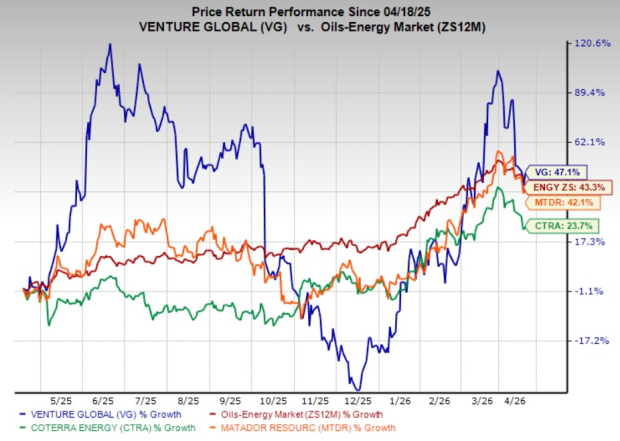

Venture Global VG has delivered an impressive run, with its shares jumping 47.1% over the past year, outpacing the industry’s 43.3% growth, and respective gains of 23.7% and 42.1% from peers Coterra Energy Inc. CTRA and Matador Resources MTDR.

The strong price performance reflects growing investor confidence in VG’s long-term prospects, particularly in a favorable energy pricing environment. Despite this momentum, investors should carefully evaluate the company’s fundamentals, growth trajectory and broader market conditions before making investment decisions.

Strong LNG Expansion Driving Growth

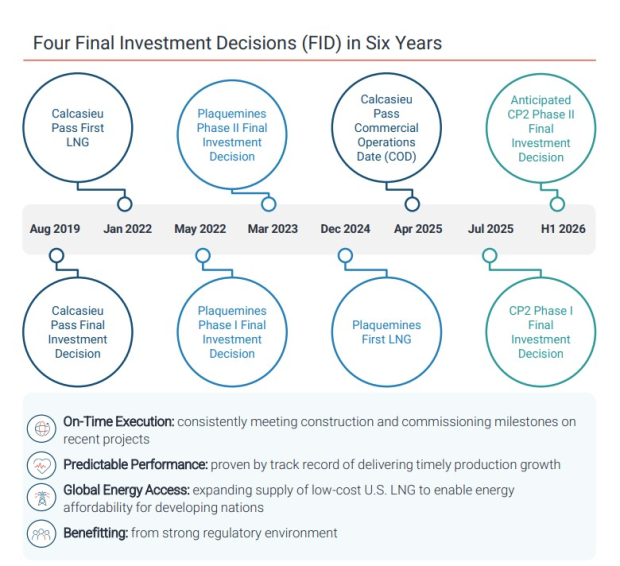

Venture Global, one of the leading natural gas exporters in the United States, has made notable progress in scaling its LNG business, positioning itself among the fastest-growing LNG exporters globally. The company currently has multiple large-scale projects across different stages — Calcasieu (operational), Plaquemines (commissioning) and CP2 (under construction). These projects collectively provide a pathway to more than 150 million tonnes per annum (MTPA) of expected production capacity, with long-term ambitions exceeding 100 MTPA of installed capacity.

The company’s growth strategy is supported by its efficient execution model and integrated business approach. Its modular “design-one, build-many” strategy enables faster project completion than traditional LNG players, allowing production to begin in nearly 30 months after the final investment decision. VG has demonstrated the ability to monetize projects early through commissioning cargo sales, improving cash flow visibility.

Integrated Model & Strategic Advantages

Venture Global is strengthening its competitive position through vertical integration across the LNG value chain. Investments in pipelines, LNG shipping and regasification infrastructure in key markets like Europe enhance margins and reduce the reliance on third parties. This integrated approach allows the company to capture value across the supply chain, improving resilience during market volatility.

The company’s focus on bolt-on expansions, adding capacity to existing facilities, helps reduce capital costs and execution risks while improving returns. A unique advantage of VG’s model is its ability to produce LNG above nameplate capacity, potentially up to 40% higher under optimal conditions. This excess output can be sold in spot markets, providing upside during periods of strong LNG pricing.

A key strength of VG lies in its strong contract base, with approximately $134 billion in long-term agreements, typically spanning around 20 years. These contracts provide stable and predictable cash flows through a mix of fixed liquefaction fees and variable pricing linked to natural gas markets. This structure limits downside risks while still allowing participation in favorable pricing environments.

A strong global energy environment, supported indirectly by high crude oil prices, can boost LNG demand and pricing, enhancing margins on uncontracted volumes.

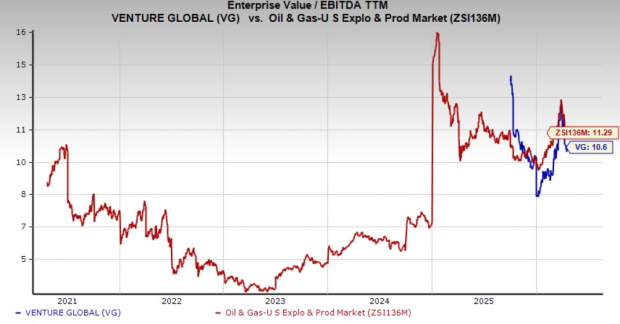

Valuation Snapshot

From a valuation standpoint, VG appears relatively attractive. The stock is currently trading at a trailing 12-month EV/EBITDA multiple of 10.6X, which is slightly below the broader industry average of 11.29X. This suggests that the stock may still offer value despite its recent run-up.

Image Source: Zacks Investment Research

Should You Buy the Stock Now?

Venture Global’s strong execution capabilities, expanding LNG footprint and robust contract base position it well to capitalize on rising global demand for natural gas. Its ability to generate early cash flows, combined with upside from spot sales and excess capacity, adds to its investment appeal.

Given the company’s solid growth outlook and supportive industry dynamics, VG appears well-positioned for long-term gains. The stock currently carries a Zacks Rank #2 (Buy), and investors can consider owning it at the current level, while keeping an eye on the broader LNG market trends. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Matador Resources Company (MTDR): Free Stock Analysis Report

Venture Global, Inc. (VG): Free Stock Analysis Report

Coterra Energy Inc. (CTRA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).