Ondas Inc’s ONDS path to profitability targets positive EBITDA at its level only by the first quarter of 2028. Though the timeline appears long-drawn, it is tied to the company’s aggressive scaling of operations.

The company is not only focused on organic growth but has resorted to intense M&A activity. Ondas has deployed approximately $550 million across five acquisitions (in the first quarter of 2026 alone), which are expected to contribute around $230 million in revenues in 2026. Management noted that the expansion was driving a larger backlog and revenues, as well as expanding ONDS’ gross profit. These are expected to cushion operating leverage and boost profitability.

Further, ONDS’ strong balance sheet is acting as an anchor. The company has resorted to financing ($1.8 billion since mid-2025), and this has boosted the pro forma cash balance to $1.5 billion. This provides ample financial flexibility to carry on with its transformation efforts.

However, Ondas’ transformation efforts strengthen long-term competitive moat, but amplify short-term financial pressure. For 2025, the adjusted EBITDA loss widened to $31.3 million compared with a loss of $28.5 million. Adjusted EBITDA losses are expected to widen in the first quarter due to higher operating expenses, including increased leadership hiring and marketing investments to support rapid growth. Ondas expects EBITDA margins to improve over the year and product-level profitability by the third quarter of 2026. OAS profitability is expected by the third quarter of 2027.

Also, the path to profitability remains heavily dependent on flawless execution. Any delays in integration and order conversion could push the profitability timeline further out. Moreover, competition in an increasingly crowded drone space remains a concern.

Taking a Look at Rival’s Profitability Metrics

AeroVironment AVAV is one of the key pure-play beneficiaries of rising global demand for military drones and its biggest competitive moat is the strategic ties with the United States and allied governments.

Adjusted gross margin in the third quarter fell to 27% compared with 40% in the prior-year quarter. Margin performance is being affected by a higher service mix and early-stage products. Adjusted EBITDA margin was 11%, representing a modest improvement from 10% in the fiscal second quarter. AeroVironment expects a sequential recovery in the fiscal fourth quarter. Management expects adjusted gross margins to improve to the low-to-mid 30% range in the fiscal fourth quarter.

For fiscal 2026, AeroVironment reiterated its expectation for adjusted gross margins to be in the high-20s to low-30s percentage range. The company also guided for adjusted EBITDA margins of 14% to 15% for the year.

Unusual Machines UMAC is also benefiting from a favorable demand environment, with management highlighting that the drone market is currently supply-constrained, with demand expected to exceed supply through 2027. Fourth-quarter 2025 revenues of $4.9 million rose 133% sequentially, while full-year revenues were $11.2 million, up 101% year over year. Gross margin expanded to 36% in the fourth quarter from 24% in the first quarter of 2025.

Nonetheless, UMAC faces increasing operating costs. For 2025, operating expenses stood at $29 million, up from $18.5 million in 2024. UMAC expects gross margins to deteriorate in the first and second quarters of 2026 owing to hiring and the creation of new processes.

ONDS’ Price Performance, Valuation and Estimates

Shares of ONDS have lost 5.8% in the past month compared with the Wireless-National industry’s decline of 4.9%

Image Source: Zacks Investment Research

In terms of the forward 12-month Price/Sales ratio, ONDS is trading at 10.38, considerably higher than the industry’s multiple of 1.8.

Image Source: Zacks Investment Research

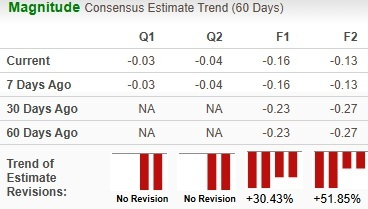

The Zacks Consensus Estimate for ONDS’ earnings for the current year has been revised upwards over the past 60 days.

Image Source: Zacks Investment Research

ONDS currently has a Zacks Rank #5 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AeroVironment, Inc. (AVAV): Free Stock Analysis Report

Ondas Holdings Inc. (ONDS): Free Stock Analysis Report

Unusual Machines, Inc. (UMAC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).