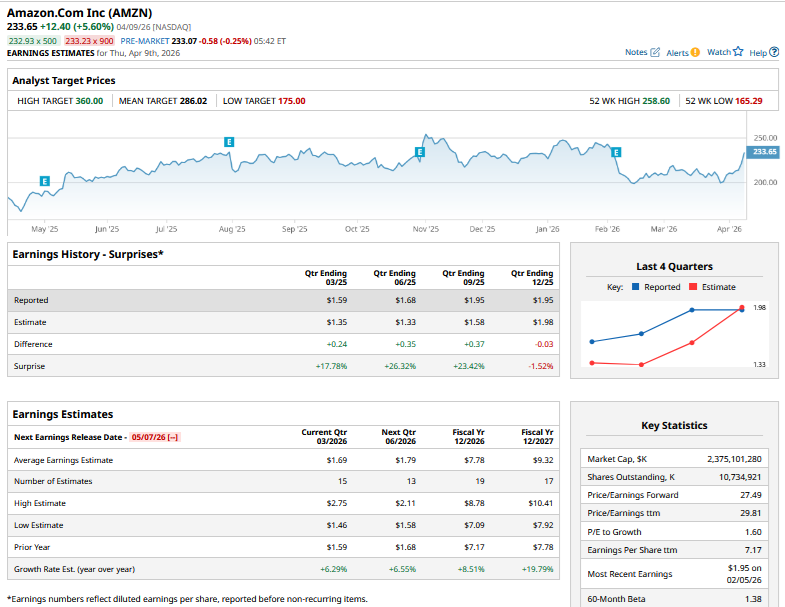

Overall, with a forward price-to-earnings (P/E) multiple of around 30 times, I find Amazon to be a value play and expect AMZN stock to deliver strong returns over the next few years as the company monetizes its AI investments.

On the date of publication, Mohit Oberoi had a position in: AMZN , GOOG . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

On Semiconductor Pops on Analyst Upgrade. Should You Buy ON Stock Here? A $21 Billion Reason to Buy CoreWeave Stock Now Oracle (ORCL) Stock May Be Priced at a Genuine Discount As Waymo Launches in Nashville, Should You Buy, Sell, or Hold GOOGL Stock?