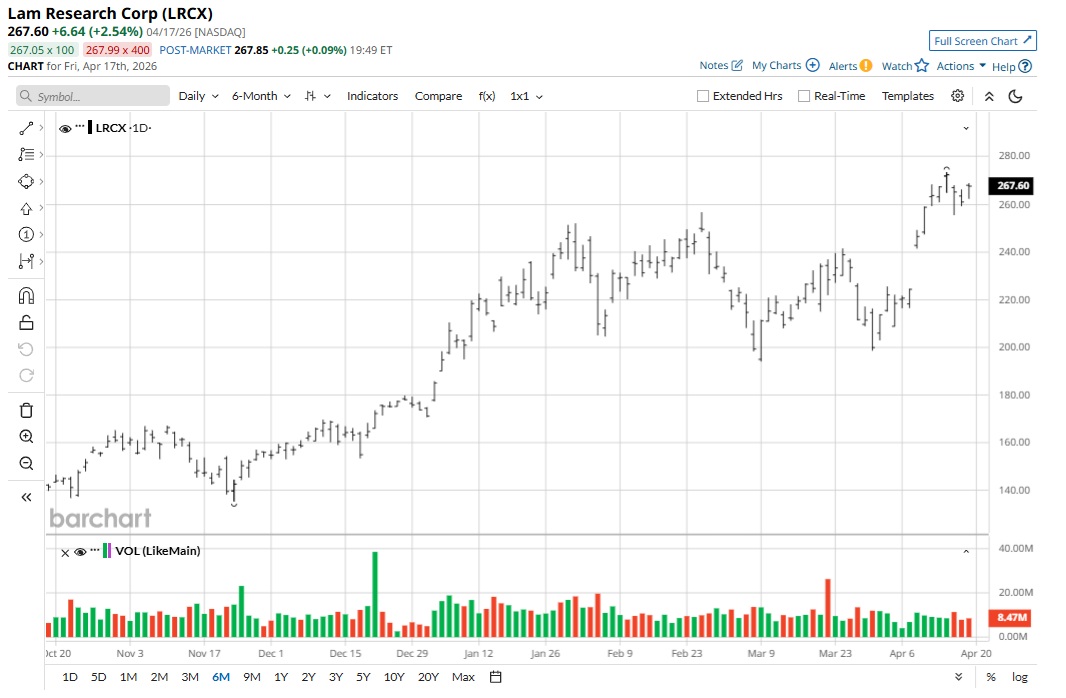

Any story related to the semiconductor industry has practically turned into gold in the last 12 to 18 months. Lam Research (LRCX) is no exception, with LRCX stock up more than 318% in the last 52 weeks. The rally in the wafer fabrication equipment (WFE) and services provider has been backed by positive fundamental developments.

In maybe the most recent development, Elon Musk's Terafab project has reportedly reached out to firms like Lam Research and Applied Materials (AMAT) for potential supplies. It’s worth noting that Terafab is a joint venture (JV) that involves Tesla (TSLA), SpaceX, and xAI.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

This JV is targeting advanced 2-nanometer chip production by 2029 with a target of building the world’s largest fabrication plant. Therefore, a potential supply collaboration for Lam Research could be a game changer in terms of top-line growth acceleration.

About Lam Research Stock

Headquartered in Fremont, California, Lam Research is a supplier of innovative wafer fabrication equipment and services. The company’s customer base includes semiconductor memory, foundry, and integrated device manufacturers.

For fiscal 2025, Lam Research reported revenue of $18.44 billion. In terms of geographical diversification, the company reported 34% of fiscal 2025 revenue from China, while Korea, Taiwan, and Japan contributed roughly 22%, 19%, and 10% of revenue, respectively. For the same period, operating cash flow was robust at $6.17 billion. Importantly, Lam Research also reported $2.1 billion in R&D spending in fiscal 2025, underscoring its focus on innovation-driven growth.

As demand for semiconductors continues to swell, Lam Research is positioned for sustained growth and robust cash flows. In-line with structural industry tailwinds and company-specific growth, LRCX stock has trended higher by almost 80% in the last six months.

www.barchart.com

www.barchart.com Ample Growth Opportunities

In its annual report, Lam Research projected the WFE market to surpass $100 billion in 2025. Further, the firm expects WFE spending to grow at a robust pace in the coming years. To put things into perspective, data-center capacity buildouts alone are projected to require approximately $200 billion of wafer fabrication equipment investments over the next five years.

Of course, there is additional demand from cloud computing, artificial intelligence, 5G, and the Internet of Things (IoT). Overall, this provides industry leaders like Lam Research with headroom for sustained growth.

Lam’s advanced packaging business is also expected to grow in calendar year 2026. This segment is likely to be the key growth driver. With Lam Research having enhanced manufacturing capacity in the last four years, the stage is set for accelerated growth and cash flow upside.

Lam Research provided some insights on the potential growth trajectory during its Investor Day 2025. By calendar year 2028, the company is targeting revenue of $25 billion to $27 billion with a gross margin of 50%. Further, free cash flow (FCF) as a percent of revenue is expected at 30%. At the midpoint of Lam's revenue guidance, the FCF potential is therefore $7.8 billion. This positions Lam Research for continued value creation.

What Do Analysts Say About LRCX Stock?

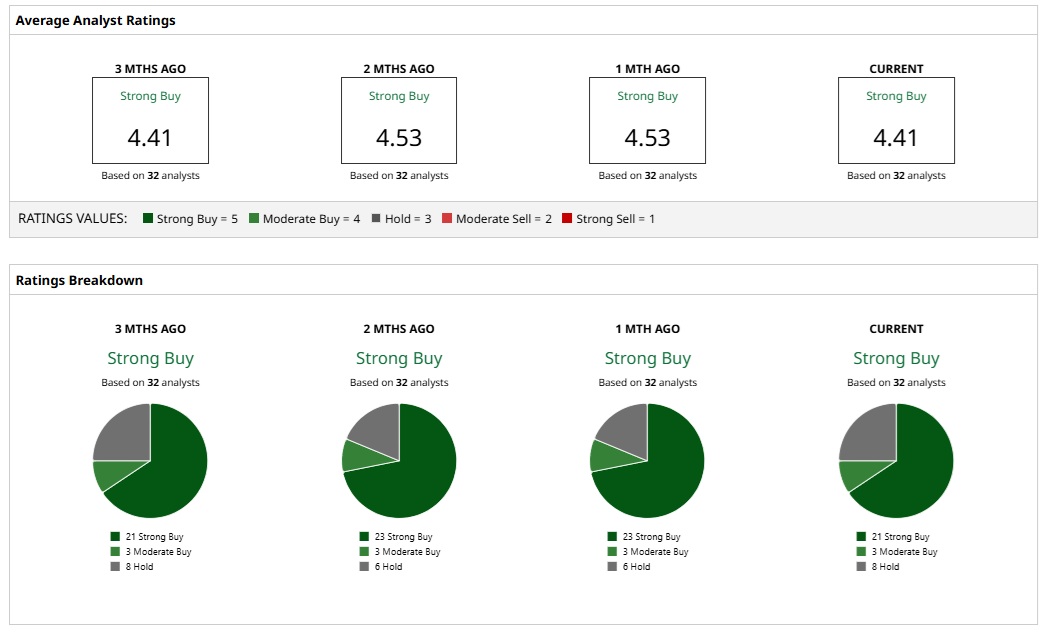

Based on 32 analysts with coverage, LRCX stock has a consensus “Strong Buy” rating. While 21 analysts have a “Strong Buy” rating for LRCX stock, three analysts have a “Moderate Buy” while eight analysts have a “Hold” rating.

The mean price target of $282.05 represents potential upside of 8% from current levels. Further, the most bullish price target of $350 suggests that LRCX stock could climb 35% from here.

Among prominent analyst views, Bank of America believes that Applied Materials and Lam Research are top picks in the semiconductor equipment space. This view is backed by the point that chip equipment spending will continue to swell in the coming years with estimates of $140 billion in 2026, $171 billion in 2027, and $193 billion in 2028.

According to analyst estimates, Lam Research likely to deliver earnings growth of 28% and 30% in fiscal 2026 and fiscal 2027, respectively. Healthy growth will likely ensure positive price action for LRCX stock.

www.barchart.com

www.barchart.com On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Missed Nvidia? AMD Could Be Your Second Chance to Earn Massive AI Gains TSLA Stock Catalyst: Get Ready for a Larger Model Y After the Blue Origin Satellite Failure, Is It Time to Sell AST SpaceMobile Stock? As Lam Research Joins the Tesla Terafab, Should You Buy, Sell, or Hold LRCX Stock?