Income-focused investors in 2026 are slowly moving into infrastructure stocks linked to data centers because many of them now offer higher yields and steady, long-term contracts. Companies like AES Corporation (AES) stand out as an example here, with a forward dividend yield of about 4.3%, supported by long agreements with big tech players like Alphabet's (GOOG) (GOOGL) Google and other deals tied to data center growth across major U.S. regions.

That trend is being reinforced by another round of big tech spending. Amazon’s (AMZN) plan to invest $25 billion in Mississippi data centers adds more weight to the ongoing buildout of cloud and AI infrastructure. In this setup, another big infrastructure player, American Tower (AMT), plays a slightly different role. It is not just about owning data centers but about providing the tower and connectivity infrastructure that helps those data centers stay connected and run smoothly. The company also pays an annual dividend of about $6.80 per share, which comes out to just under a 4% yield, putting it in the same income-focused group of infrastructure stocks benefiting from this demand.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

With hyperscalers still spending heavily and no slowdown in sight, can a stock like AMT turn all this demand into steady income and long-term share gains? Let’s find out

AMT's Financial Engine

American Tower owns and leases wireless towers and other connectivity assets, and its CoreSite data center business gives it more exposure to cloud and AI traffic.

Over the past 52 weeks, AMT is down about 18%, though it remains slightly positive for the year, up 1.25% year-to-date (YTD).

www.barchart.com

www.barchart.comWith a forward P/E ratio of 17x compared to the sector average of 31.82x, the stock looks attractively priced for investors who want steady income at a fair value.

The latest quarter backed that up. Revenue came in at $2.738 billion, up 7.5% year-over-year (YoY), driven by steady leasing demand and continued growth in its data center business. That top-line strength flowed through to profitability, with Adjusted EBITDA at about $1.82 billion, also up roughly 7.5%, showing margins are still holding up. On cash flow, AFFO per share came in at $2.63, beating expectations.

Reported net income was $821 million for AMT shareholders, down sharply YoY due to non-operating items and currency swings. For the full year, revenue reached $10.65 billion, while net income attributable to shareholders totaled $2.53 billion. Free cash flow also stayed strong at $836 million for the quarter, supporting dividends and buybacks. Capital spending was $592 million, and the company also kept full-year AFFO guidance at $10.78 to $10.95 per share, which points to a steady payout base.

AMT’s Growth Story

Most of the growth story in AMT now comes from CoreSite, its data center business. Recently, CoreSite became a Google Gold Verified Peering Provider, which basically means it now has a stronger and more direct connection setup for companies using Google services like Google Cloud. It helps customers get faster and more reliable access without much complexity, especially for businesses running tools like Google Workspace or other cloud-based apps that need steady internet performance.

CoreSite also rolled out a native 400 Gbps AWS Direct Connect in its Chicago data center. This is built for heavier workloads, especially AI-related ones that need a lot of data moving quickly. It’s already being used by some customers, including a cybersecurity firm processing large data sets for real-time threat detection, while some financial companies are also looking at it for fast trading and research work.

On the income side, AMT currently offers an annual dividend yield of about 3.79%, paid out quarterly, with the latest dividend at $1.79 per share. The only concern is that the payout ratio is high at about 125.74%, meaning it is paying out more than its current earnings cover. Even so, the company has still managed to raise its dividend for two straight years, showing it is still trying to grow shareholder payouts, even if coverage is tight right now.

Wall Street’s Take and the Road Ahead

Looking ahead, Street estimates are anchored around $2.65 for the current quarter (03/2026), easing slightly from $2.75 a year earlier, then $2.62 for 06/2026 versus $2.60 the prior year, before stabilizing into $10.60 for fiscal 2026 compared to $10.76 previously.

Analyst sentiment remains firmly constructive. BMO Capital maintained an “Outperform” rating while adjusting its price target, lowering it from $250 to $245, but still citing strong international performance, expanding data center exposure, and rising U.S. carrier activity as core supports for the long-term thesis.

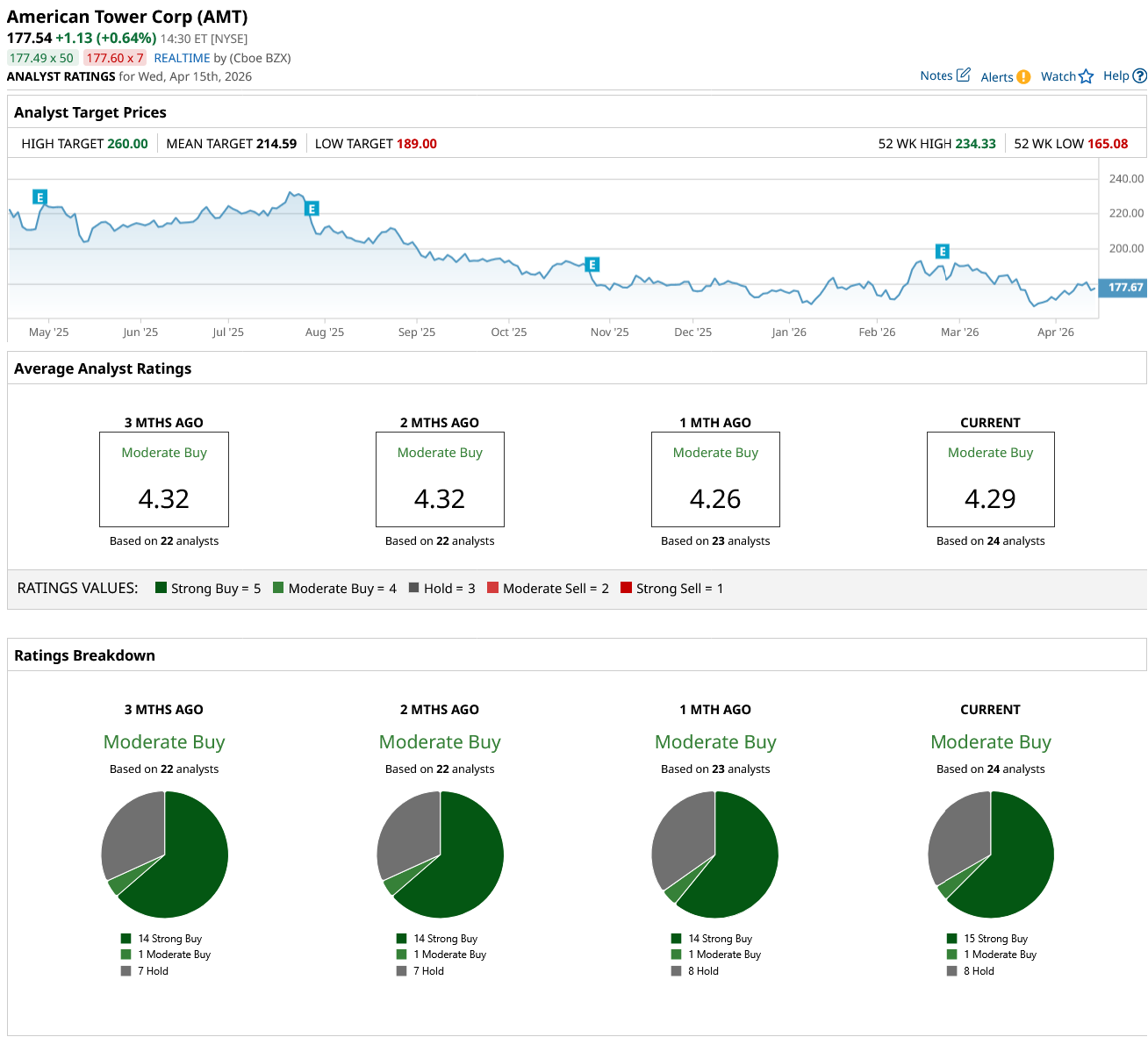

Across 24 analysts, AMT carries a “Moderate Buy” consensus, with an average price target of $214.59, implying an upside of roughly 22% from current levels.

www.barchart.com

www.barchart.comConclusion

Amazon’s extra $25 billion push into data centers just shows the same thing again: demand for digital infrastructure is still growing fast. American Tower is not directly building those data centers, but it is still tied in through its tower network and its CoreSite business, which connects to cloud and AI traffic. You still get close to a 4% dividend yield and fairly steady cash flow, with exposure to hyperscaler spending that the market does not fully price in yet. If cloud and AI spending stay strong, the stock is more likely to move up slowly over time rather than make big jumps, driven by income and gradual revaluation.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

As Amazon Pours Another $25B into Data Centers, Buy This 1 High-Yield Data Center Dividend Stock This Dividend Stock Is Becoming Too Cheap to Ignore: Should You Buy? Do New Energy Drink and Soda Sales Make McDonald’s Stock a Buy Here? Is Nokia Stock a Buy at 52-Week Highs?