Oracle ORCL and ServiceNow NOW are enterprise software giants competing intensely for large corporate IT budgets while aggressively expanding their artificial intelligence capabilities. Oracle is a diversified cloud infrastructure, database and applications powerhouse; ServiceNow has built its identity as an AI-driven workflow automation platform.

Both stocks carry premium valuations and have outlined ambitious multiyear revenue roadmaps, making them a compelling pair for technology investors to compare amid a turbulent 2026 market environment.

Let's delve deep and closely compare the fundamentals of the two stocks to determine which one is a better investment now.

The Case for ORCL Stock

Oracle is undergoing a significant transformation from a legacy software vendor to a cloud and AI infrastructure powerhouse. Per its third-quarter fiscal 2026 earnings release, cloud revenues surged 44% year over year to $8.9 billion, with AI infrastructure revenues up 243% and multicloud database revenues up 531%. Remaining performance obligations (RPO) reached $553 billion, up 325% year over year, reflecting extraordinary demand visibility. Following these strong results, management raised its fiscal 2027 revenue target to $90 billion, while fourth-quarter fiscal 2026 guidance calls for cloud revenue growth of 46-50%.

Oracle's AI World Tour 2026, traveling across global markets, continues to unveil significant product innovations, including Fusion Agentic Applications — a new class of AI-driven enterprise apps spanning finance, HR, supply chain and CX. In April 2026, Oracle announced sweeping enhancements to Oracle AI Database 26ai, delivering Platinum and Diamond-tier mission-critical availability for demanding workloads. The company has also secured over 10 gigawatts of data center capacity, with more than 90% partner-funded, supporting a capital-efficient path to revenue conversion.

Oracle is not without meaningful risks. A $30 billion financing raise — part of a planned $50 billion program — adds substantially to an already heavy debt load. Capital expenditure commitments at this scale introduce execution risk if AI demand softens. The Cerner integration, particularly the Department of Veterans Affairs contract, remains a source of friction. Cloud competition from AWS and Microsoft is persistent. Nevertheless, Oracle's record $553 billion RPO, rising margins, raised fiscal 2027 revenue outlook, and expanding multicloud capabilities make a broadly constructive investment case.

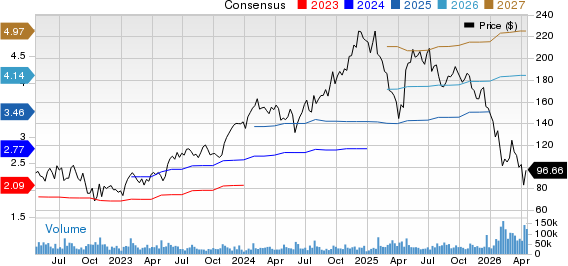

The Zacks Consensus Estimate for ORCL's fiscal 2026 earnings is pegged at $7.45 per share, indicating 23.55% growth year over year.

Oracle Corporation Price and Consensus

Oracle Corporation price-consensus-chart | Oracle Corporation Quote

The Case for NOW Stock

ServiceNow has long been regarded as one of enterprise software's most consistent performers, and fourth-quarter 2025 continued that track record on paper. Subscription revenues grew 21% year over year to $3.47 billion, with current RPO reaching $12.85 billion — up 25%. The company's board authorized an additional $5 billion share repurchase program and reported an impressive 98% renewal rate, signaling strong underlying customer retention. For 2026, management guided subscription revenues to be in the band of $15.53-$15.57 billion, suggesting 19.5-20% growth, while also targeting a free cash flow margin of 36%.

However, ServiceNow's growth narrative is becoming expensive to sustain. The company is simultaneously pursuing three major acquisitions — Moveworks, Armis and Veza — which elevates integration complexity and shifts focus from organic momentum. The Moveworks acquisition contributes only 100 basis points to 2026 subscription revenue growth, a modest return on a significant capital commitment. Management also flagged a material 150 basis point headwind in first-quarter 2026 from a mix shift toward hosted revenues as hyperscaler partner offerings gain traction — a near-term pressure point that investors should monitor.

ServiceNow's guided 2026 subscription revenue growth of approximately 19.5-20% represents a notable deceleration from prior-year trends, raising legitimate questions about possible platform saturation in its core IT service management market. Federal government exposure introduces meaningful uncertainty in the current policy environment. While ServiceNow positions itself as the "AI control tower for business reinvention" — evidenced by its April 2026 announcement making the entire product portfolio AI-enabled — its growing reliance on acquisitions to sustain growth momentum is a structural concern.

The Zacks Consensus Estimate for NOW’s 2026 earnings has been steady at $4.14 per share over the past 30 days and indicates 17.95% growth from 2025’s reported figure.

ServiceNow, Inc. Price and Consensus

ServiceNow, Inc. price-consensus-chart | ServiceNow, Inc. Quote

Valuation and Price Performance Comparison

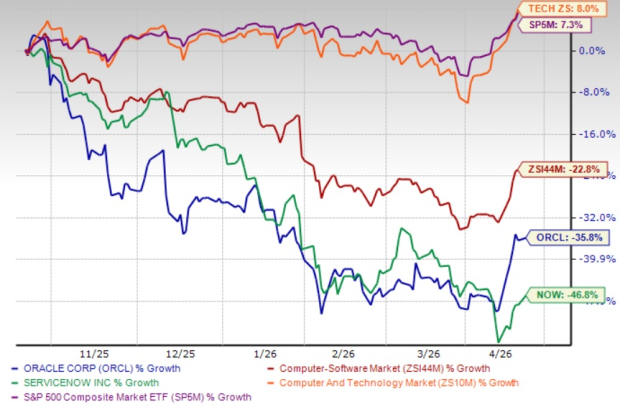

ServiceNow shares have plunged 46.8% in the past six-month period, underperforming the Zacks Computer and Technology sector's growth of 8% and Oracle’s plunge of 35.8% — signaling that the market is applying a meaningful de-rating to NOW stock.

ORCL Outperforms NOW in 6 Months

Image Source: Zacks Investment Research

Both ORCL and NOW trade at a premium to the sector, but the comparison reveals a clear divergence in justification. Both ORCL and NOW have a Value Score of D. ServiceNow's elevated forward 12-month price-to-sales ratio of 5.95Sx, set against decelerating organic growth and mounting M&A execution risk, makes its premium difficult to defend at current levels. Oracle's relatively modest 5.89x multiple is better supported by its accelerating cloud revenue trajectory, record $553 billion RPO, and raised fiscal 2027 guidance of $90 billion.

ORCL vs. NOW: P/S F12M Ratio

Image Source: Zacks Investment Research

Conclusion

Oracle holds a clear edge over ServiceNow at this juncture. Its accelerating cloud and AI revenues, a record $553 billion RPO, raised 2027 revenue guidance of $90 billion, expanding multicloud reach, and AI database innovations collectively underpin a stronger fundamental growth outlook. ServiceNow's decelerating organic growth, simultaneous M&A integration burden, near-term revenue mix headwinds and the steepest YTD stock decline among its peers make it a less compelling bet. Oracle's lower forward P/S of 5.01x versus ServiceNow's 6.55x further strengthens the case. Investors should carefully track Oracle for a better entry point while steering clear of ServiceNow stock right now. ORCL currently carries a Zacks Rank #3 (Hold), whereas NOW has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Oracle Corporation (ORCL): Free Stock Analysis Report

ServiceNow, Inc. (NOW): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).