Snap-on Incorporated SNA is likely to witness growth in its top and bottom lines when it reports first-quarter 2026 earnings on April 23, before the opening bell. The Zacks Consensus Estimate for revenues is pegged at $1.18 billion, which indicates a rise of 3.2% from the year-ago quarter’s reported figure.

The Zacks Consensus Estimate for earnings is pegged at $4.68 per share, which indicates growth of 3.8% from the year-ago quarter’s registered numbers. The consensus mark has remained unchanged over the past 30 days.

The company has a negative trailing four-quarter earnings surprise of 0.1%, on average. It delivered an earnings surprise of 1.7% in the last reported quarter.

Factors Likely to Impact SNA’s Q1 Results

SNA's first-quarter fiscal 2026 results are expected to reflect stable demand across its core automotive repair markets, supported by the ongoing aging of the global vehicle parc and rising vehicle complexity. The company has consistently emphasized that aging vehicles require more frequent maintenance and specialized repairs, driving sustained demand for professional tools, diagnostics, and repair solutions. Continued strength in technician activity and repair shop utilization is expected to have supported sales momentum across the Tools and Repair Systems & Information (RS&I) segments.

Strength in the Commercial & Industrial (C&I) segment is also expected to have aided overall performance, particularly driven by demand from critical industries, such as aviation, heavy-duty equipment and technical education. Recent performance indicated solid growth supported by new product launches, including advanced power tools and specialty torque solutions, which have been key contributors to volume expansion. Ongoing investments in custom kitting capabilities and precision tools are likely to have provided additional traction in the first quarter.

The company’s focus on innovation and continuous product development is anticipated to have remained a meaningful growth driver. Snap-on has been actively launching new tools and diagnostic solutions tailored to evolving technician needs, particularly as vehicles become increasingly sophisticated. Expansion of proprietary software, data platforms and diagnostic capabilities is likely to have enhanced customer productivity and strengthened recurring demand, supporting growth in the RS&I business.

Margin performance in the to-be-reported quarter is likely to reflect the combined impact of higher material costs, tariff-related pressures, and continued investments in brand building, software development and training initiatives. While operational efficiency initiatives, including Rapid Continuous Improvement (RCI) programs, have historically offset some cost pressures, elevated expenses tied to innovation and market development could weigh modestly on near-term profitability.

However, macroeconomic uncertainty, fluctuating trade policies and cautious spending behavior among technicians remain key risks. Management had previously noted that uncertainty around tariffs and broader economic conditions can influence purchasing patterns, particularly for higher-ticket items such as tool storage products.

SNA’s diversified product portfolio, strong brand positioning and ongoing investments in technology and product innovation must have mitigated these challenges and supported overall first-quarter performance.

What Does the Zacks Model Predict for SNA Stock?

Our proven model does not conclusively predict an earnings beat for Snap-on this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that is not the case here.

Snap-on has an Earnings ESP of 0.00% and a Zacks Rank of 4 at present. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Valuation Picture

From a valuation perspective, Snap-on appears attractive, trading at a discount to its historical averages and broadly in line with industry benchmarks. With a forward 12-month price-to-earnings ratio of 18.21X, which is below the five-year high of 19.42X and nears the Tools - Handheld industry’s average of 19.27X, the stock offers compelling value for investors seeking exposure to the sector.

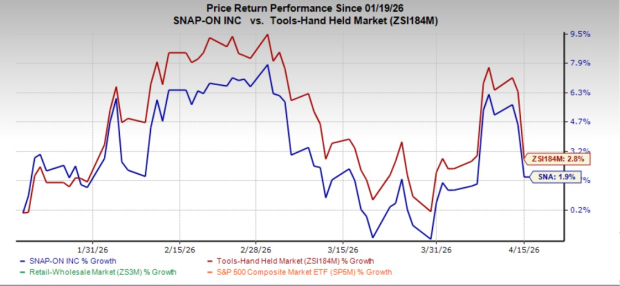

SNA Stock Price Performance

Image Source: Zacks Investment Research

The recent market movements show that SNA shares have gained 1.9% in the past three months compared with the industry's 2.8% growth.

Image Source: Zacks Investment Research

Stocks With the Favorable Combination

Here are some companies, which, according to our model, have the right combination of elements to post an earnings beat:

Cimpress plc CMPR currently has an Earnings ESP of +6.67% and a Zacks Rank of 1. CMPR is likely to register top and bottom-line growth when it reports third-quarter fiscal 2026 results. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for its quarterly revenues is pegged at $861.8 billion, indicating a 9.2% increase from the figure reported in the year-ago quarter. The consensus estimate for CMPR’s fiscal third-quarter earnings is pegged at 15 cents per share, implying a 145.5% surge from the year-ago quarter’s reported actuals. The consensus mark has moved south 11.8% in the past 30 days.

Marriott International, Inc. MAR currently has an Earnings ESP of +4.03% and a Zacks Rank of 3. MAR is likely to register top and bottom-line growth when it reports first-quarter 2026 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $6.58 billion, indicating 5% growth from the figure reported in the year-ago quarter.

The consensus estimate for MAR’s first-quarter earnings is pegged at $2.59 per share, implying 11.6% growth from the year-earlier quarter’s level. The consensus mark has moved up 0.8% in the past seven days.

Hilton Worldwide, Inc. HLT currently has an Earnings ESP of +4.88% and a Zacks Rank of 3.

For the to-be-reported quarter, Hilton Worldwide’s earnings are expected to increase 13.4%. Hilton Worldwide reported better-than-expected earnings in each of the trailing four quarters, the average surprise being 5.7%.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Marriott International, Inc. (MAR): Free Stock Analysis Report

Snap-On Incorporated (SNA): Free Stock Analysis Report

Hilton Worldwide Holdings Inc. (HLT): Free Stock Analysis Report

Cimpress plc (CMPR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).