Software stocks have had a rough start to 2026. By late February, the iShares Expanded Tech-Software Sector ETF (IGV) was down about 27.2% for the year, while many application software names had fallen 30% to 55% as investors started questioning how much growth these companies can still deliver in a market being reshaped by AI.

The S&P 500 Software Index was also down 20% year-to-date (YTD) as of early April. If AI agents can do work that once required expensive software platforms, what happens to the old SaaS model? That fear has become so widespread that some have even started calling it the “SaaS-pocalypse.”

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

That helps explain Piper Sandler’s recent move on Salesforce. The firm cut its price target on Salesforce (CRM) from $250 to $215, while still keeping an “Overweight” rating. Even so, the lower target shows a clear drop in confidence. Piper had earlier called Microsoft (MSFT) its top AI pick while staying cautious on the rest of the software, so this is not just about Salesforce. It reflects a broader reset happening across Wall Street.

So is software really in trouble, or is the market just getting too pessimistic about companies that are still building tools businesses will keep using for years? Let’s find out.

Salesforce Under the Microscope

Salesforce mainly sells business software on a subscription basis. Its tools help companies manage sales, customer service, marketing, data, and analytics, and it serves both private companies and government clients around the world.

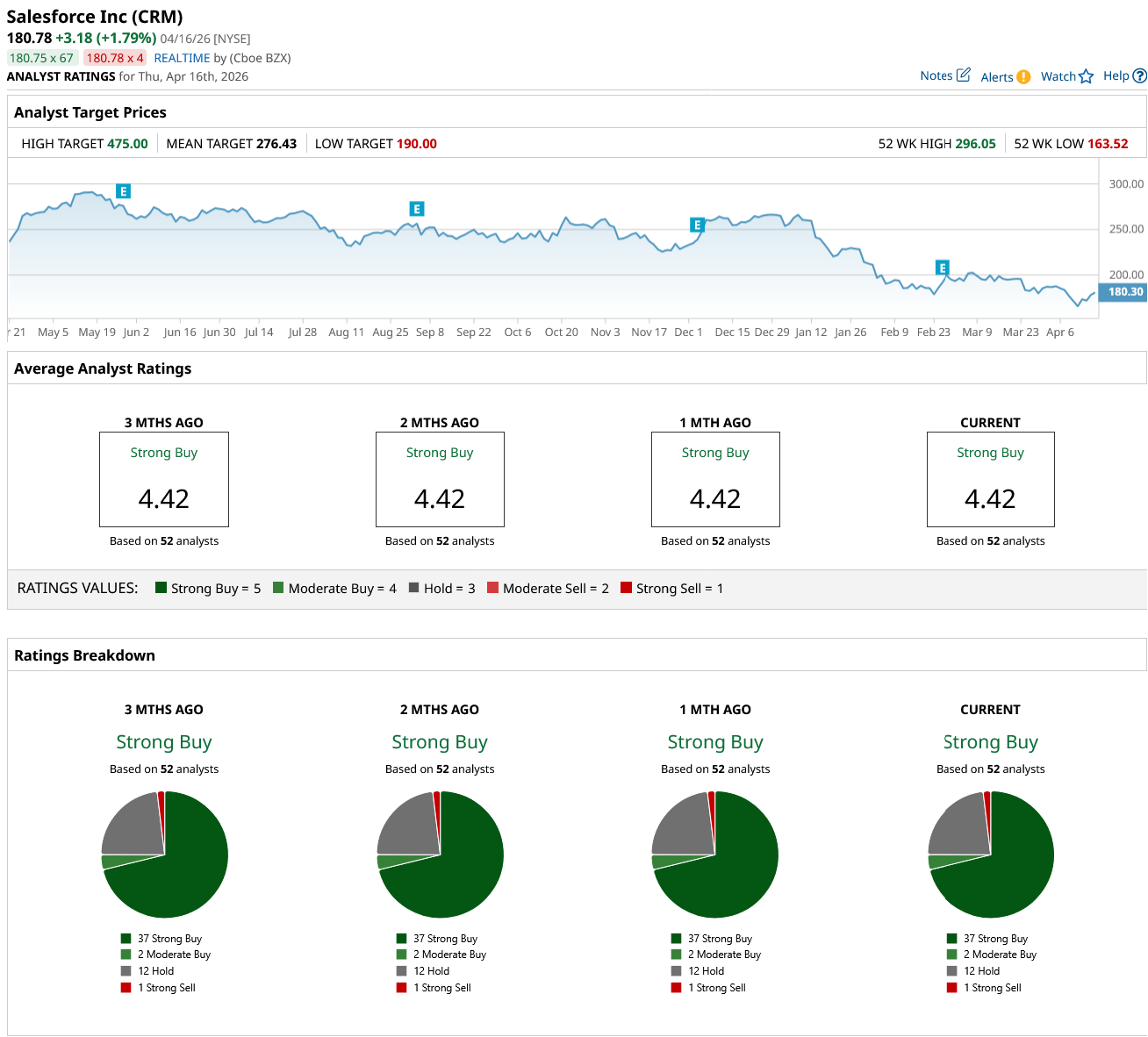

CRM stock has been under heavy pressure. Salesforce shares are down about 28% over the past 52 weeks and about 32% so far this year.

www.barchart.com

www.barchart.com That selloff has also made the stock look cheaper. Salesforce now trades at a forward P/E of 17.81x, compared with about 23.04x for the broader software sector. It also pays a dividend, with an annual yield of about 0.95% and a low forward payout ratio of 16.90%. The company has raised its dividend for two straight years, pays it quarterly, and its latest dividend was $0.44 per share in April 2026.

Its latest results help explain why it can afford that. Fourth-quarter revenue came in at $11.2 billion, up 12% from a year ago, or 10% in constant currency. That included a $399 million contribution from Informatica. Subscription and support revenue reached $10.7 billion, up 13%, or 11% in constant currency, including $388 million from Informatica. For the full 2026 fiscal year, revenue rose to $41.5 billion, up 10%, or 9% in constant currency. Remaining performance obligation grew to $72.4 billion, up 14%, while current RPO rose to $35.1 billion, up 16%, or 13% in constant currency.

What Still Powers the Salesforce Story

In healthcare, Salesforce is already being used in a very practical way. The Veterans Health Administration rolled out a Salesforce-based system across more than 150 VA medical and outpatient centers to help manage incidents faster and improve care for veterans.

Since the VA serves between 16 million and 18 million veterans, the goal here is scale. The system connects medical teams, caregivers, service providers, and VA staff in one place so they can coordinate better, share best practices, save time, and cut costs without hurting care.

The same idea shows up in sports and media. Formula 1 expanded its partnership with Salesforce by launching a new fan tool for its 827 million fans worldwide. It will first appear on F1.com and help answer questions about the new 2026 rules using trusted F1 information while also tracking what fans are asking about most. With 43% of F1 fans under 35, this gives the sport a simple way to reach younger audiences and keep them engaged.

Salesforce is also gaining ground in government. The U.S. Army awarded the company a $5.6 billion, 10-year IDIQ contract through Computable Insights, its national security unit. Through Missionforce National Security, Salesforce will provide the tools and cloud setup needed to help the Department of Defense make faster decisions, simplify procurement, lower costs, and improve readiness across military staff, civilian workers, partners, and dependents.

Wall Street’s Reset and What Comes Next for CRM Stock

For the quarter ending in April 2026, Wall Street expects Salesforce to earn $2.30 a share, up from $1.94 a year ago. For the July quarter, the estimate is $2.36, up from $2.27 last year. Looking further out, analysts expect full-year earnings of $9.71 for the fiscal year ending January 2027, which is basically flat from $9.70 the year before, before rising to $10.92 in 2028.

Analysts also still lean clearly bullish on CRM stock. On Jan. 26, Evercore ISI analyst Kirk Materne kept a “Buy” rating and set a $340 price target, pointing to confidence in Salesforce’s business momentum and broader product lineup.

A day later, Citizens analyst Patrick Walravens kept a “Market Outperform” rating and set a $405 target, saying strong execution in Agentforce was a key reason for his optimism. So yes, Piper Sandler’s cut added to the more cautious mood around software, but it has not changed the bigger Wall Street view.

The 52 analysts tracked by Barchart still rate Salesforce a consensus “Strong Buy,” and the average price target is $276.43, which implies about 53% upside from the current price.

www.barchart.com

www.barchart.com Conclusion

To be blunt, no, the software apocalypse does not look real, at least not in Salesforce’s case. Piper Sandler’s cut to $215 matters because it reflects a harsher market mood, but the company’s fundamentals, contract backlog, cash flow, and real-world AI deployments still point to a business that is being repriced, not broken. The more likely path for the shares is continued volatility in the near term as Wall Street digests slower growth and resets valuation multiples, but if Salesforce keeps converting AI adoption into revenue and holds its margin discipline, CRM stock still looks more likely to grind higher over time than keep collapsing from here.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Is Bloom Energy Stock a Buy, Sell, or Hold at New All-Time Highs? Does the QQQ ETF Have a Bad Case of Premature Accumulation? Is the Software Apocalypse Real? Piper Sandler Just Slashed Its Price Target on Salesforce Stock. As Airline Stocks Sell Off on Jet Fuel Prices, Delta Is the Top-Rated Stock to Buy on the Dip